|

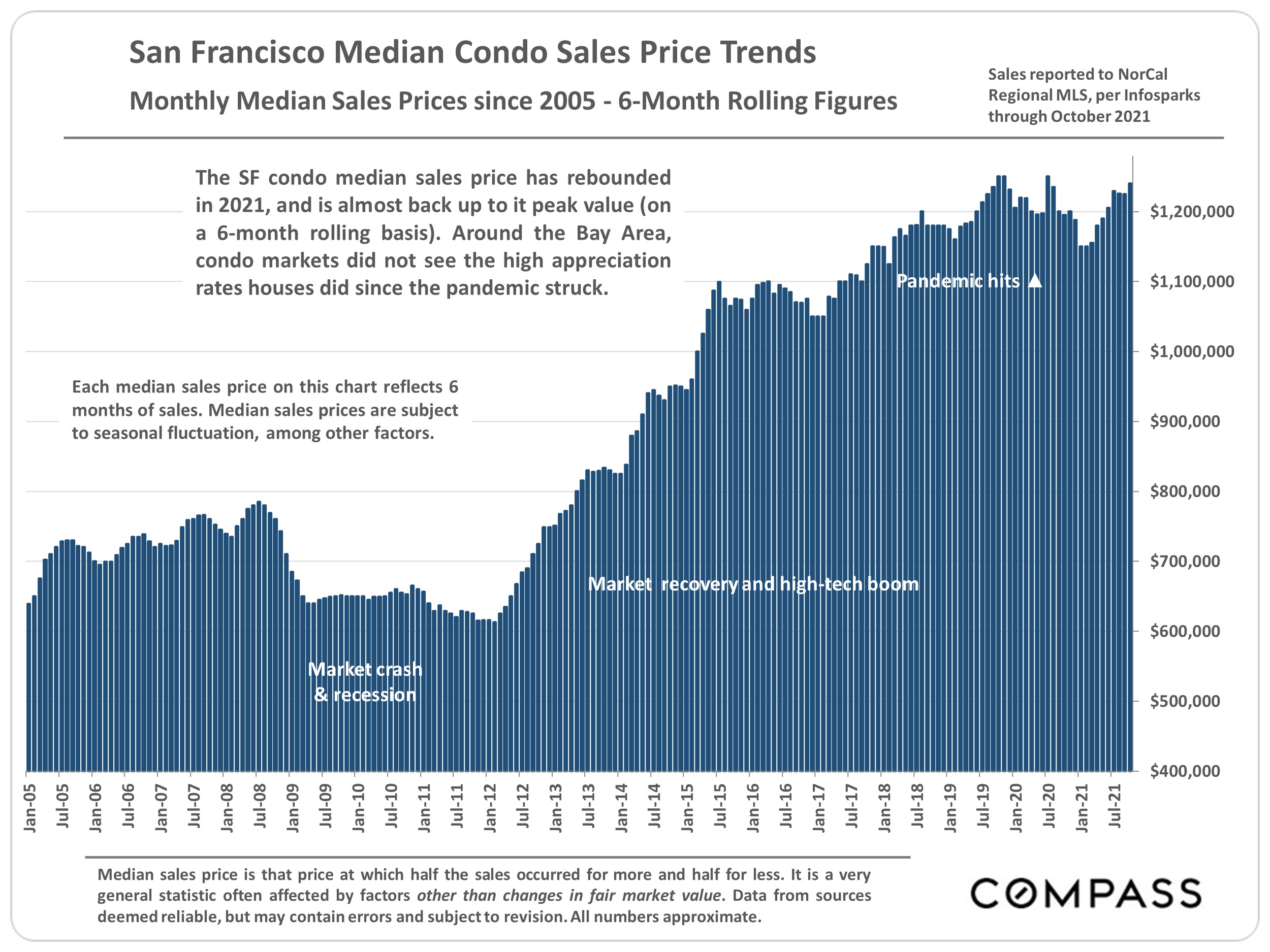

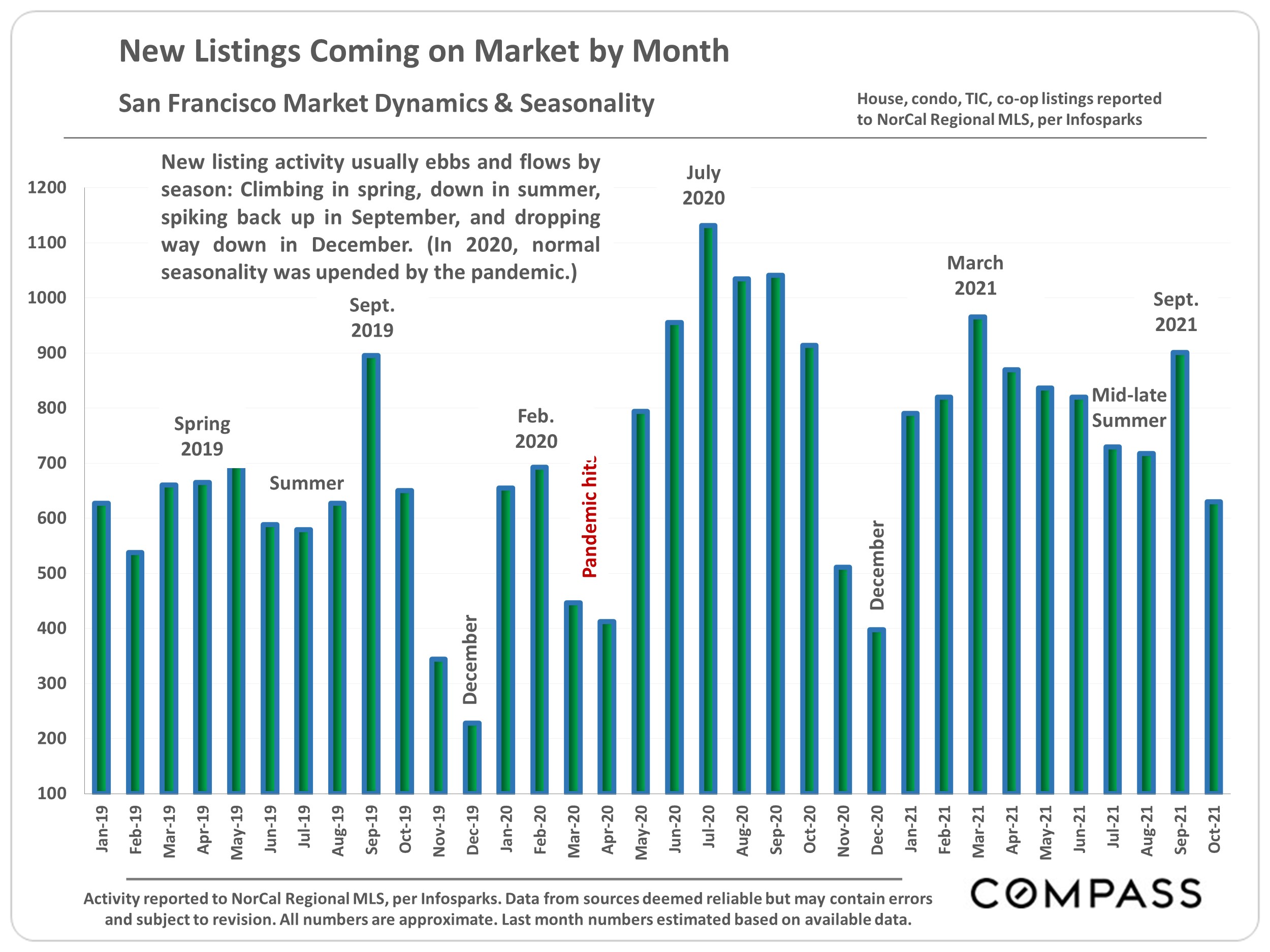

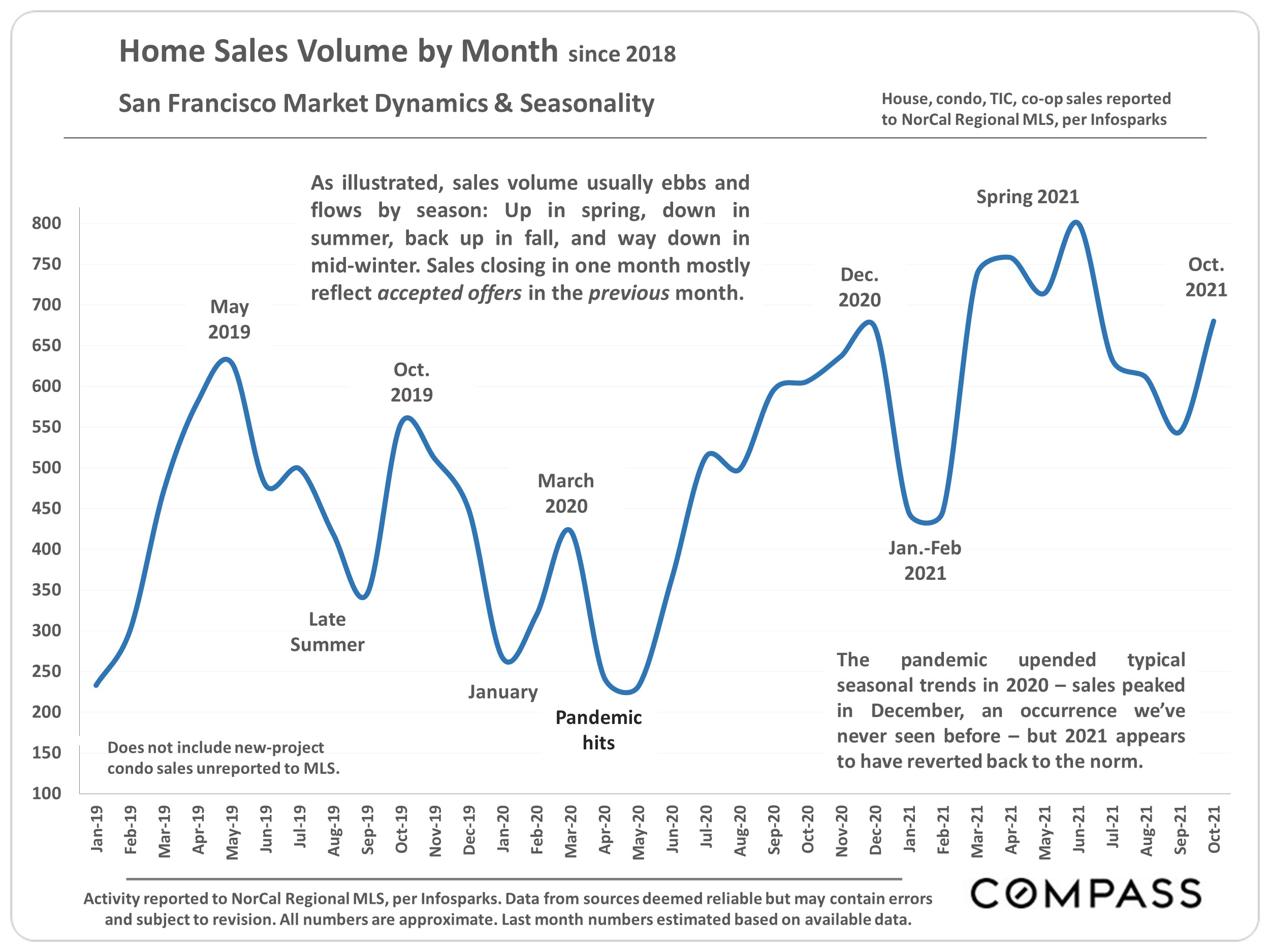

As the year begins to wind down and move into the mid-winter holidays, the market typically slows down as well: The number of new listings declines, to finally plunge in December, with sales volume following one step behind. Price reductions often jump, and some listings, especially of more expensive homes, are pulled off the market until the market wakes up in the new year – usually in late January or February depending on the weather and other factors. Of course, buying and selling occur at all times of the year, including in mid-winter, but commonly at a much reduced rate. Note that typical market seasonality was often upended in 2020 due to the pandemic; more normal seasonal trends seem to have returned in 2021.

