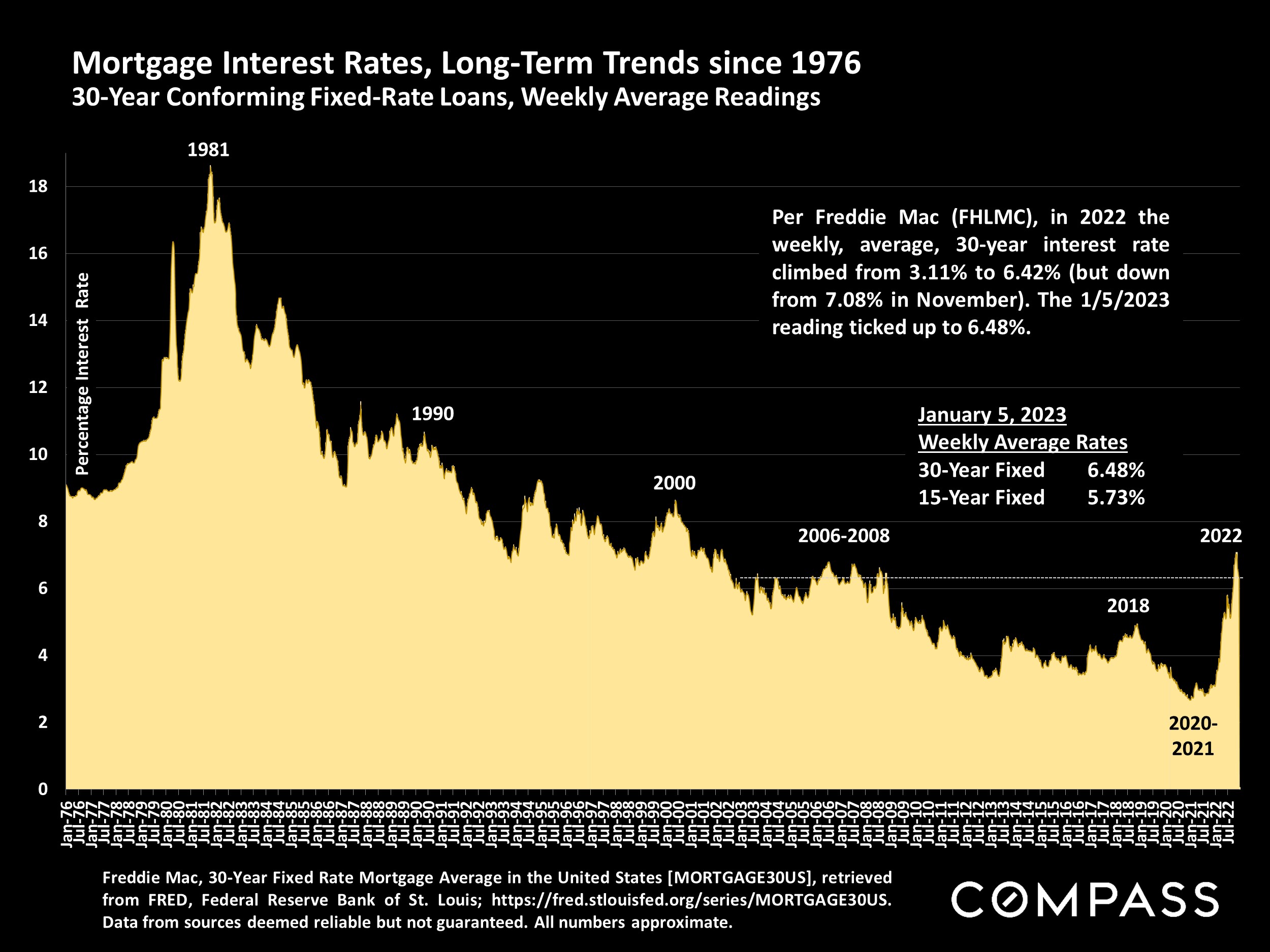

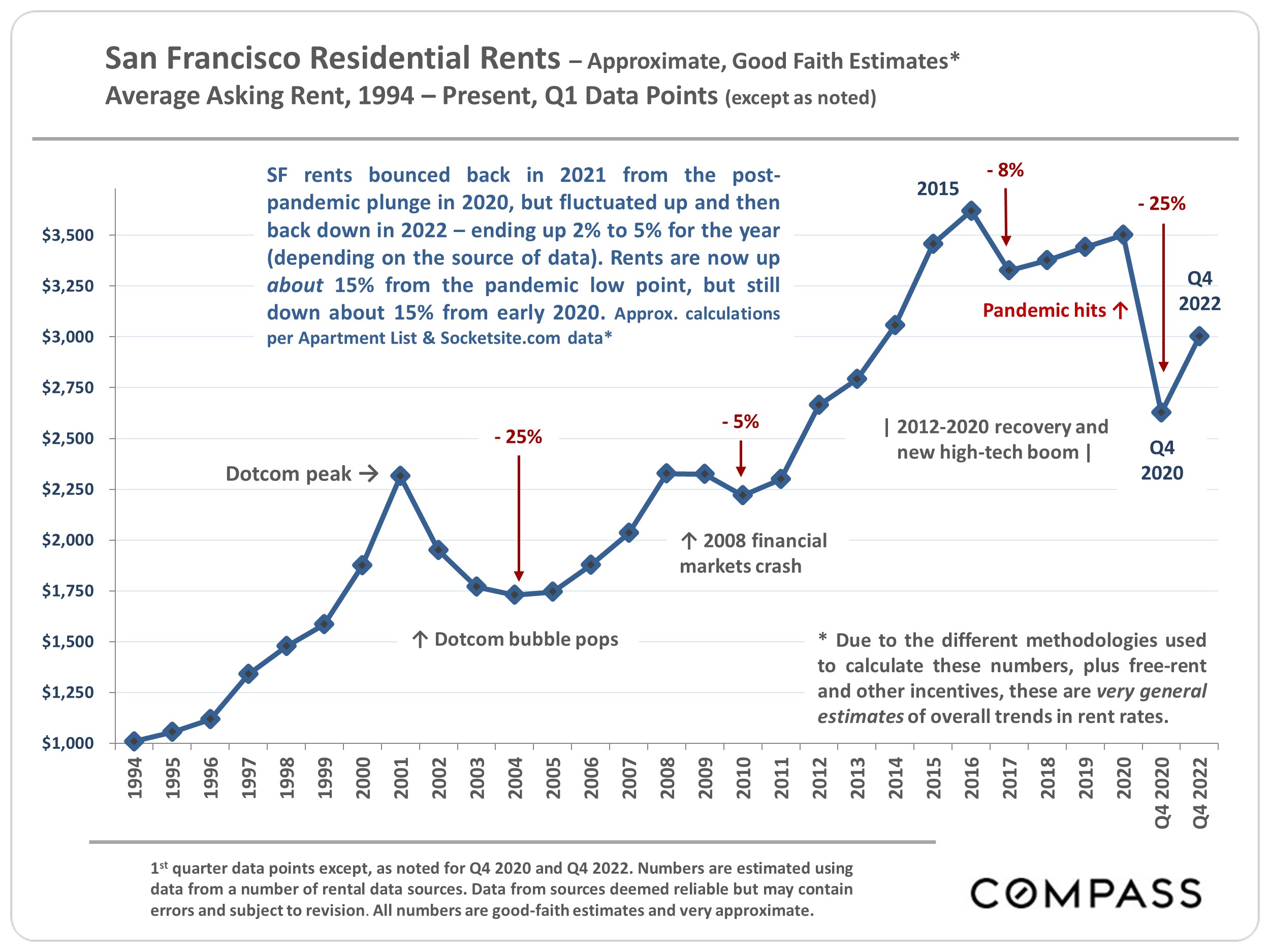

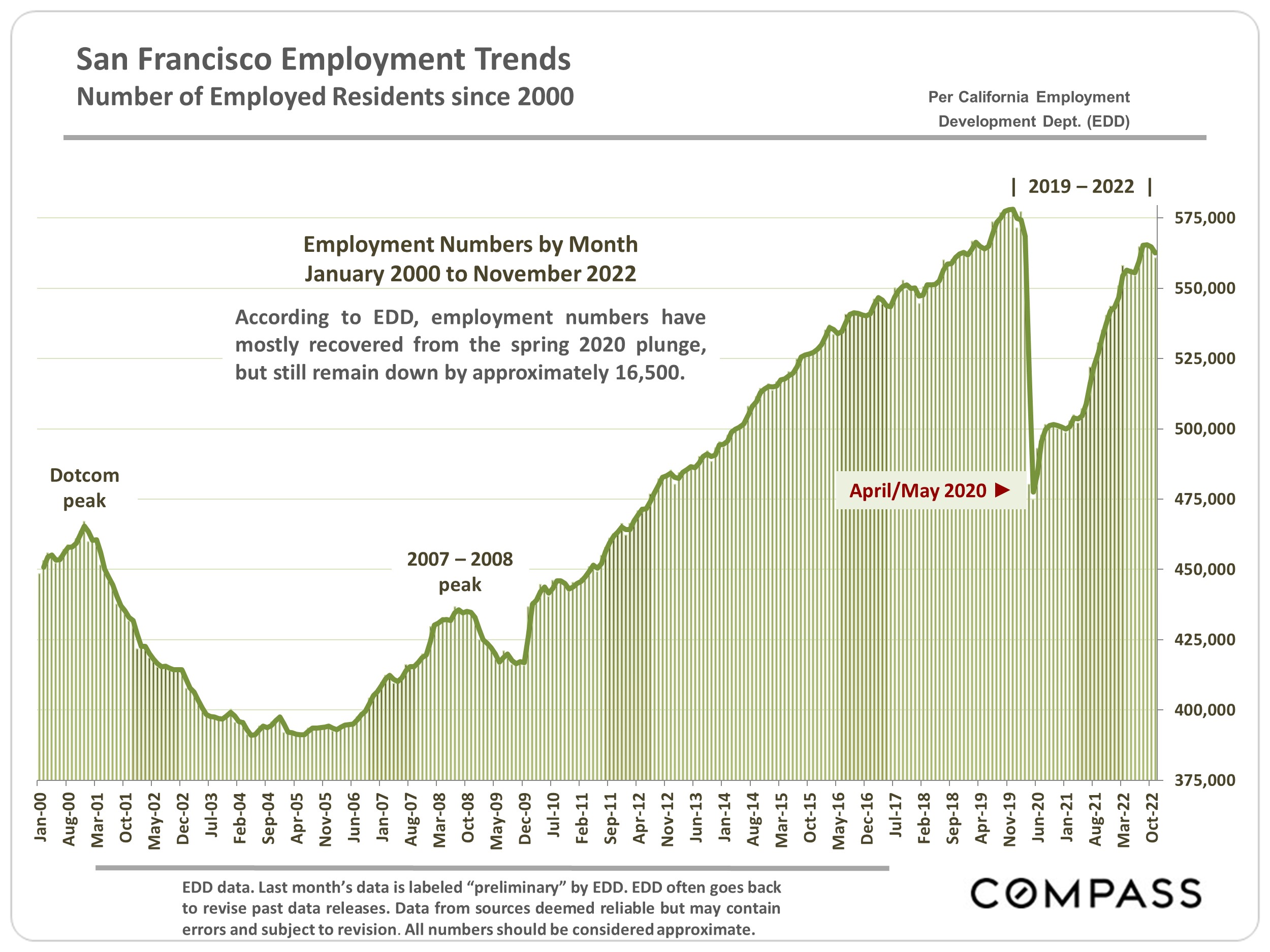

The San Francisco rental property market continued to be affected by general economic factors, such as interest rates and financial markets, as well as issues more specific to the city, such as tech lay-offs, work from home, social issues such as homelessness, the (still) high cost of housing relative to other regions, and half-empty office buildings. Weekly office attendance in the multi-county San Francisco Metro Area is more than 50% below pre-pandemic levels, a major factor in demand for rental apartments. In the space of less than 3 years, San Francisco has gone from one of the strongest office markets in the world to one of the weakest, impacting the downtown rental market the most. Employment has mostly recovered from the huge, initial pandemic plunge, but remains down by about 16,500 workers, reflecting a decline in the city’s population. The unemployment rate is close to historic lows.

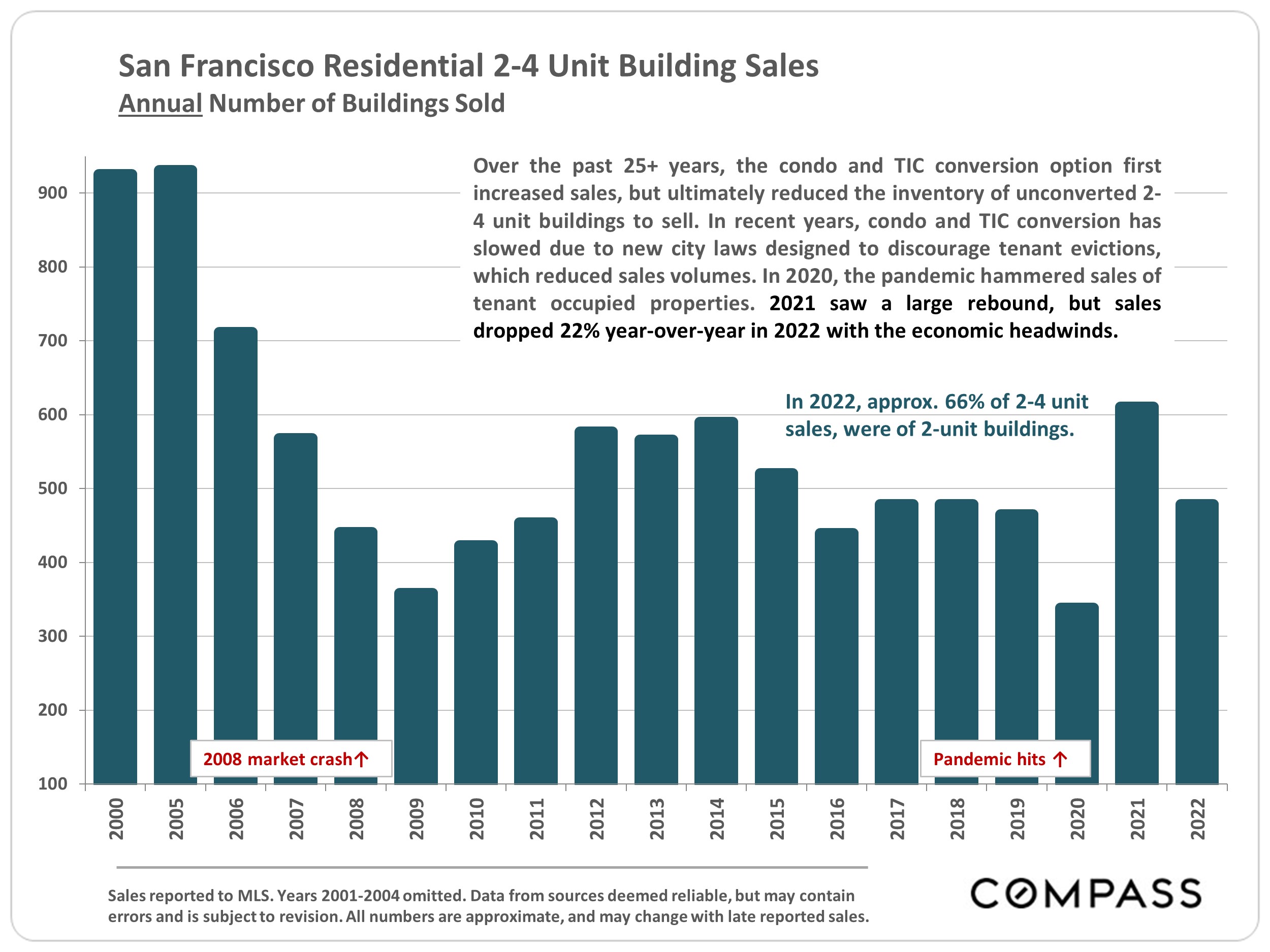

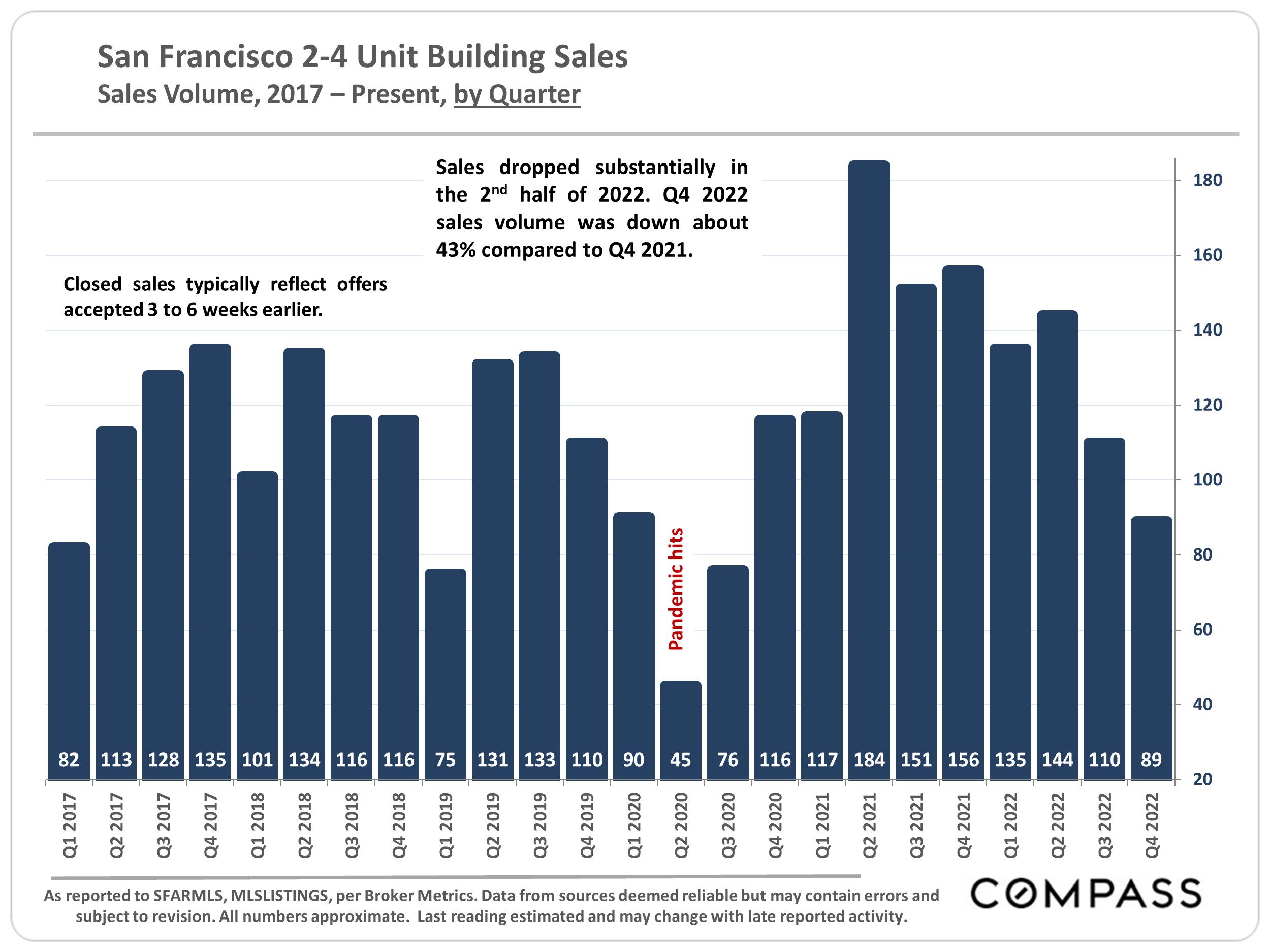

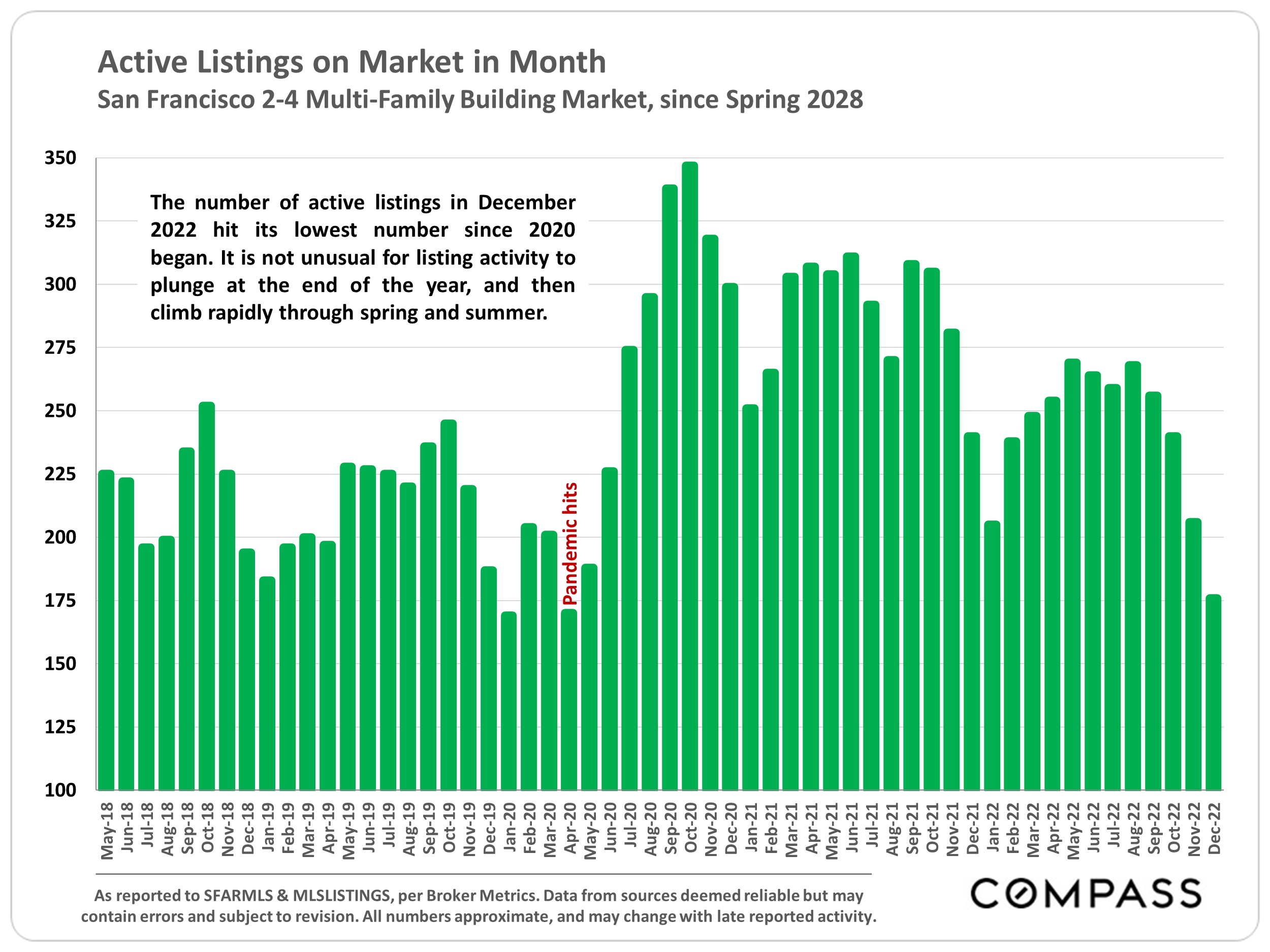

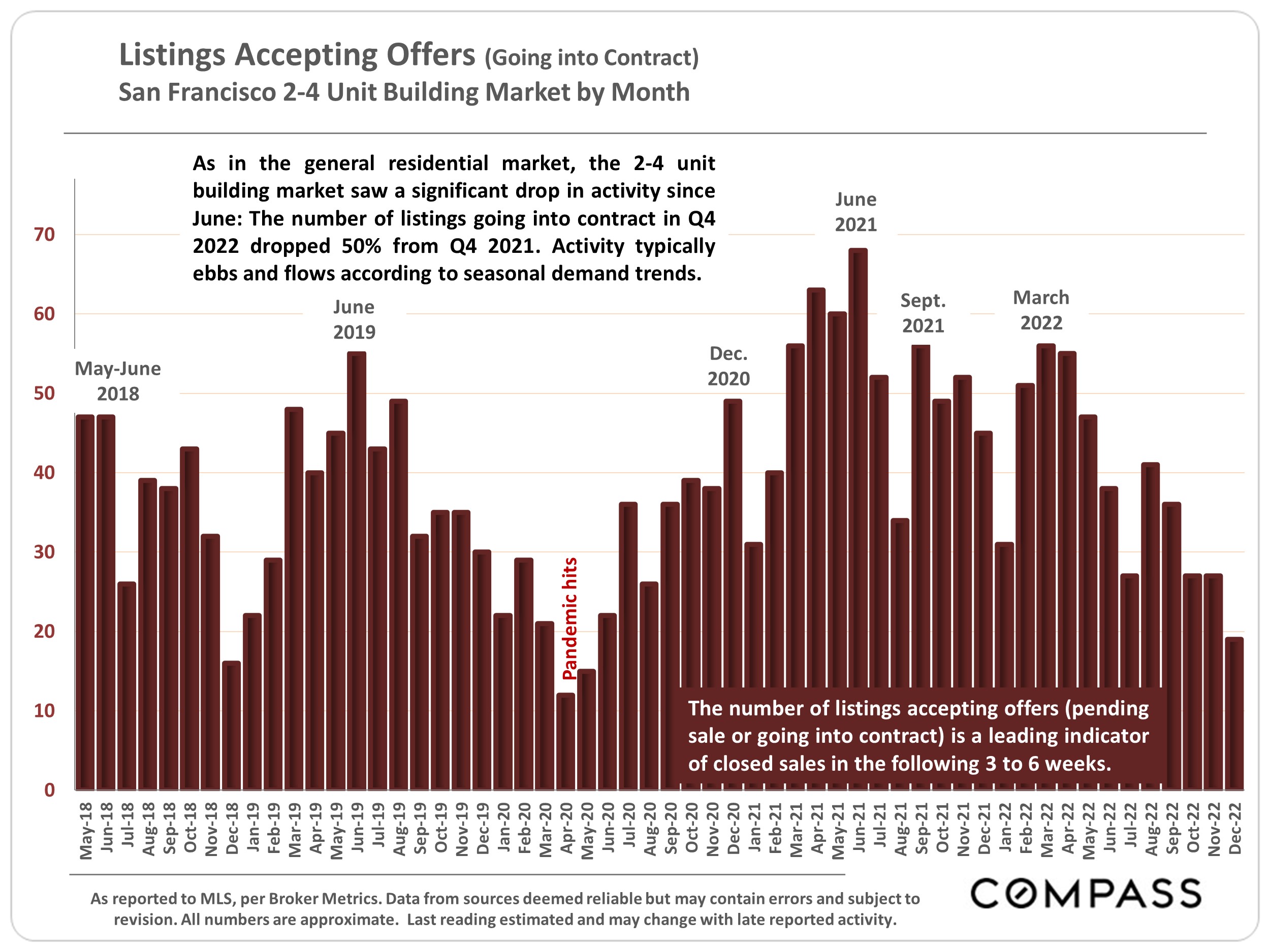

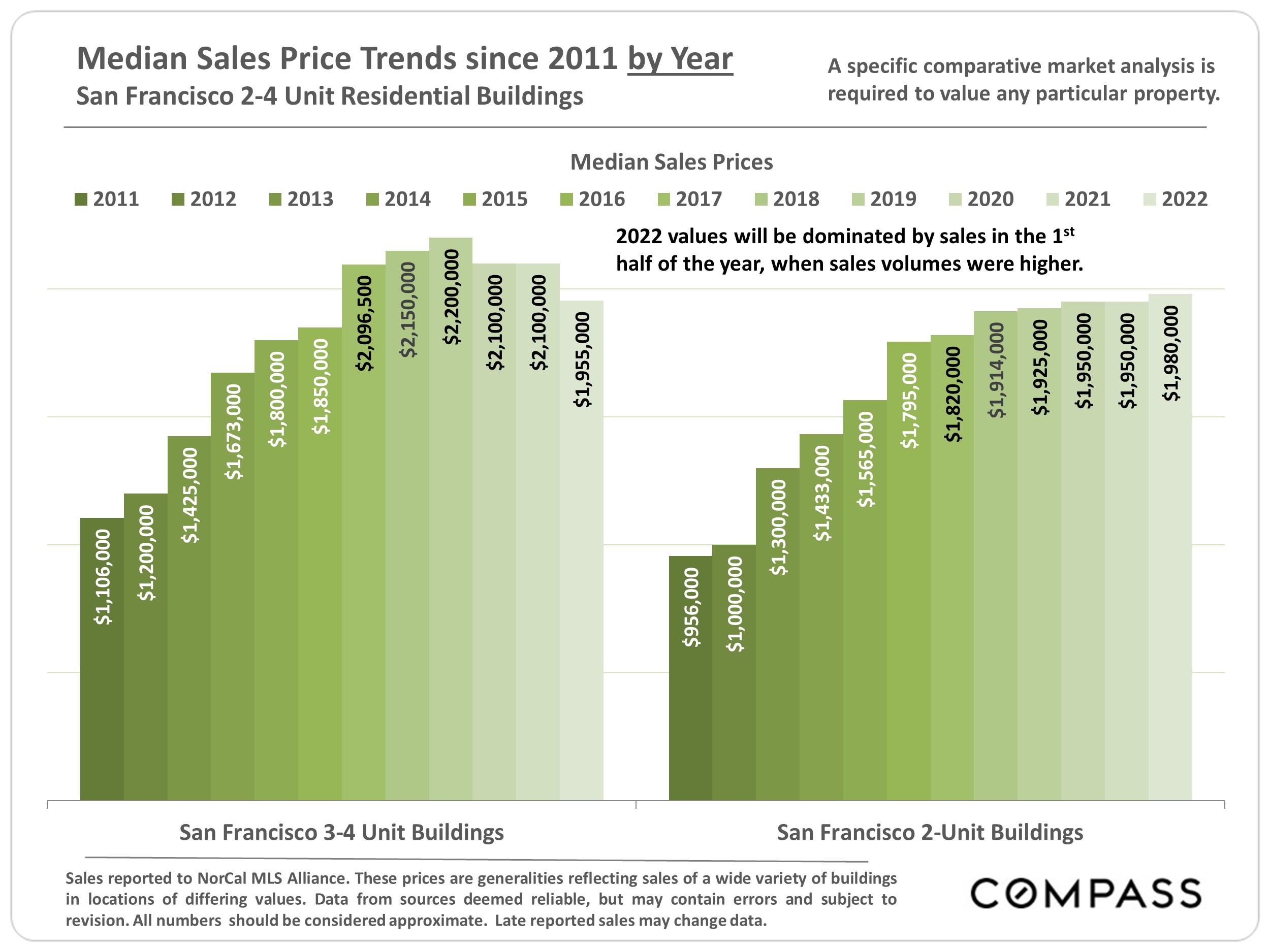

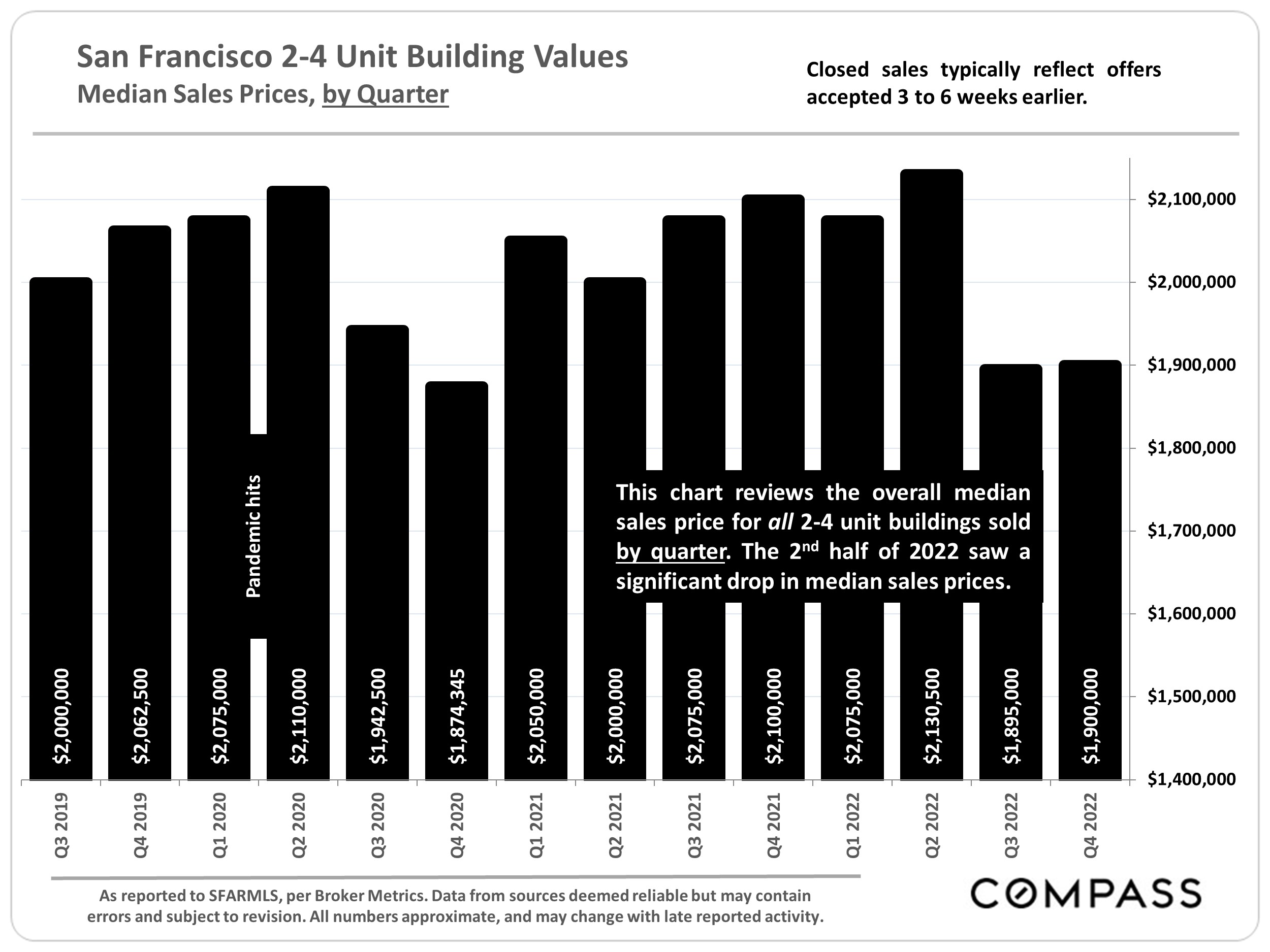

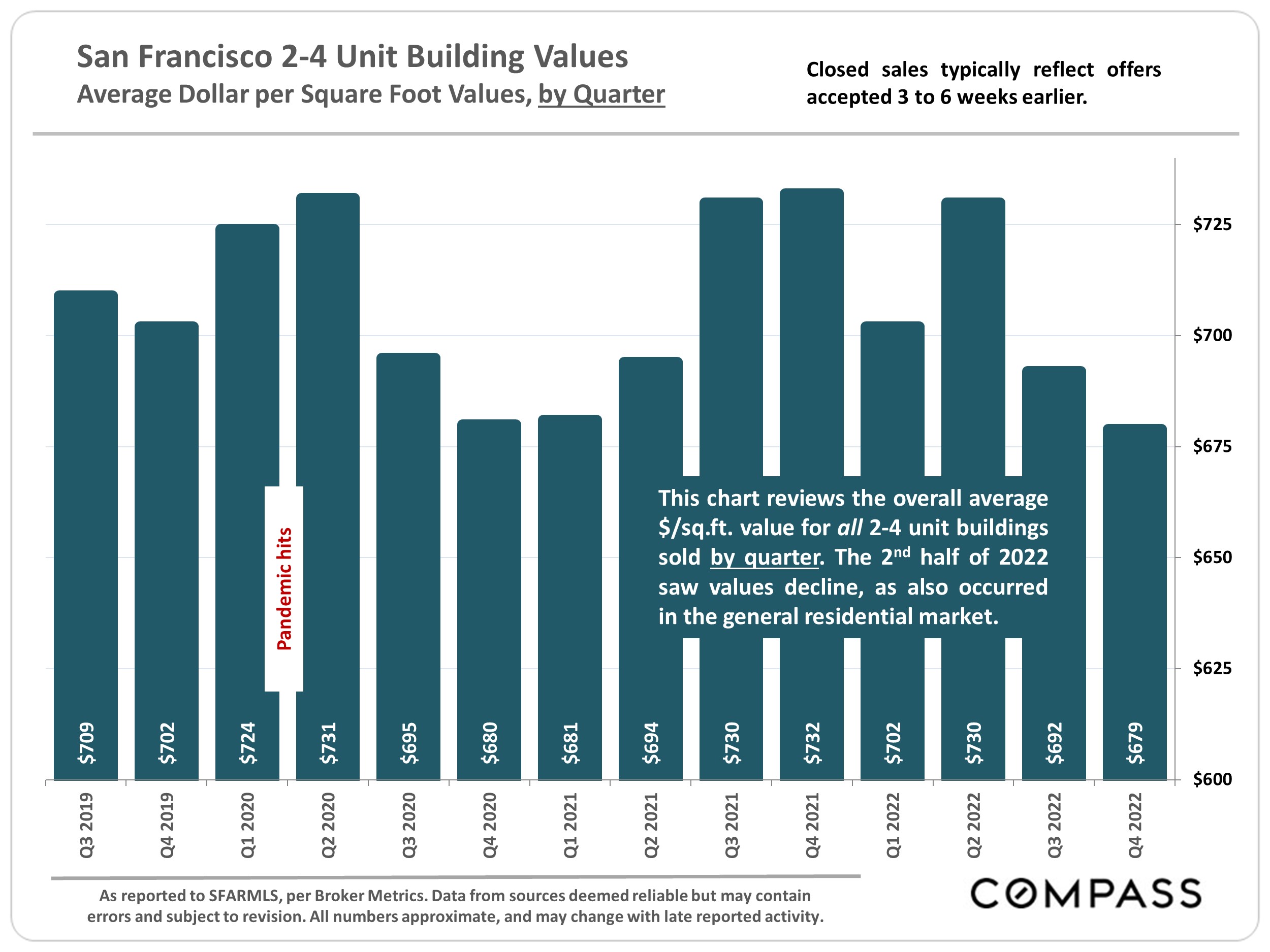

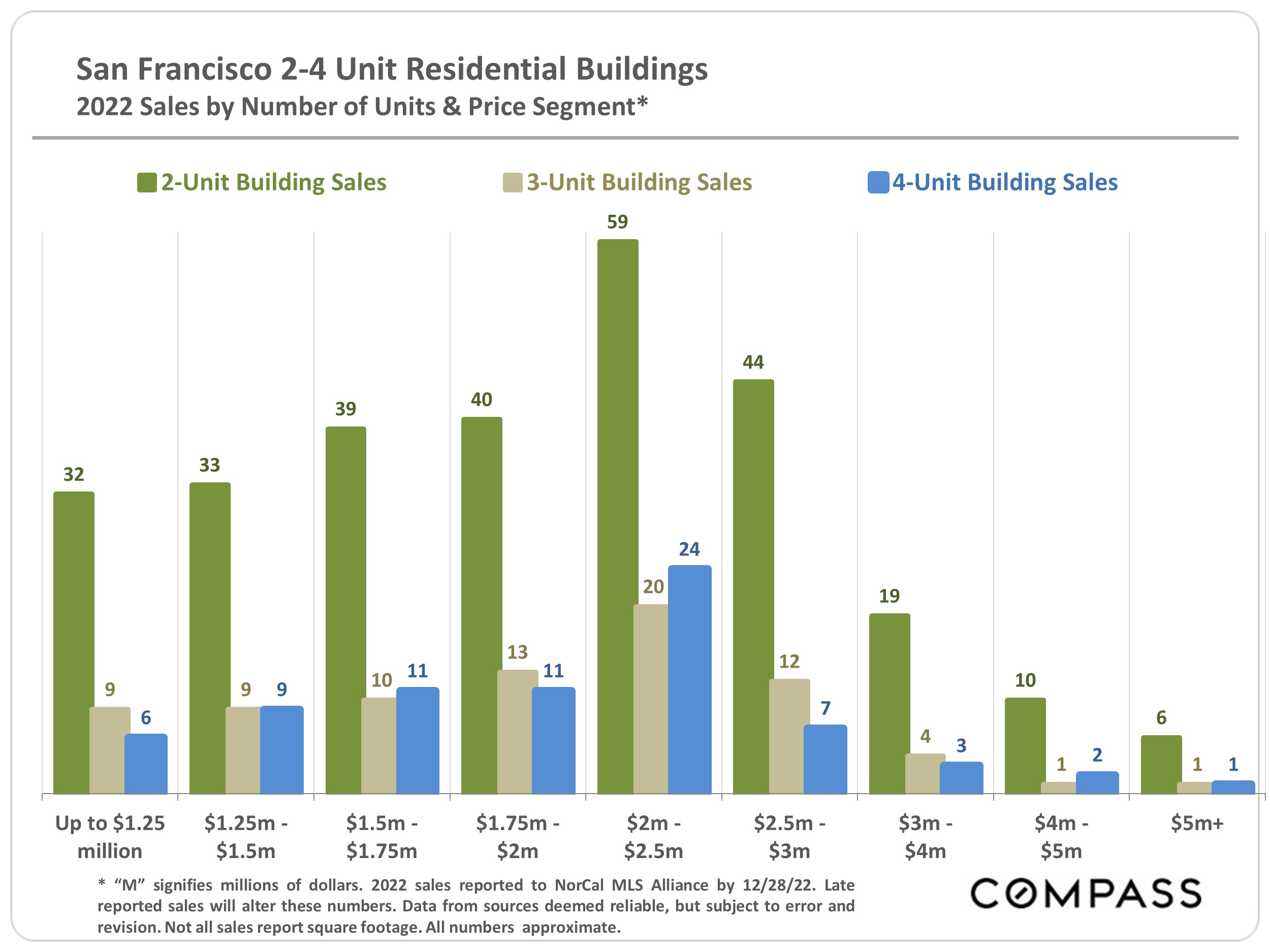

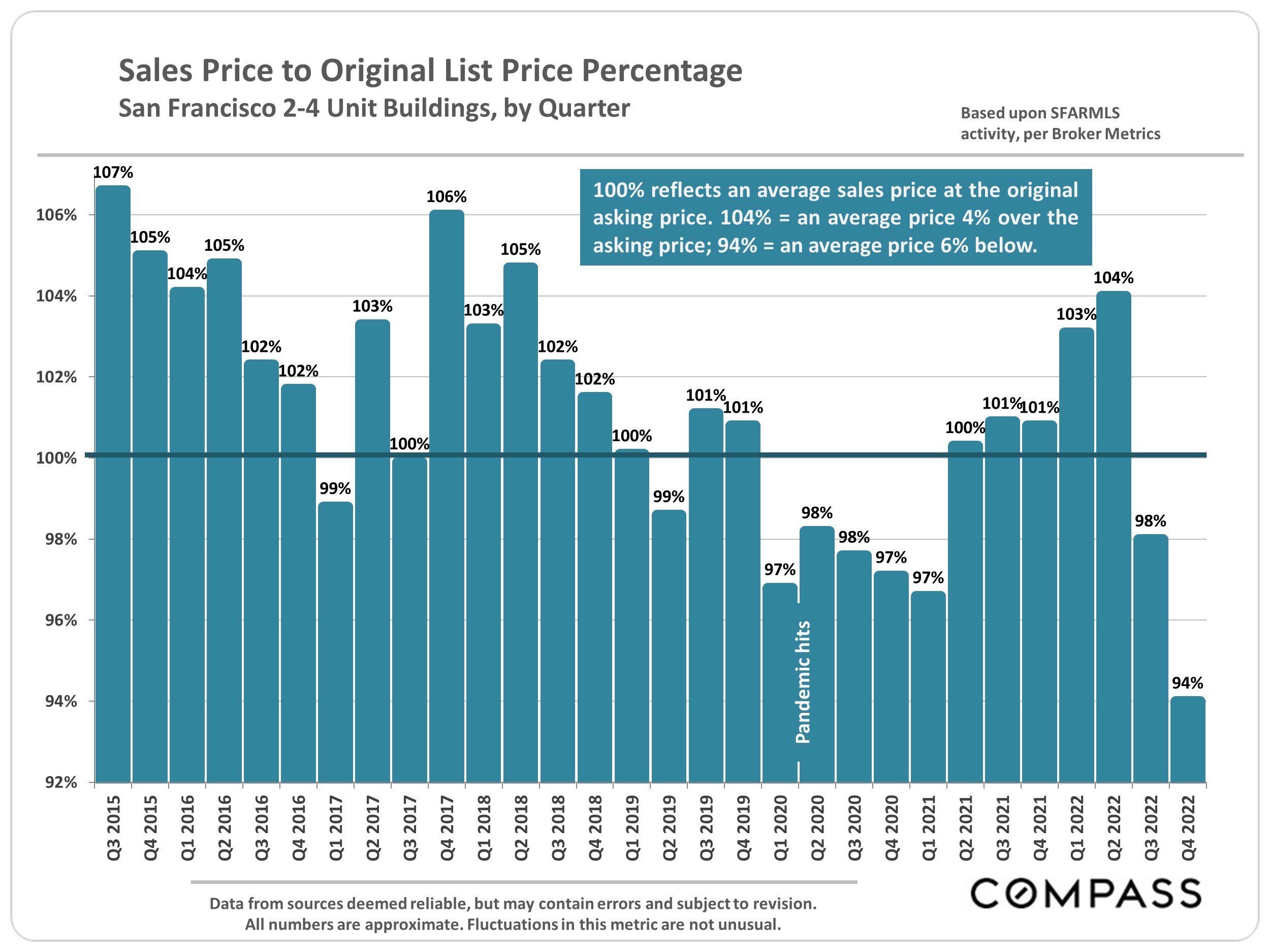

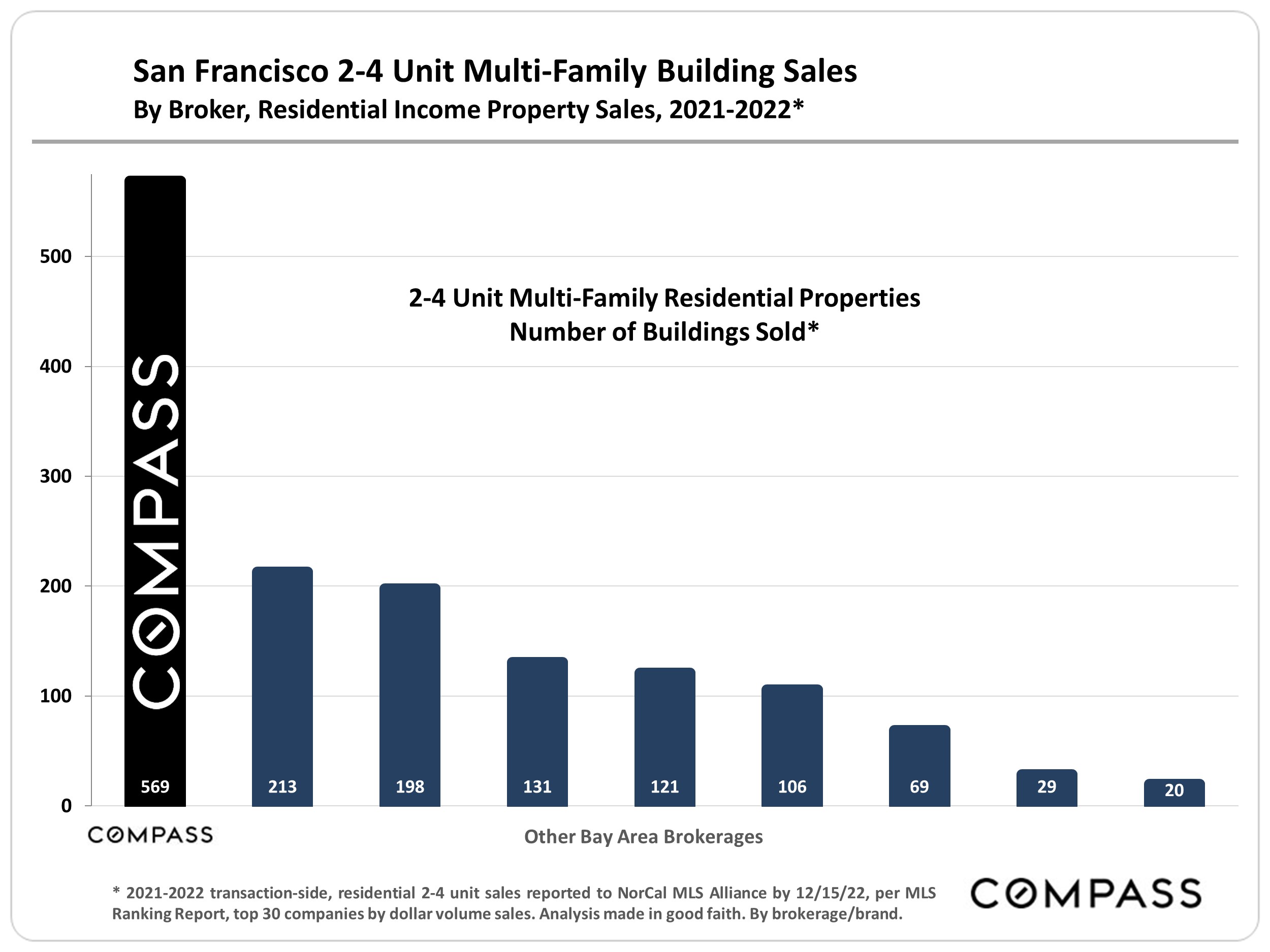

In the second half of 2022, sales volumes and values dropped in the residential income segment, paralleling similar changes in the general residential market. However, hundreds of apartment buildings continued to change hands, as buyers sought out good values and premium properties. Correct pricing is more important than ever. Average asking rents climbed in the first half of 2022, but declined in the second – ending up a little higher than where the year began, but still well down from early 2020.