For buyers, the coming months can offer substantial opportunities in the form of reduced competition, fewer multiple offers, less overbidding, more room to negotiate, and often significantly better deals. This is an excellent time for buyers to take a second look at listings that haven’t sold, and to make aggressive offers.

This report will review home prices appreciation by property type in selected city neighborhoods, supply and demand dynamics as illustrated by a variety of statistical measures, luxury home sales, and a survey of selected macroeconomic indicators.

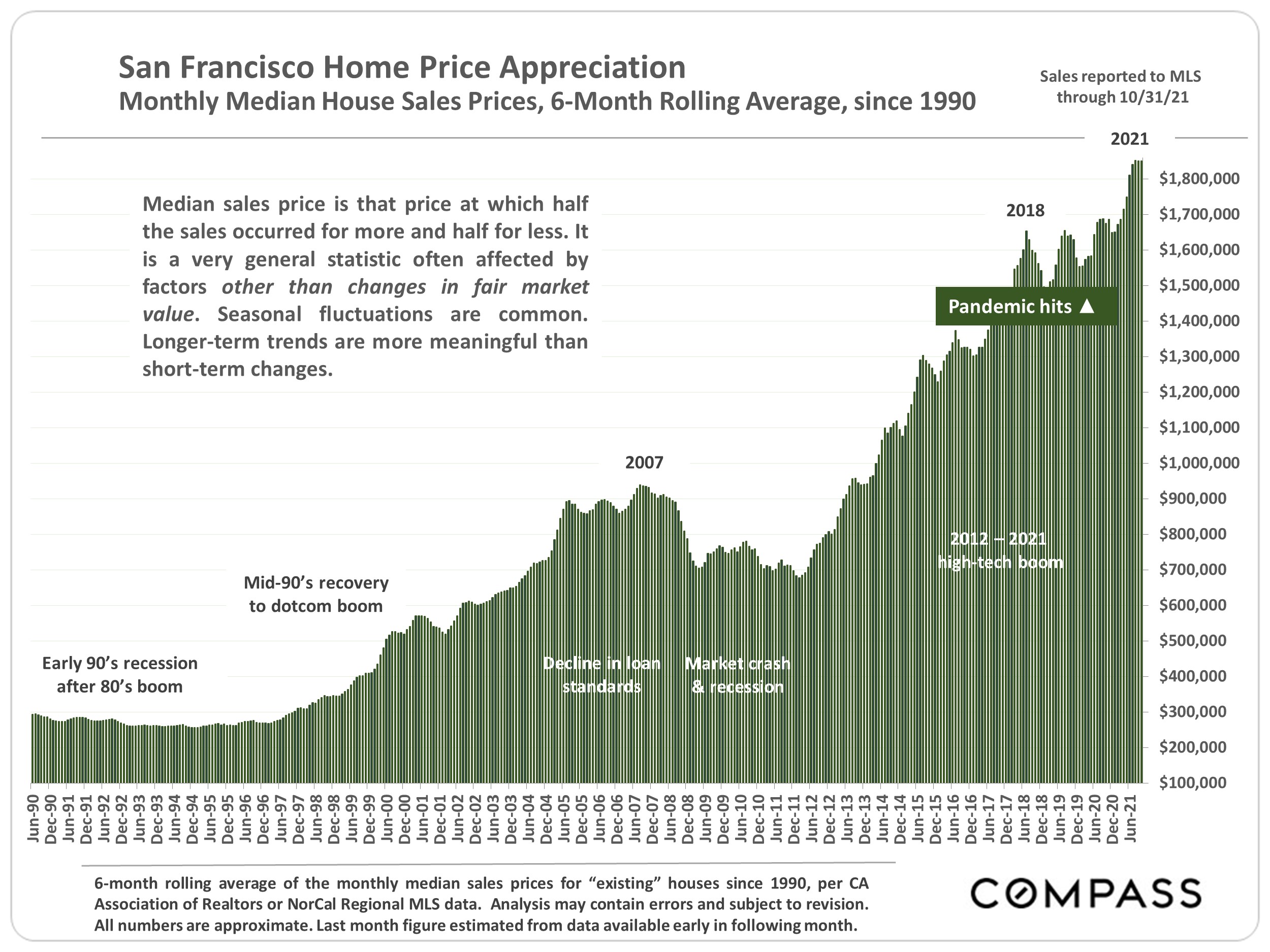

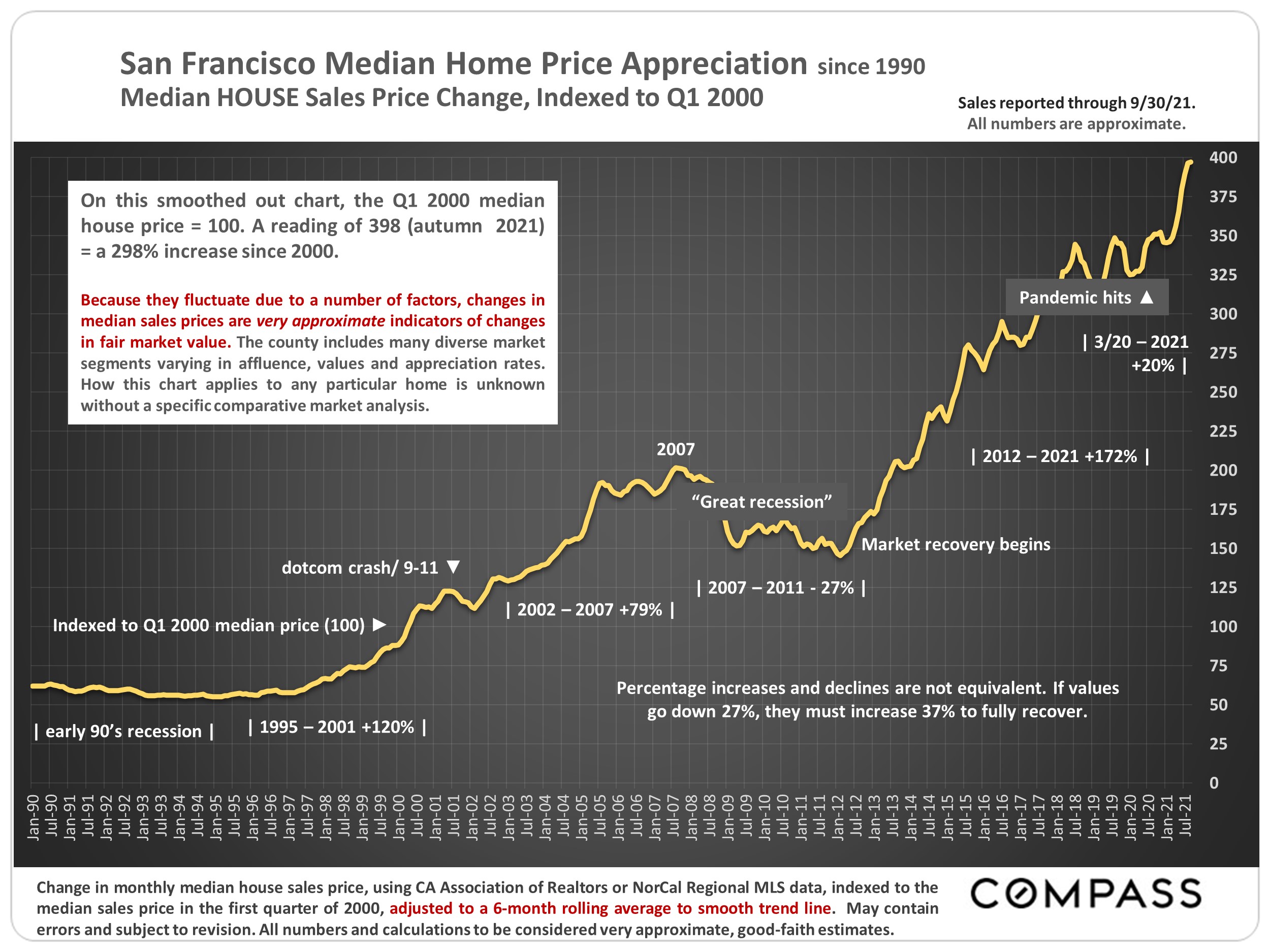