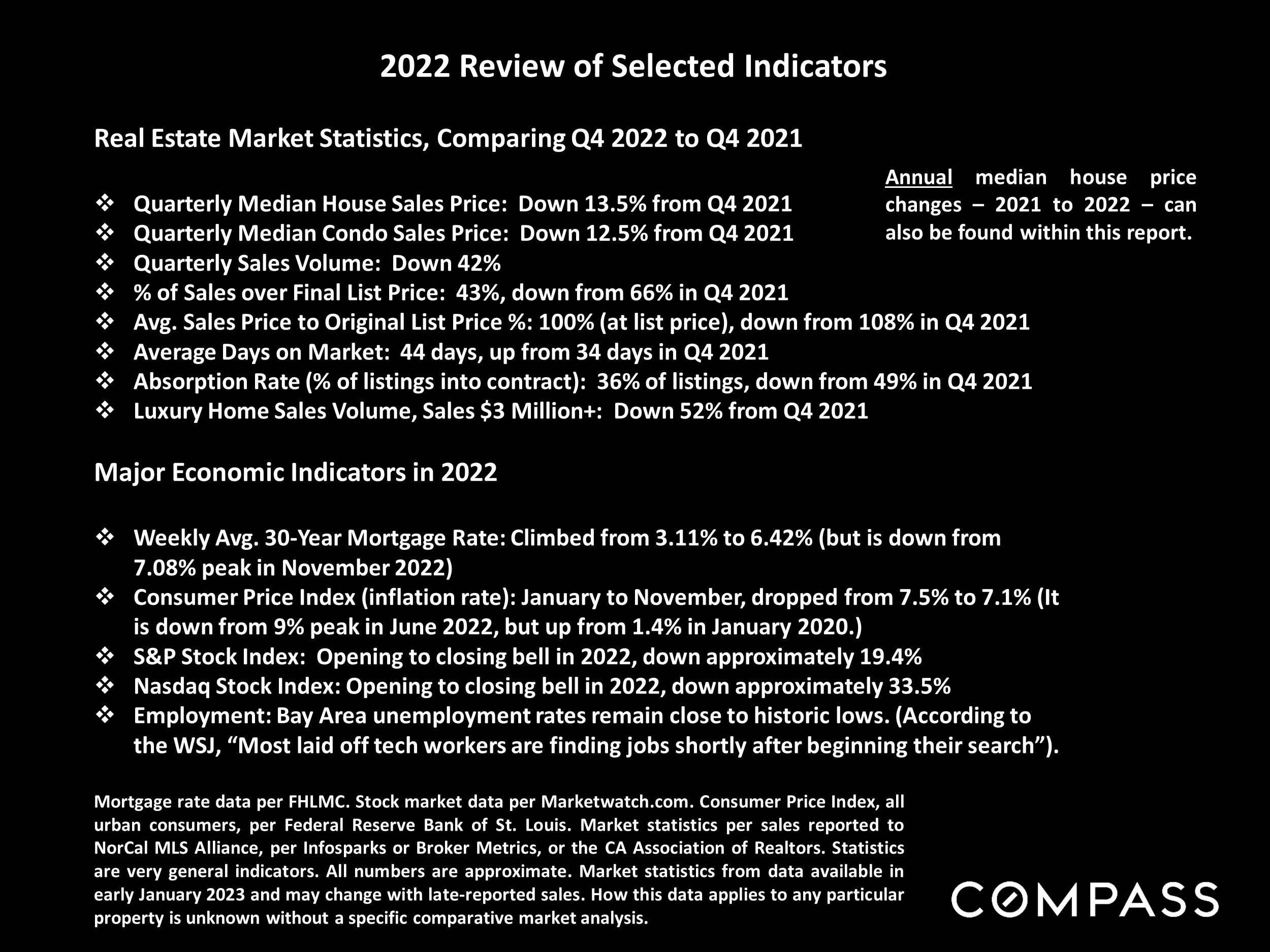

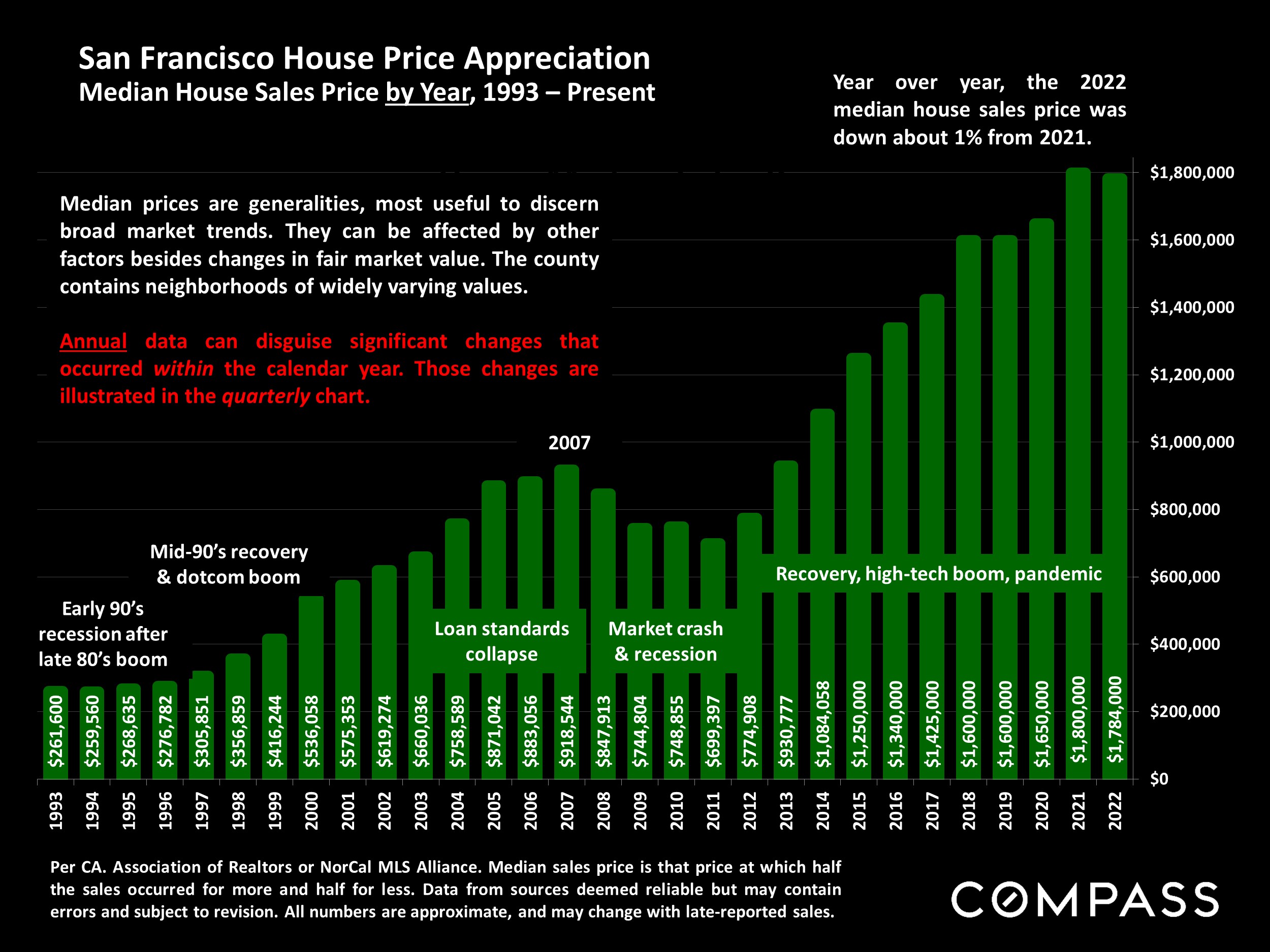

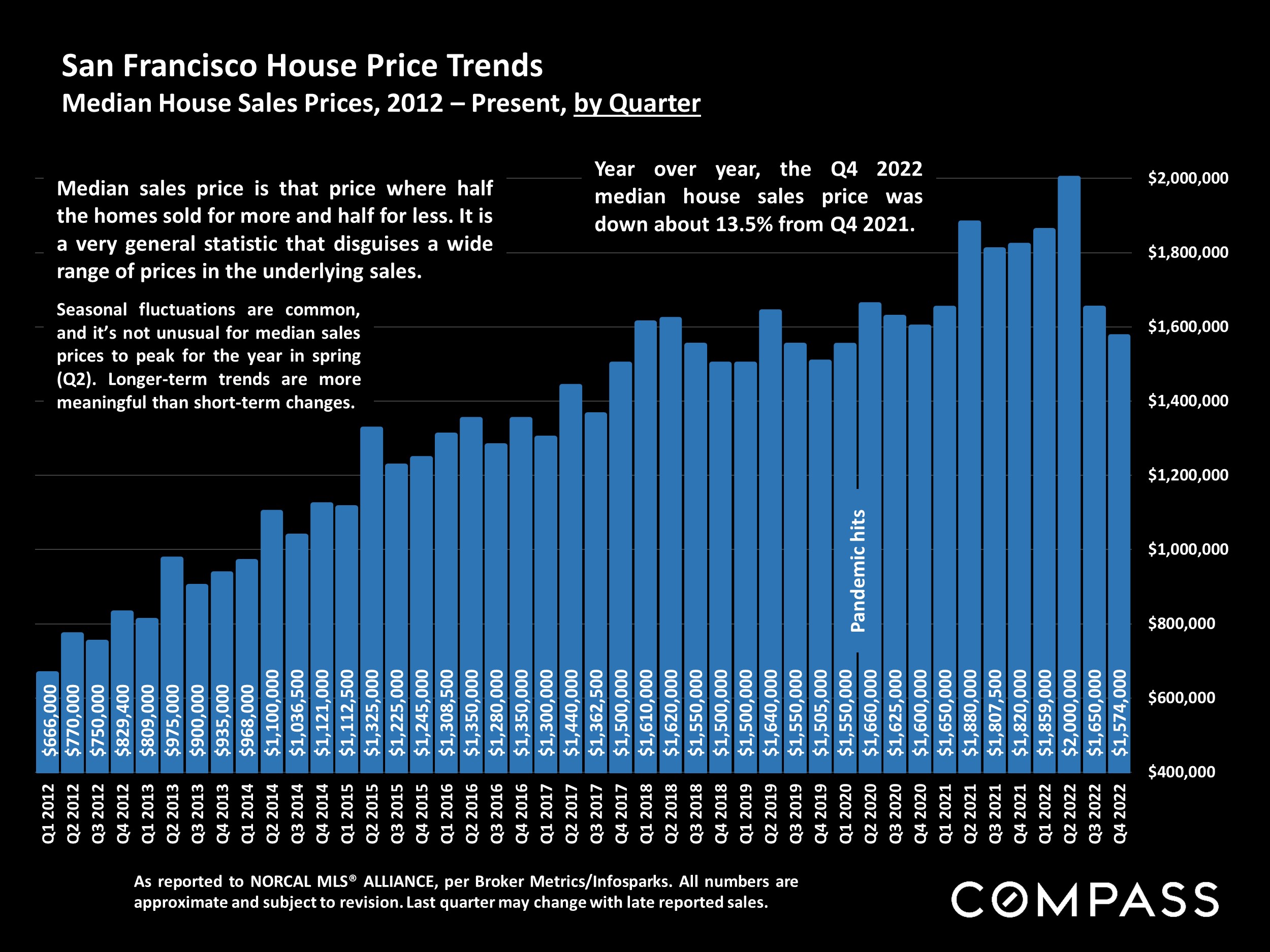

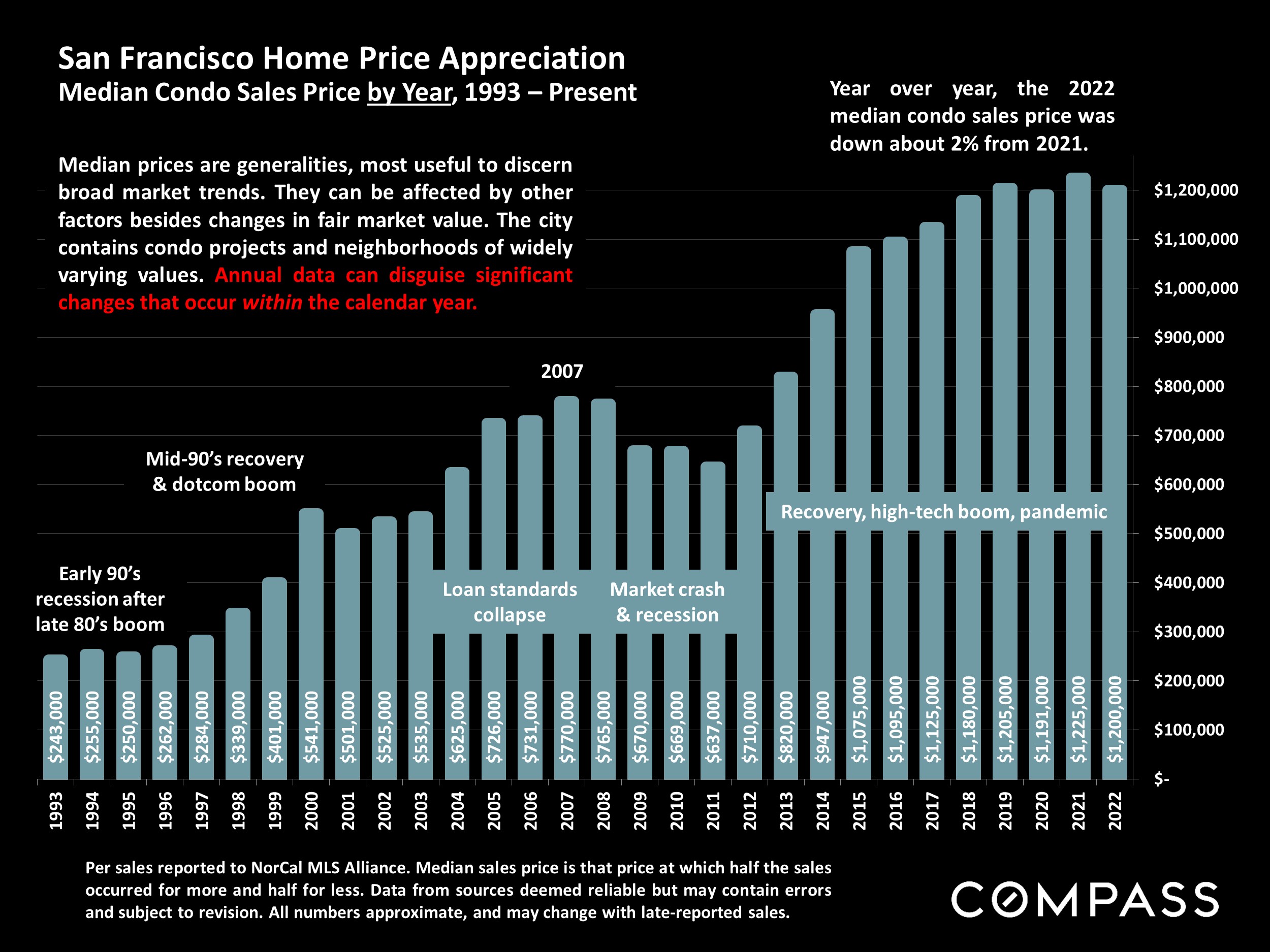

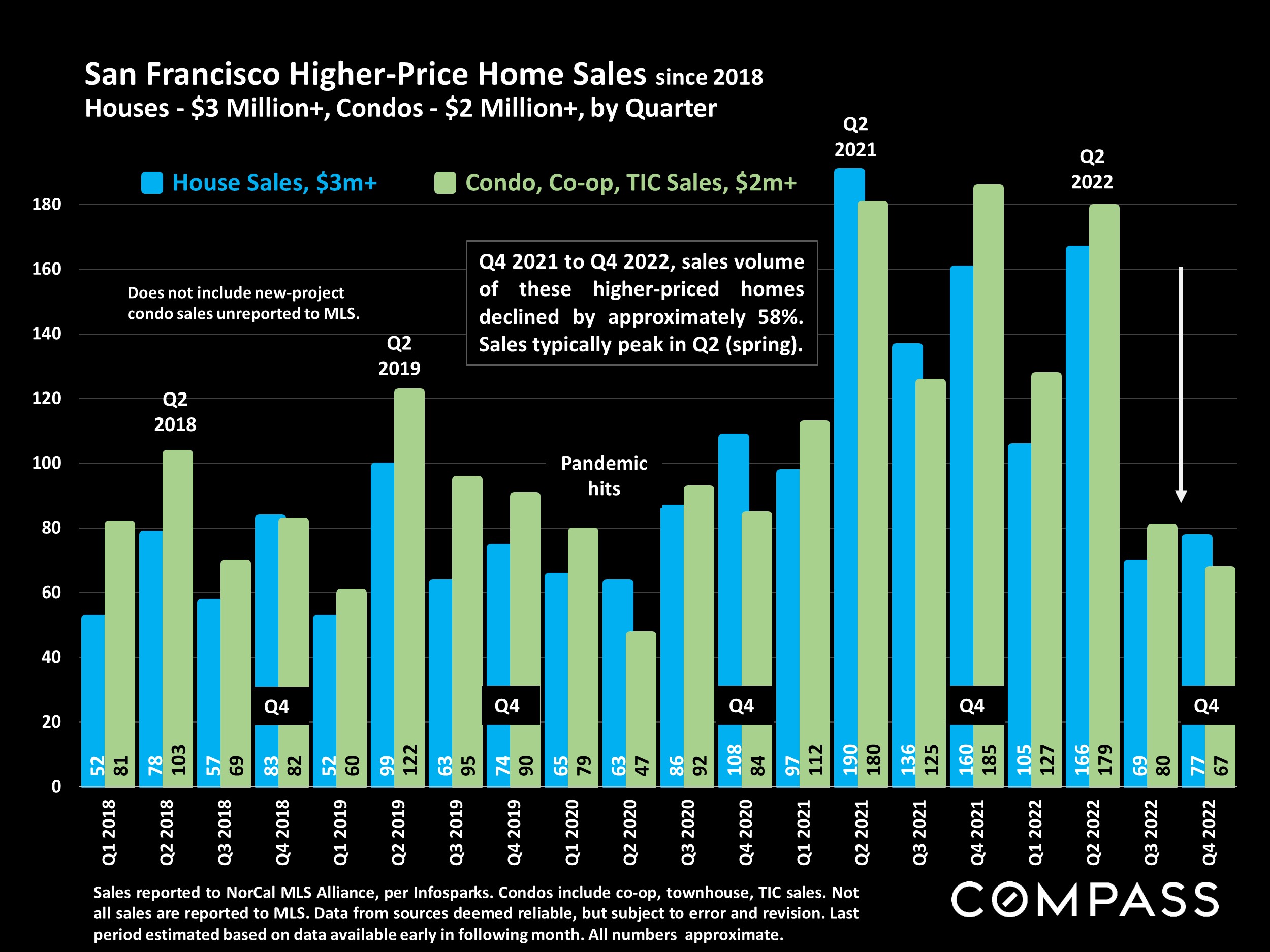

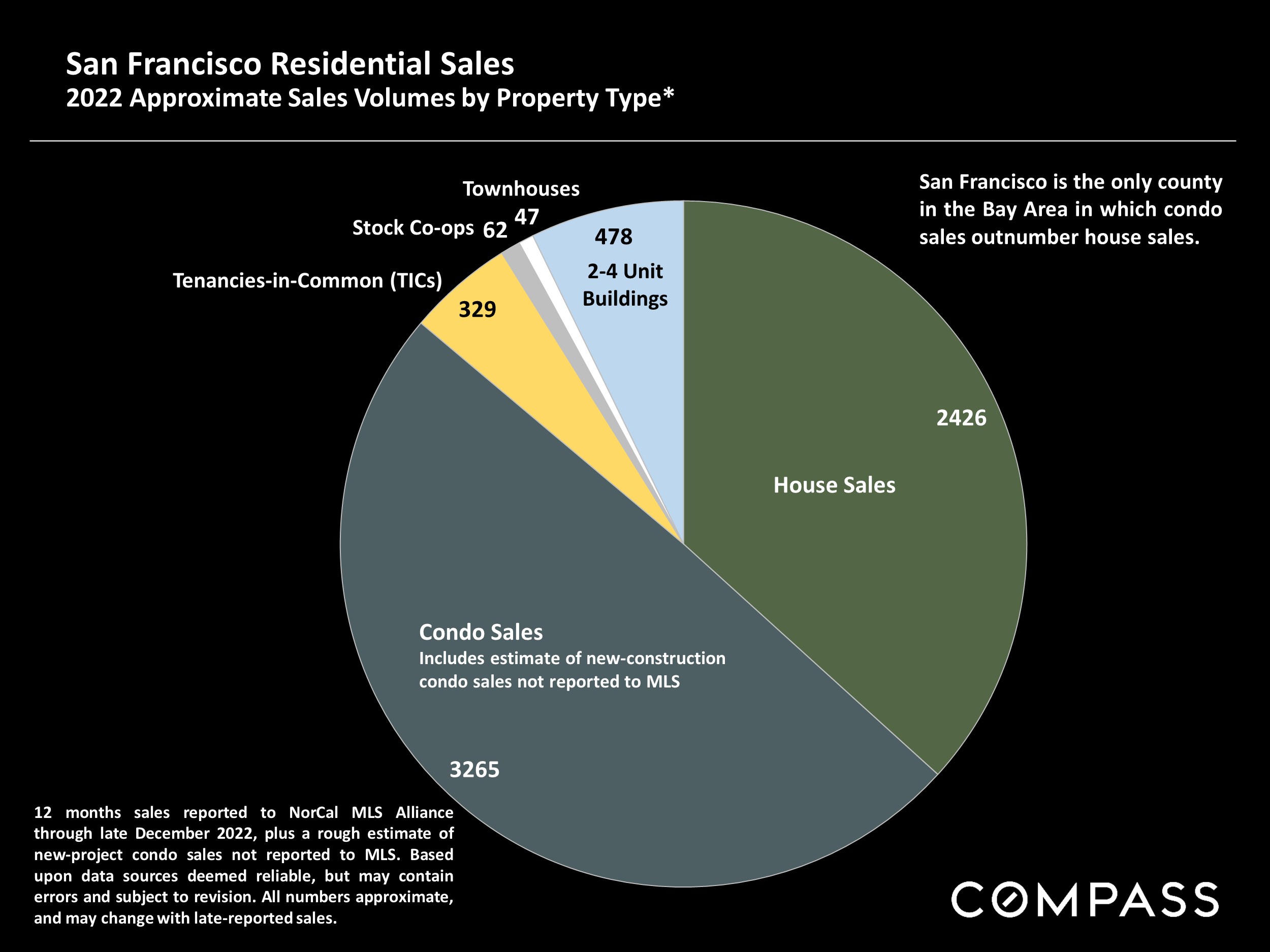

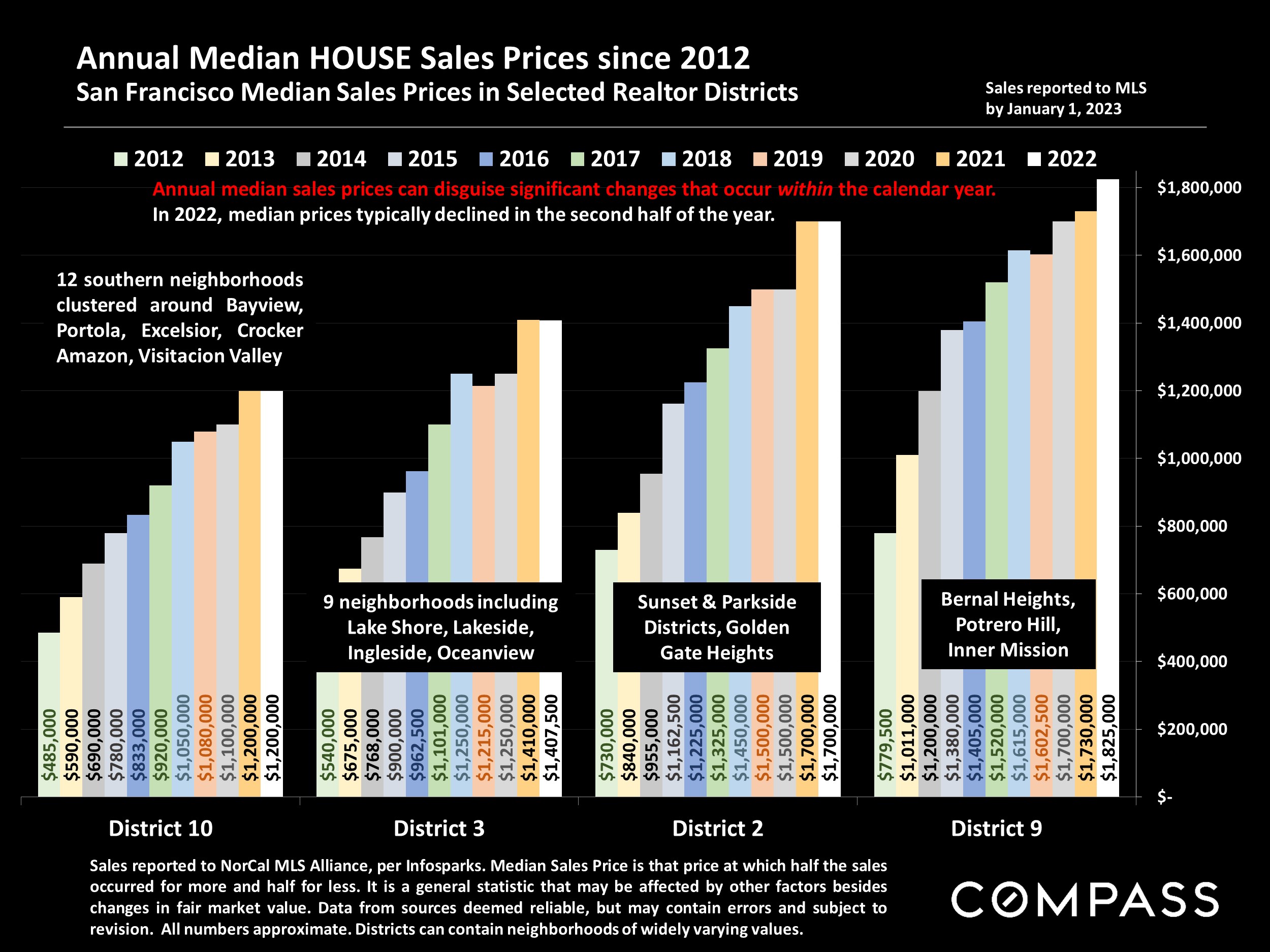

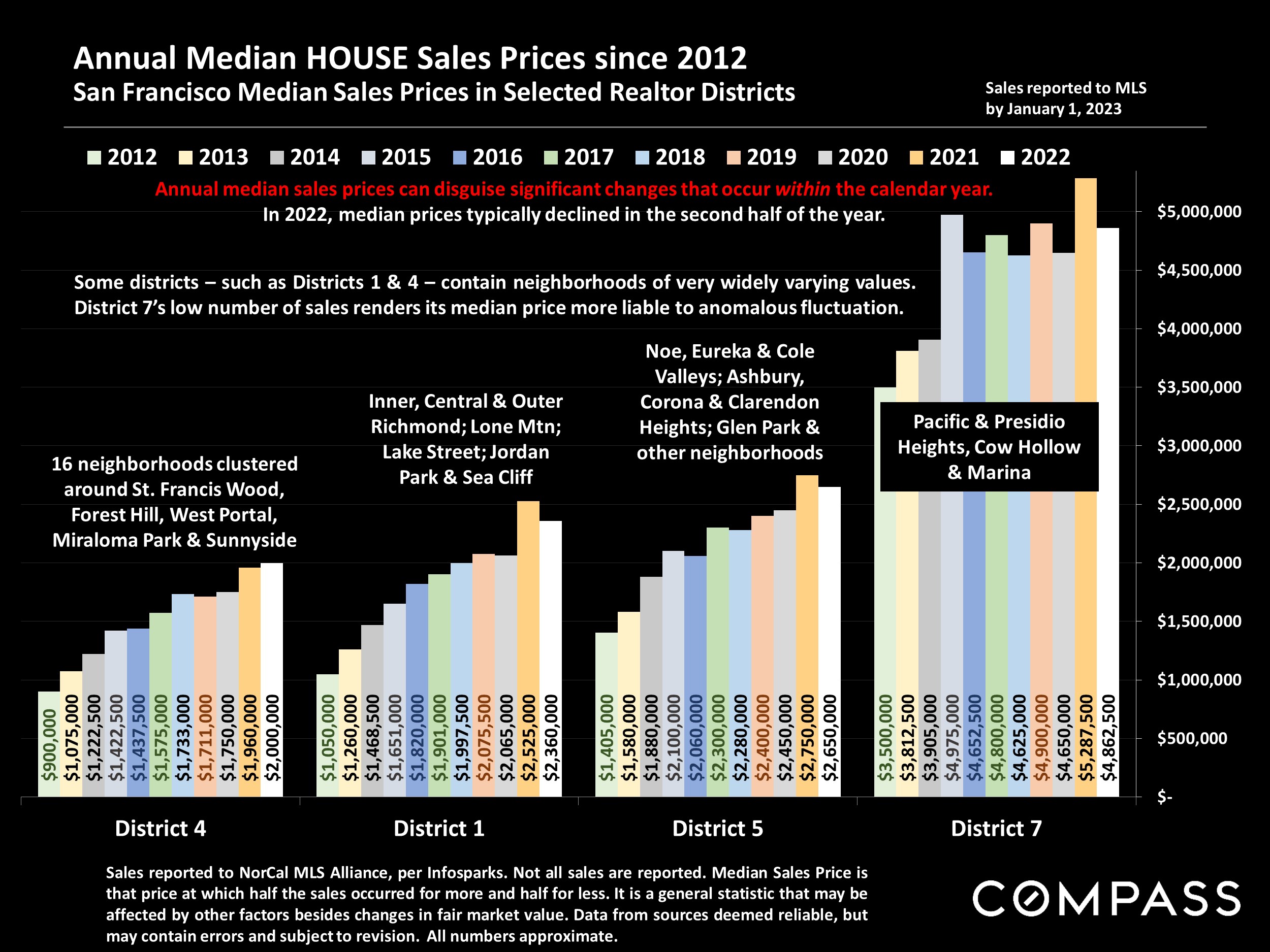

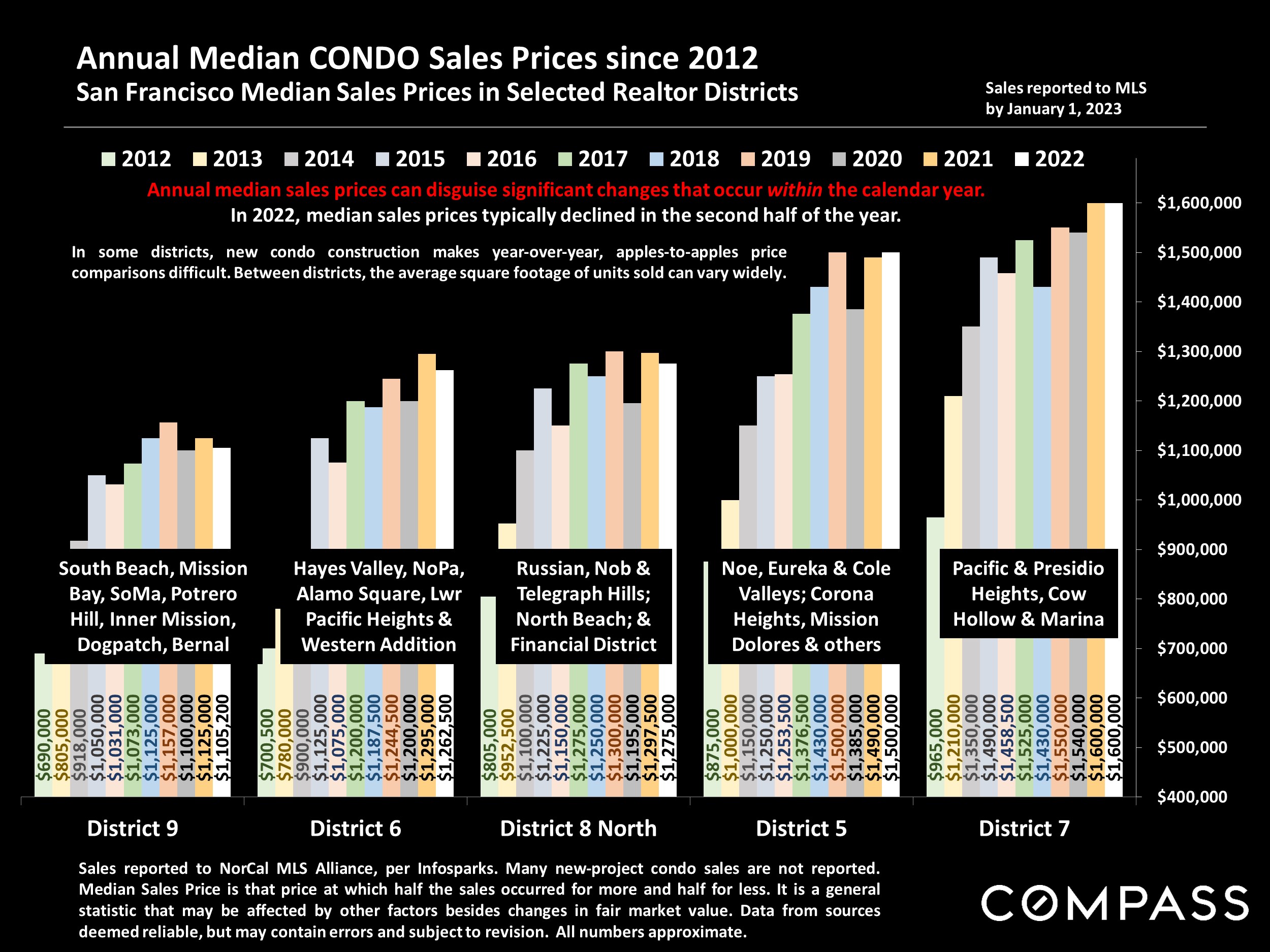

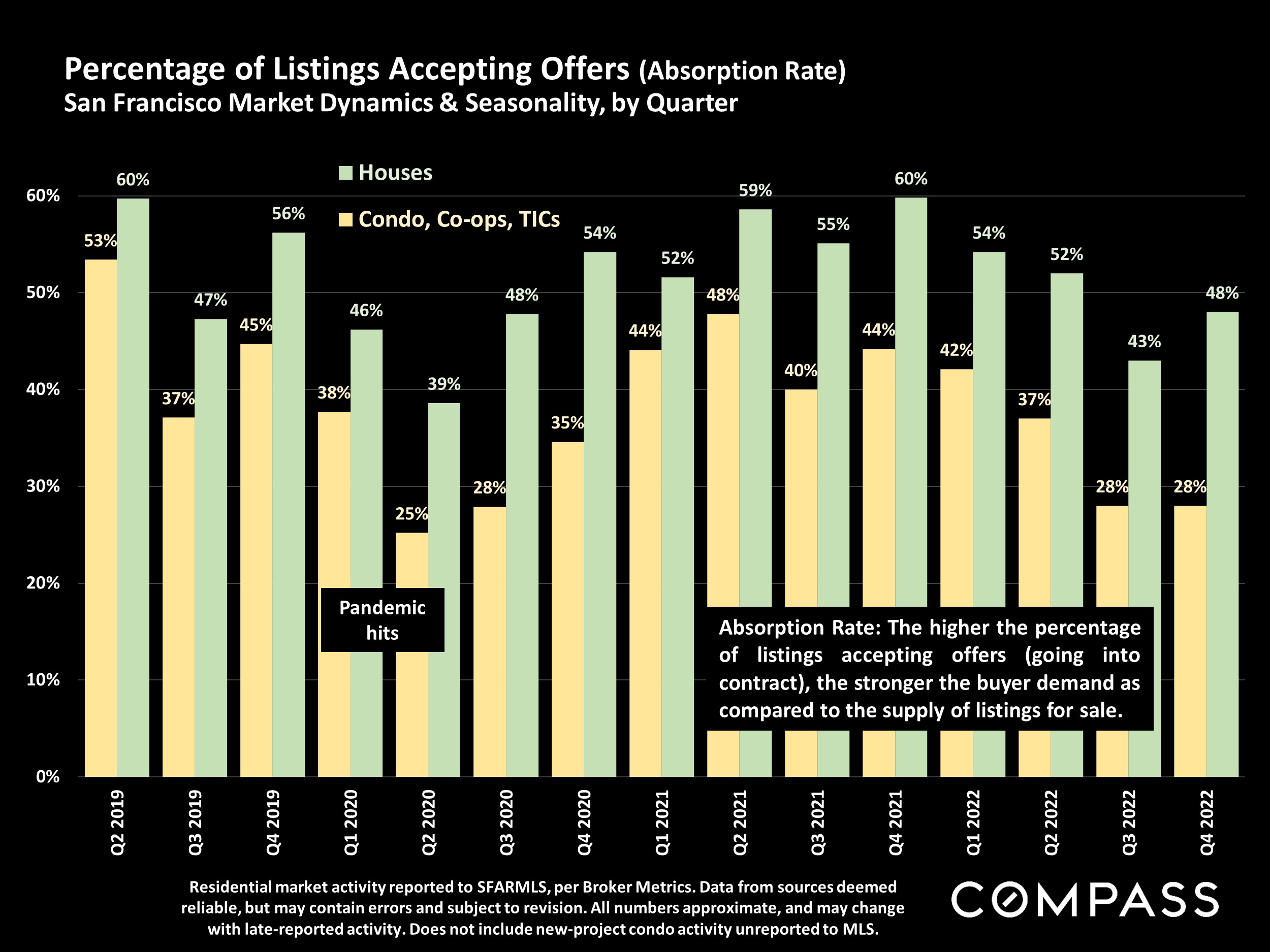