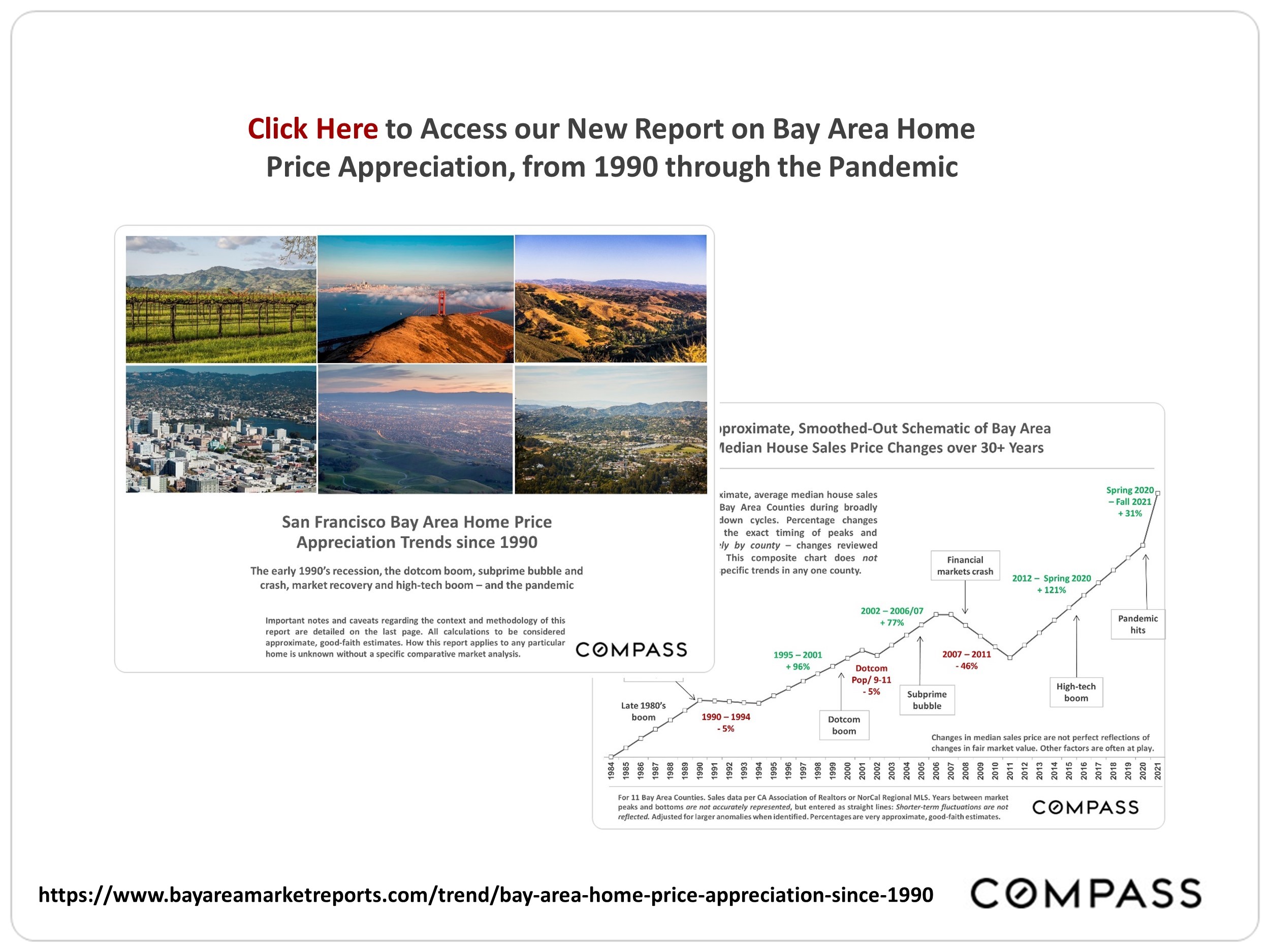

The following chart reviews approximate media house sales price changes since 1990, breaking down percentage ups and downs during periods such as the dotcom era, the subprime bubble, the recent high-tech boom, and the pandemic. Readings on the chart refer not to specific