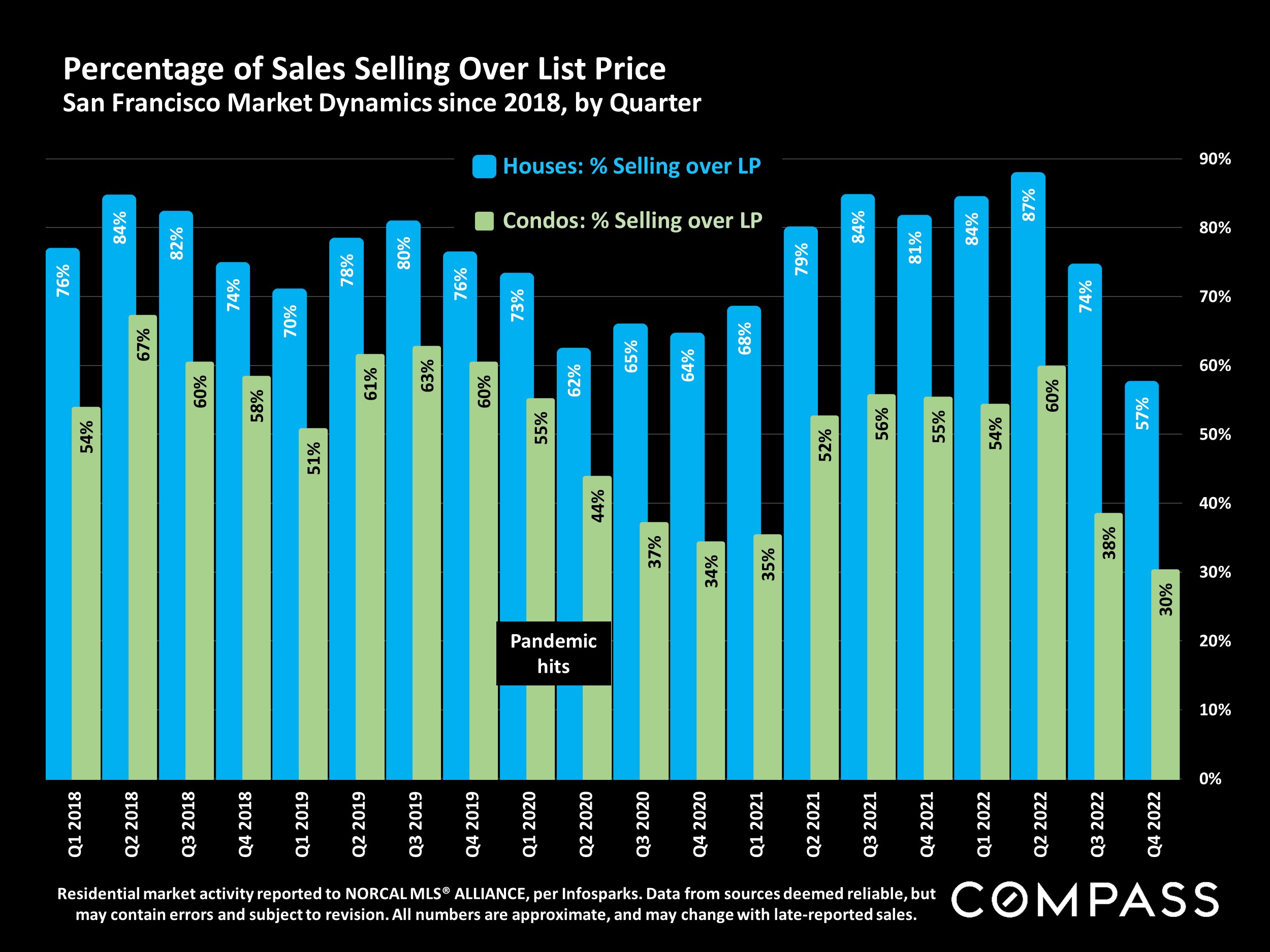

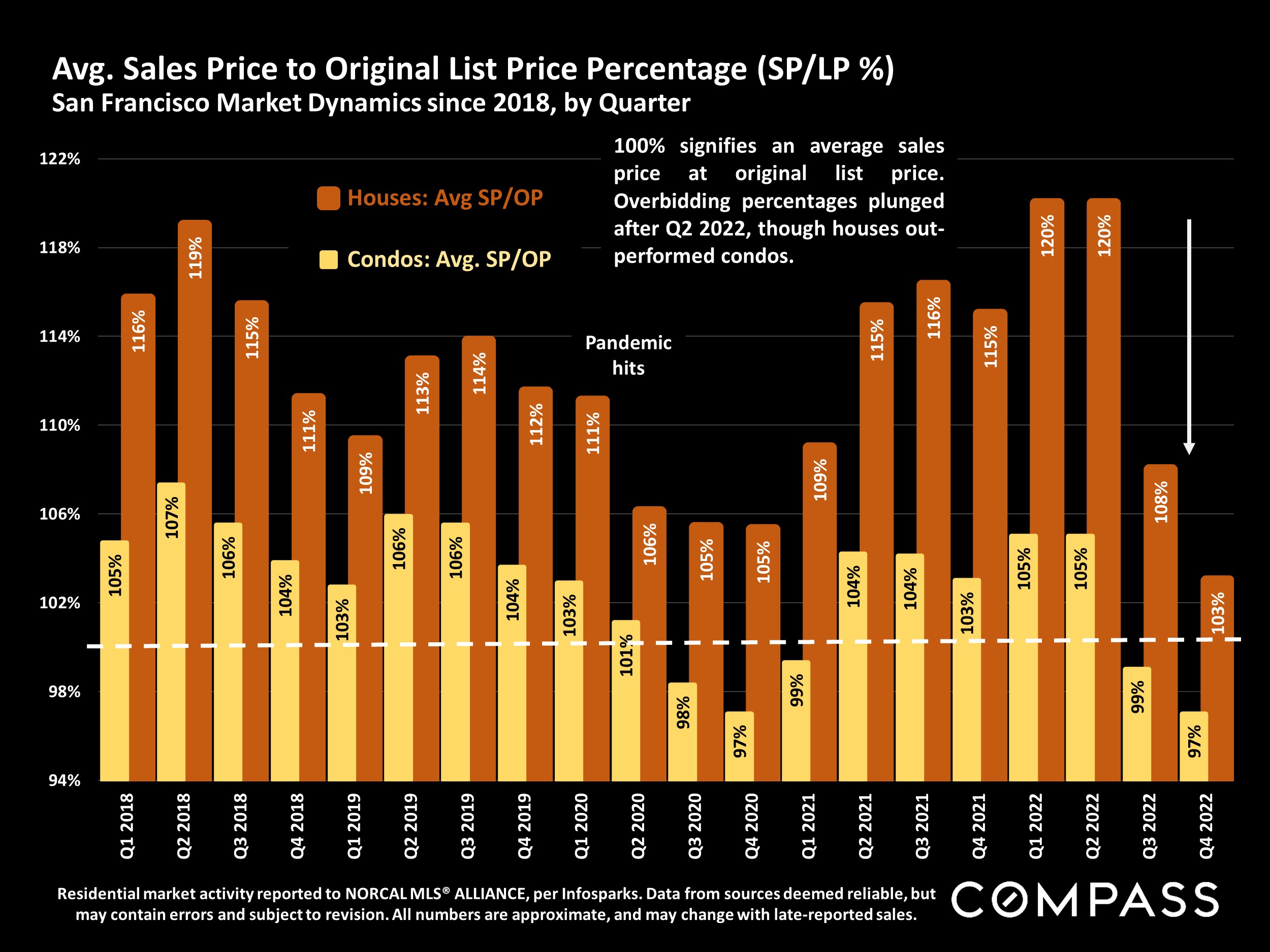

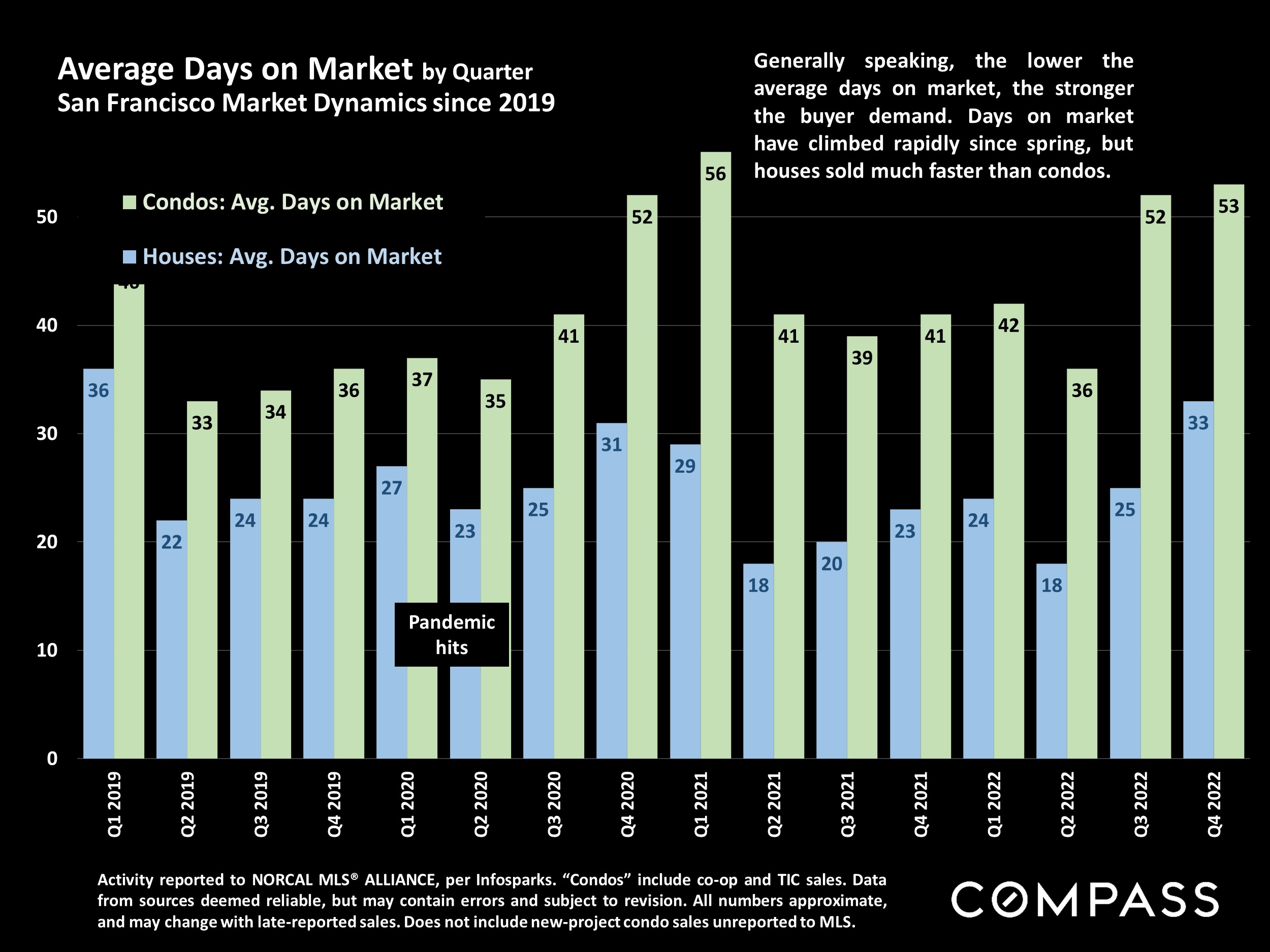

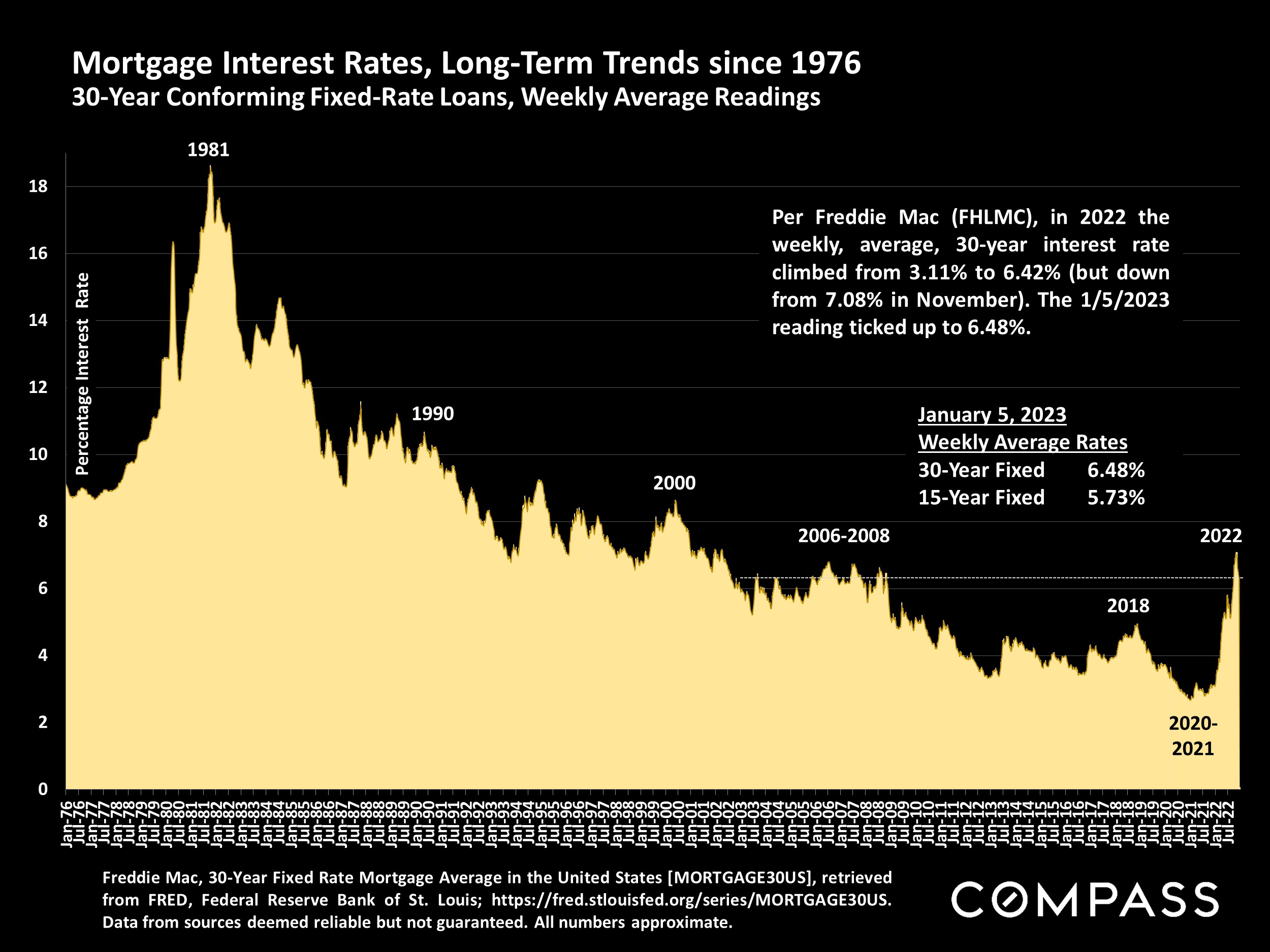

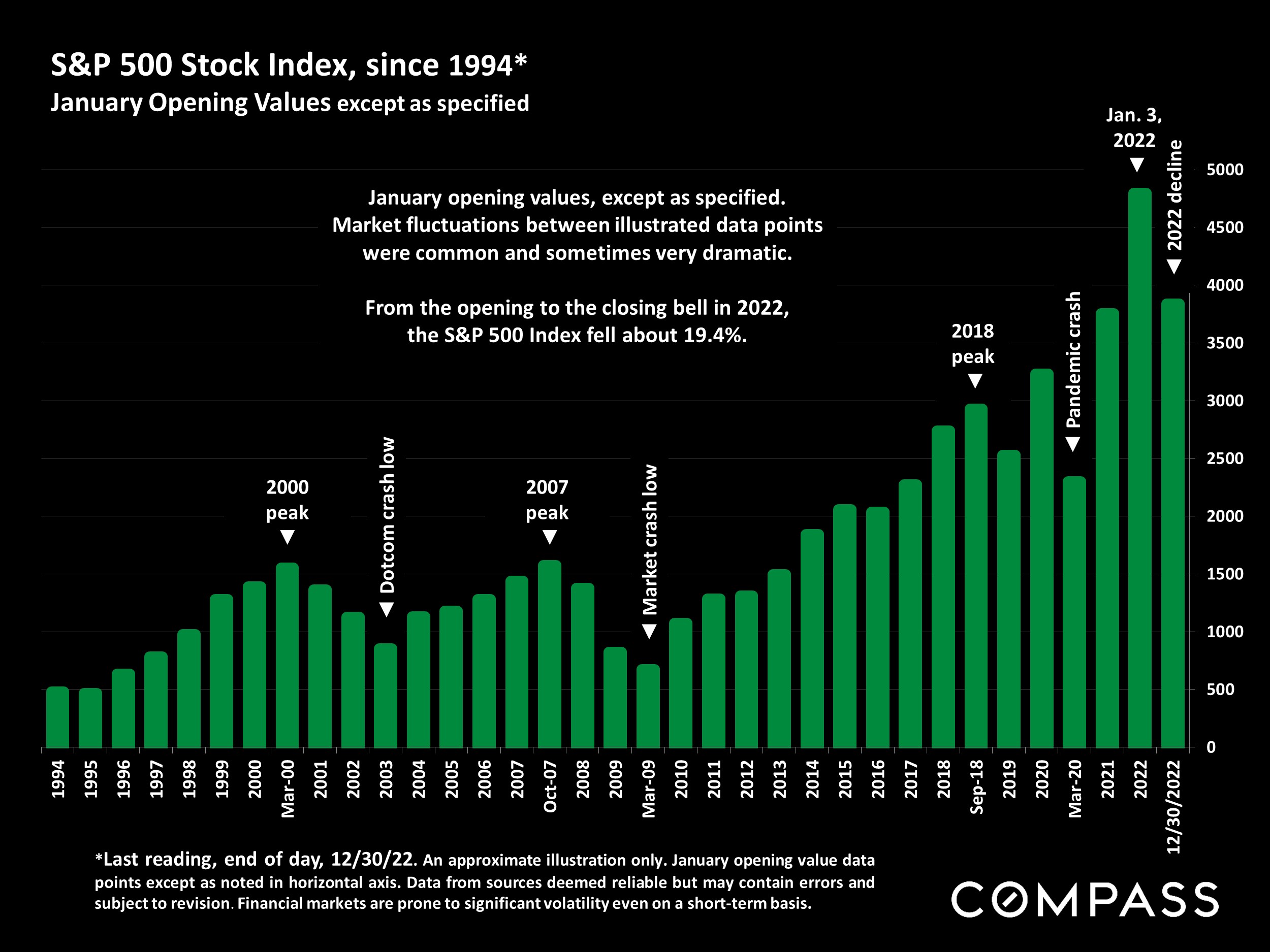

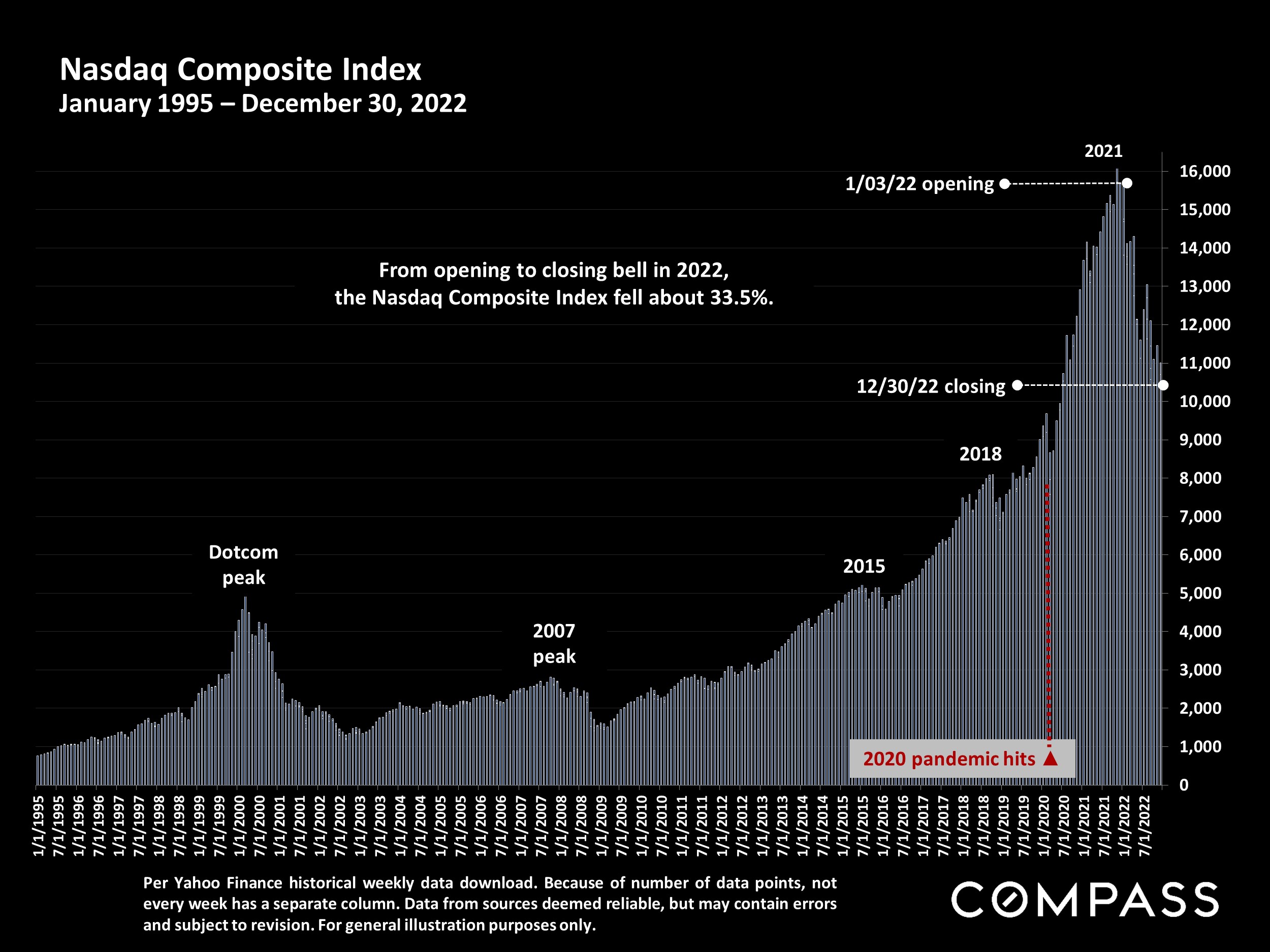

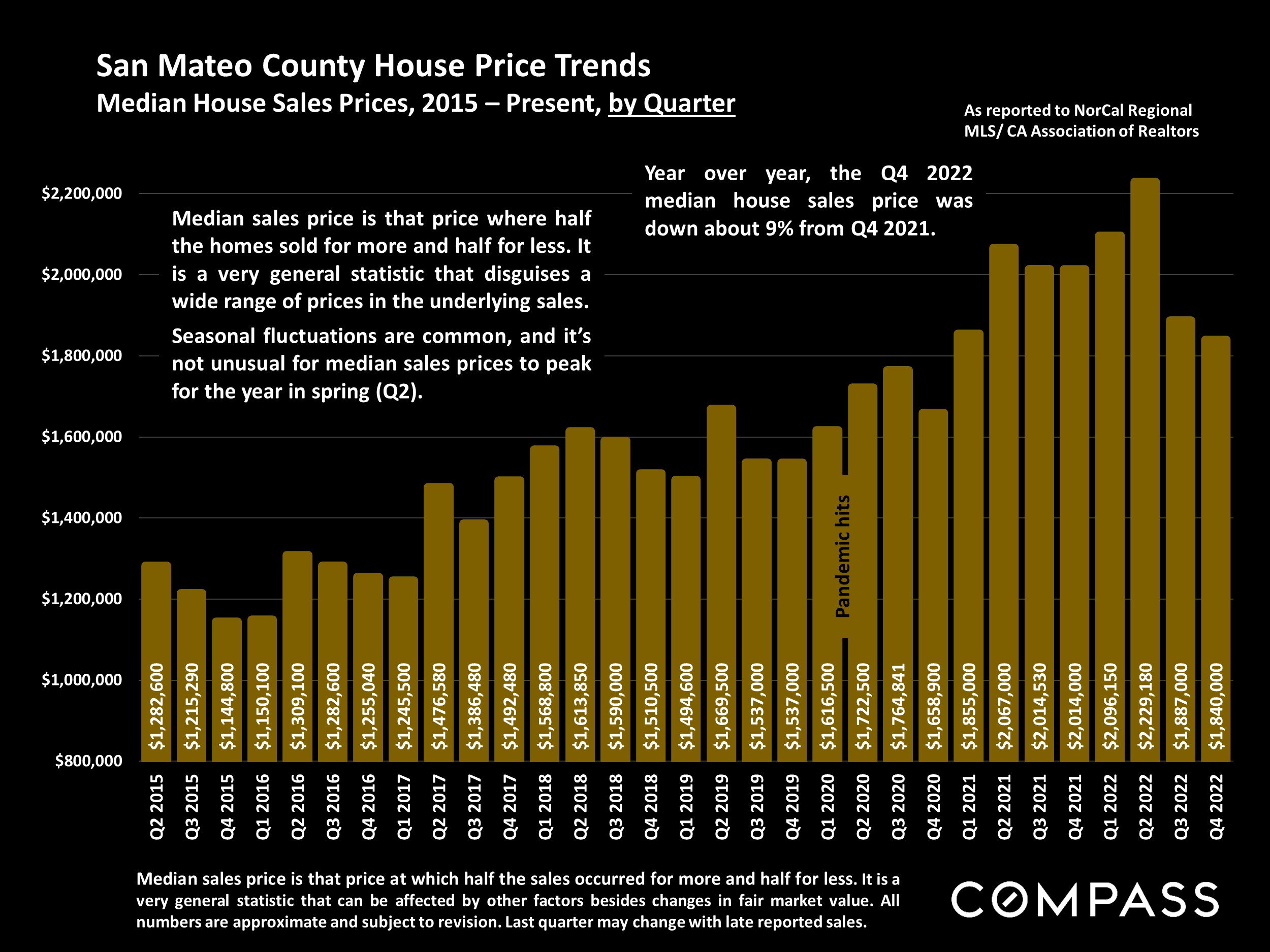

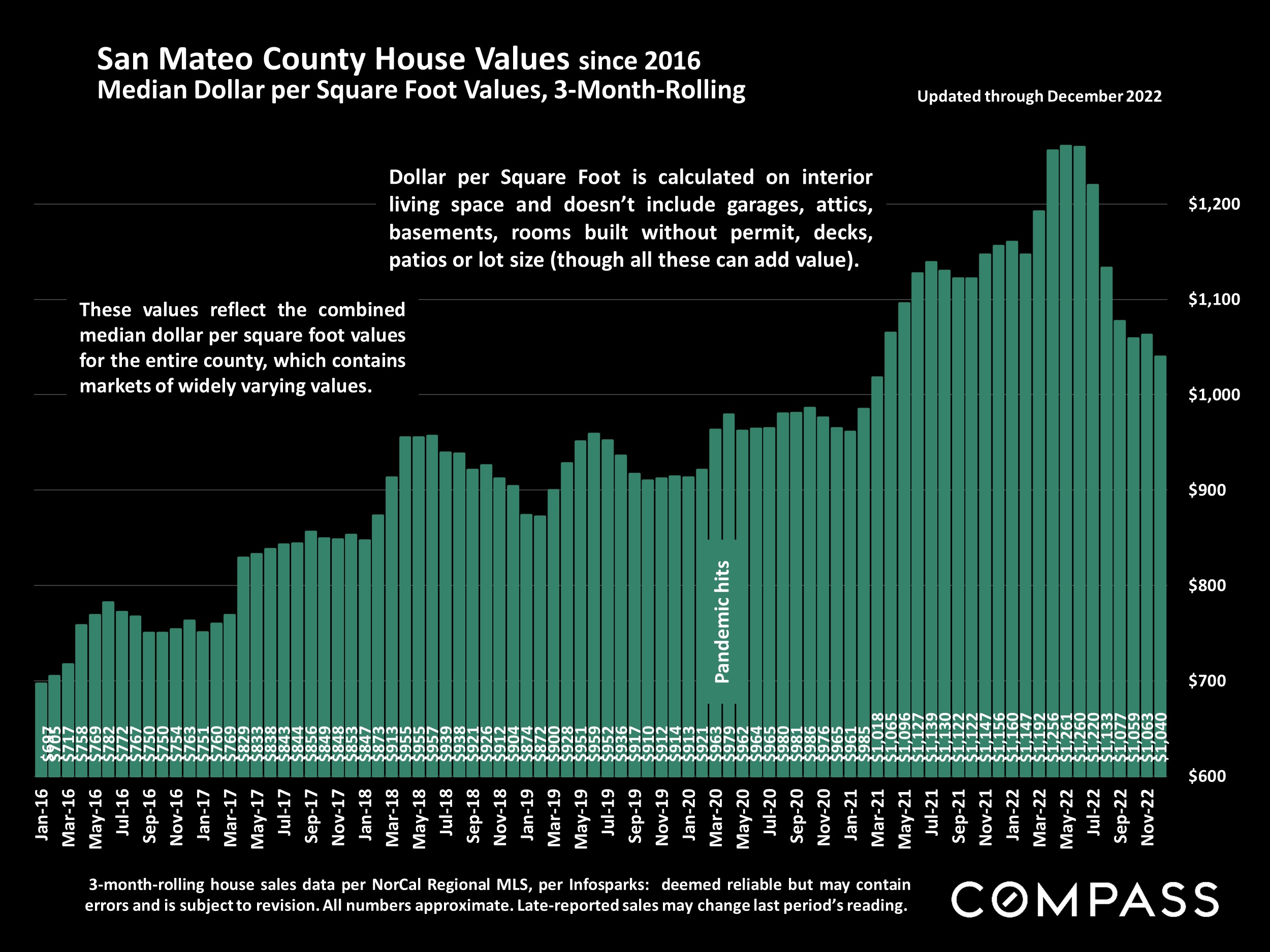

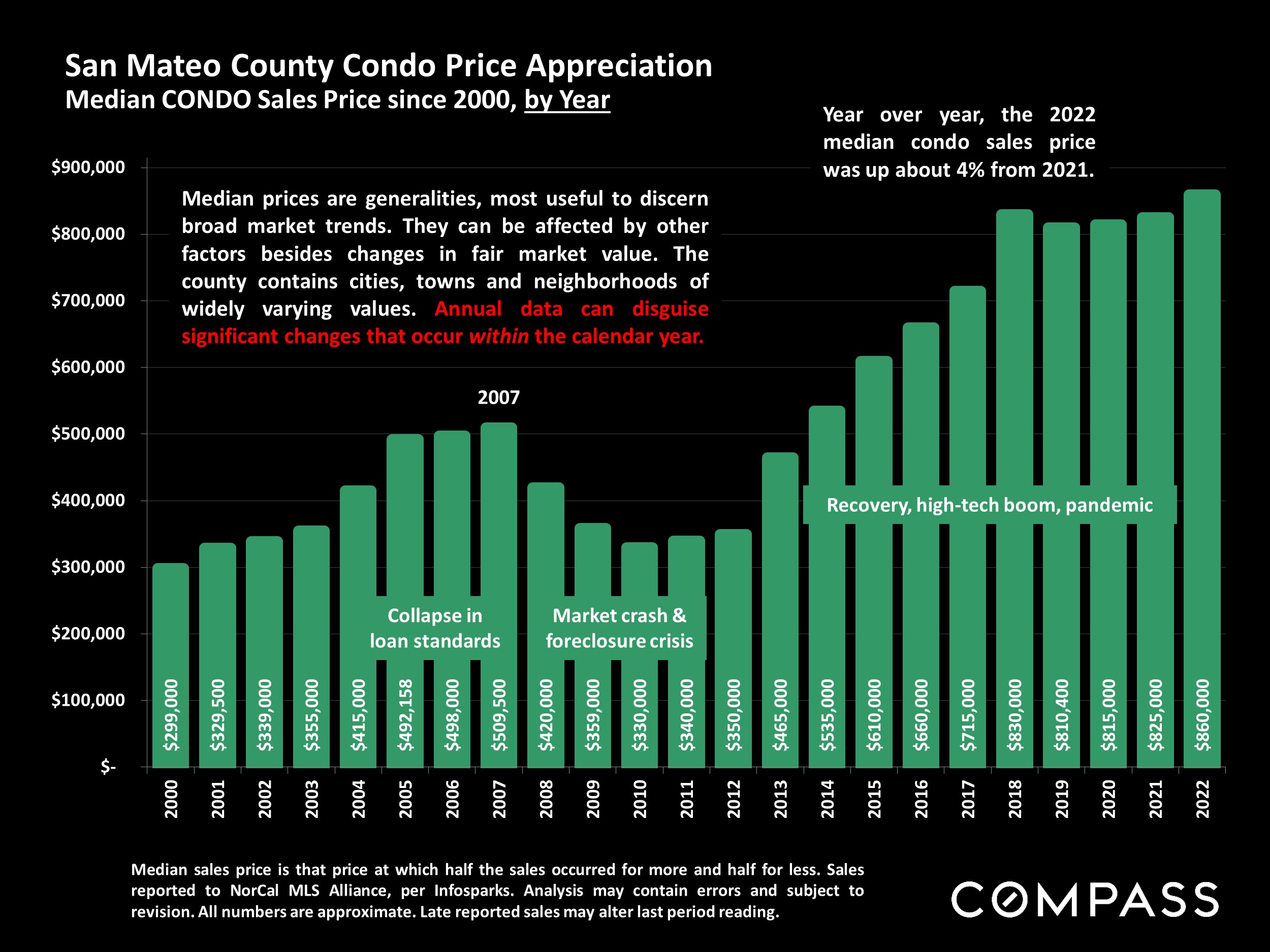