prices, but to the Q1 2000 median sales price, assigned a value of 100: A reading of 180 signifies the median house price has increased by 80% since Q1 2000.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Source: Compass

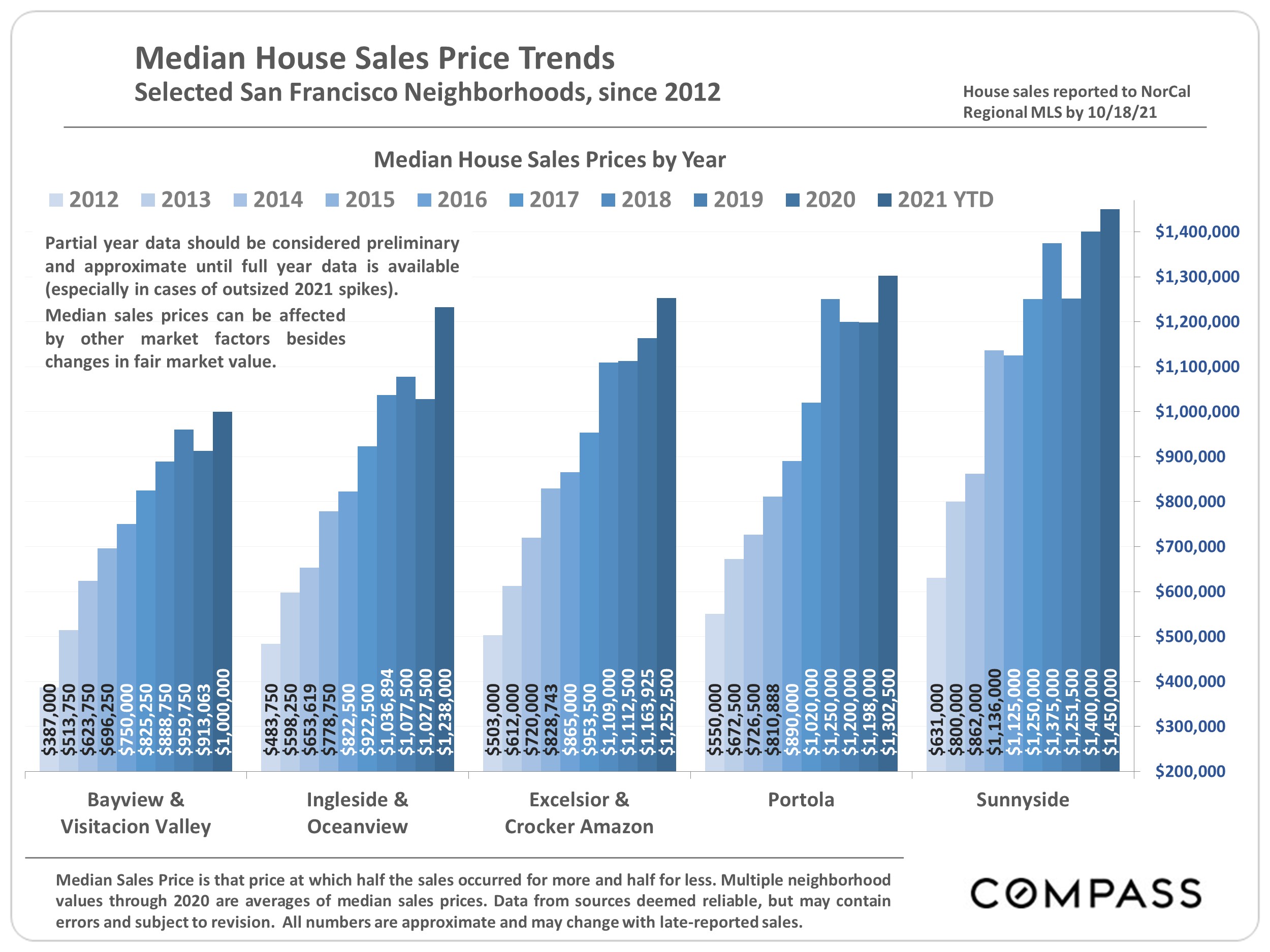

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.