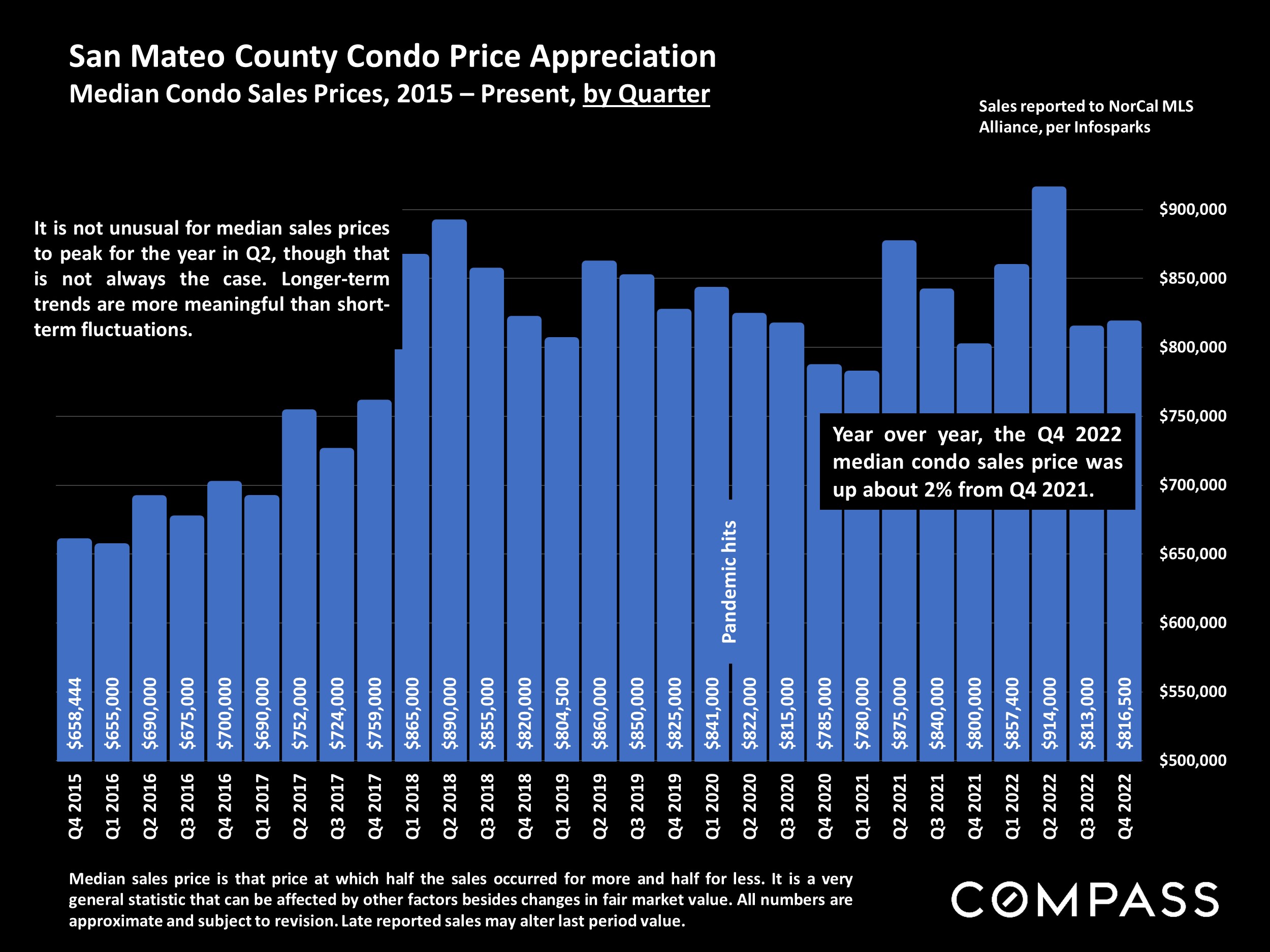

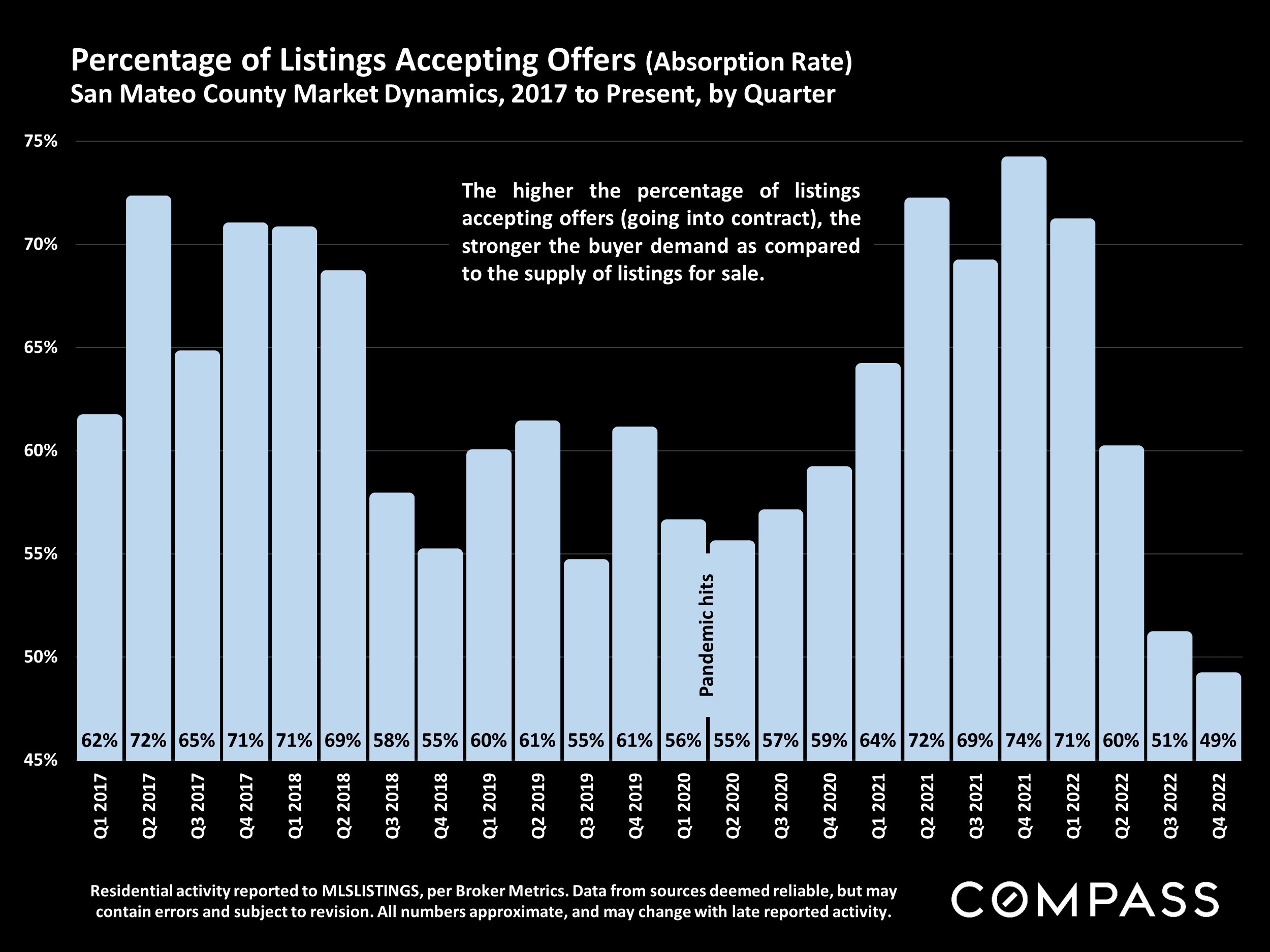

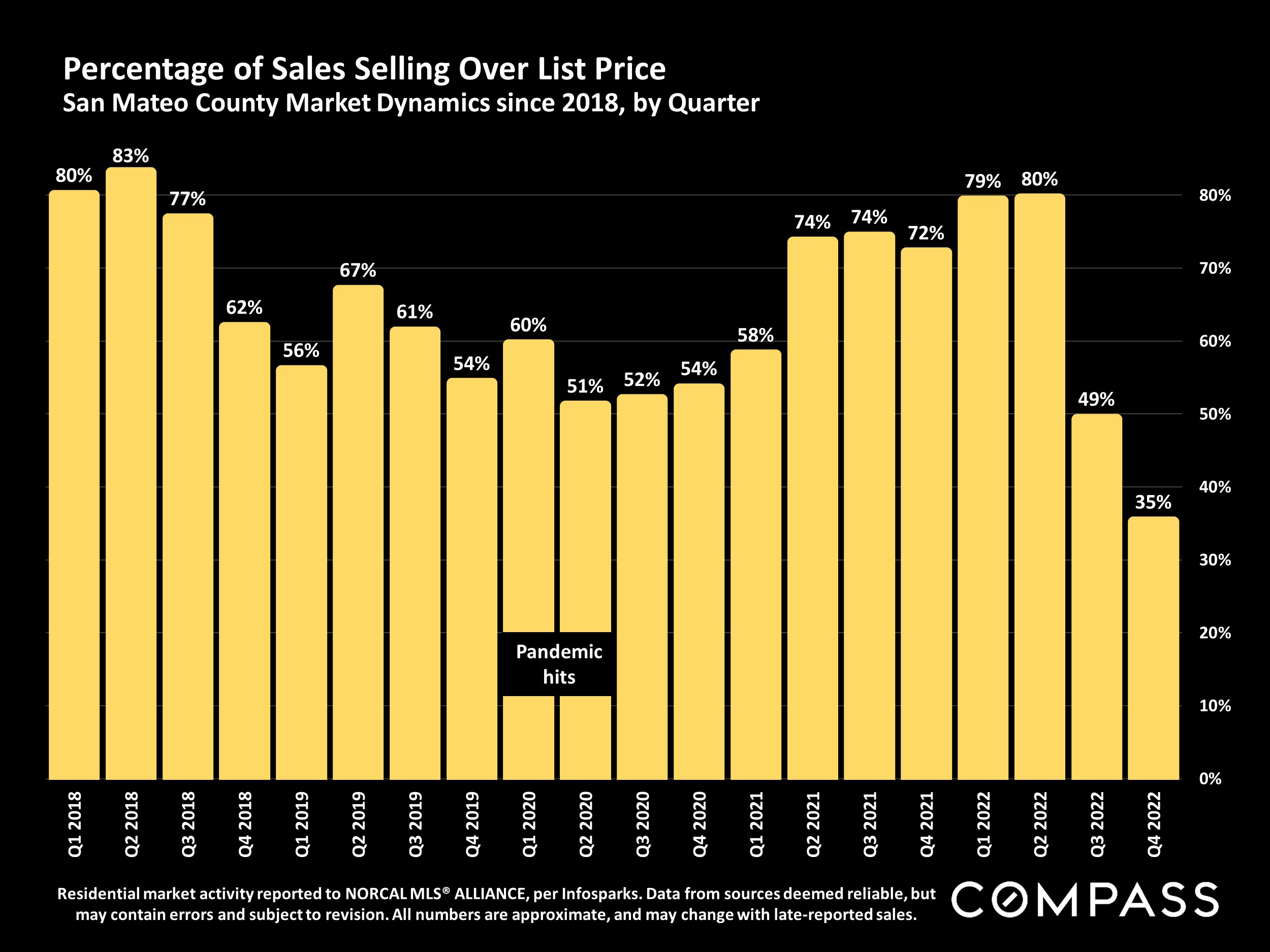

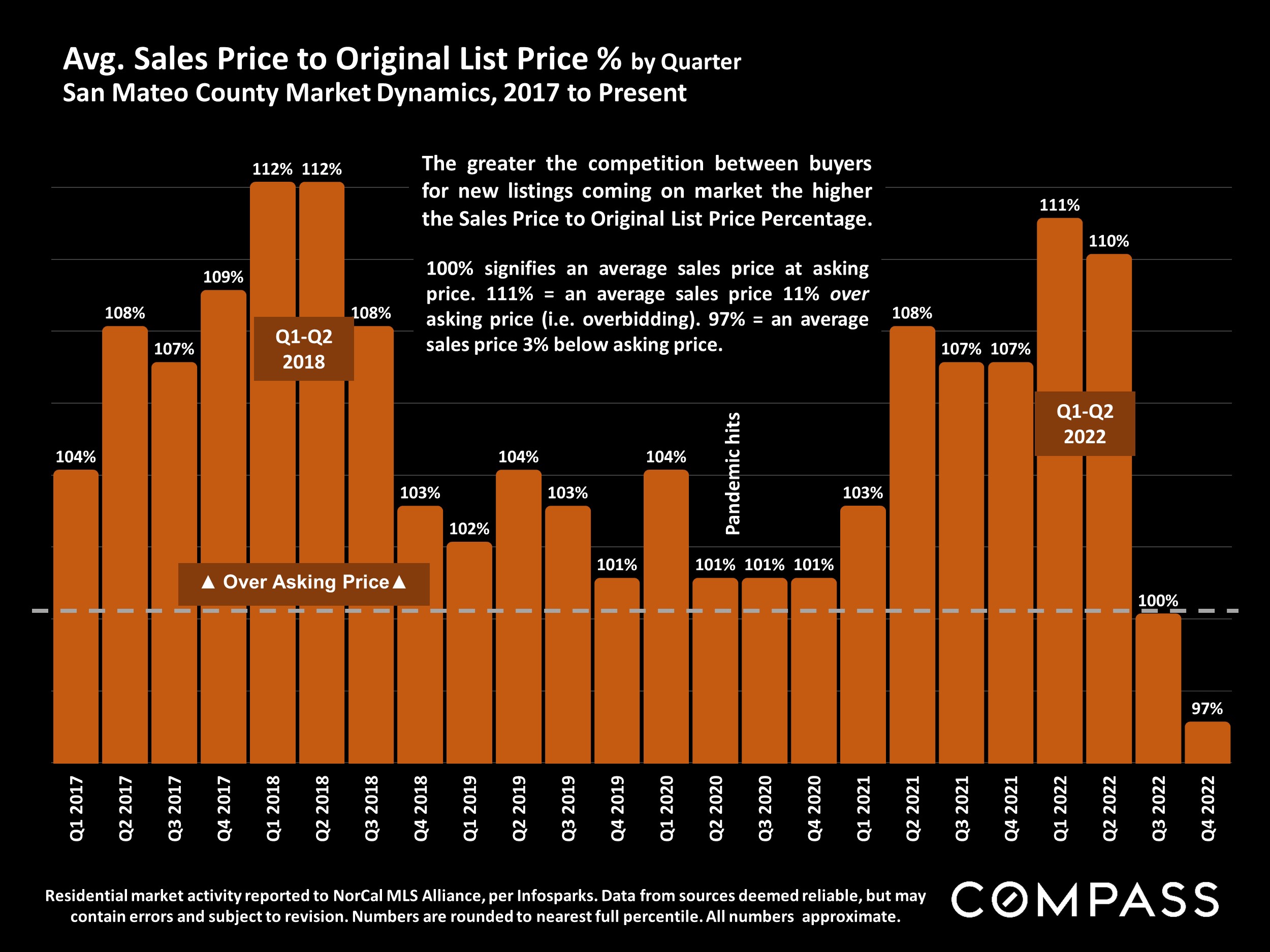

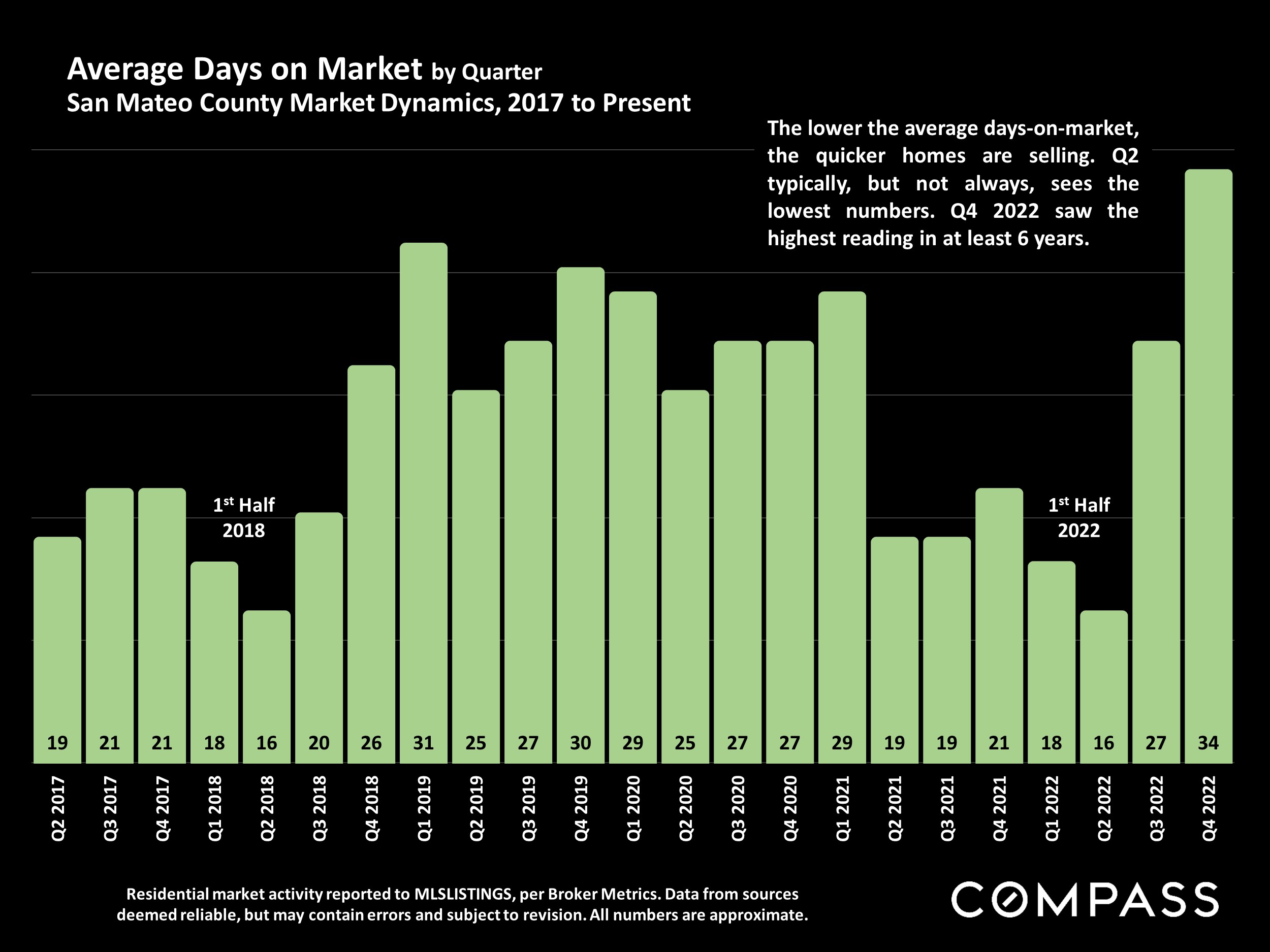

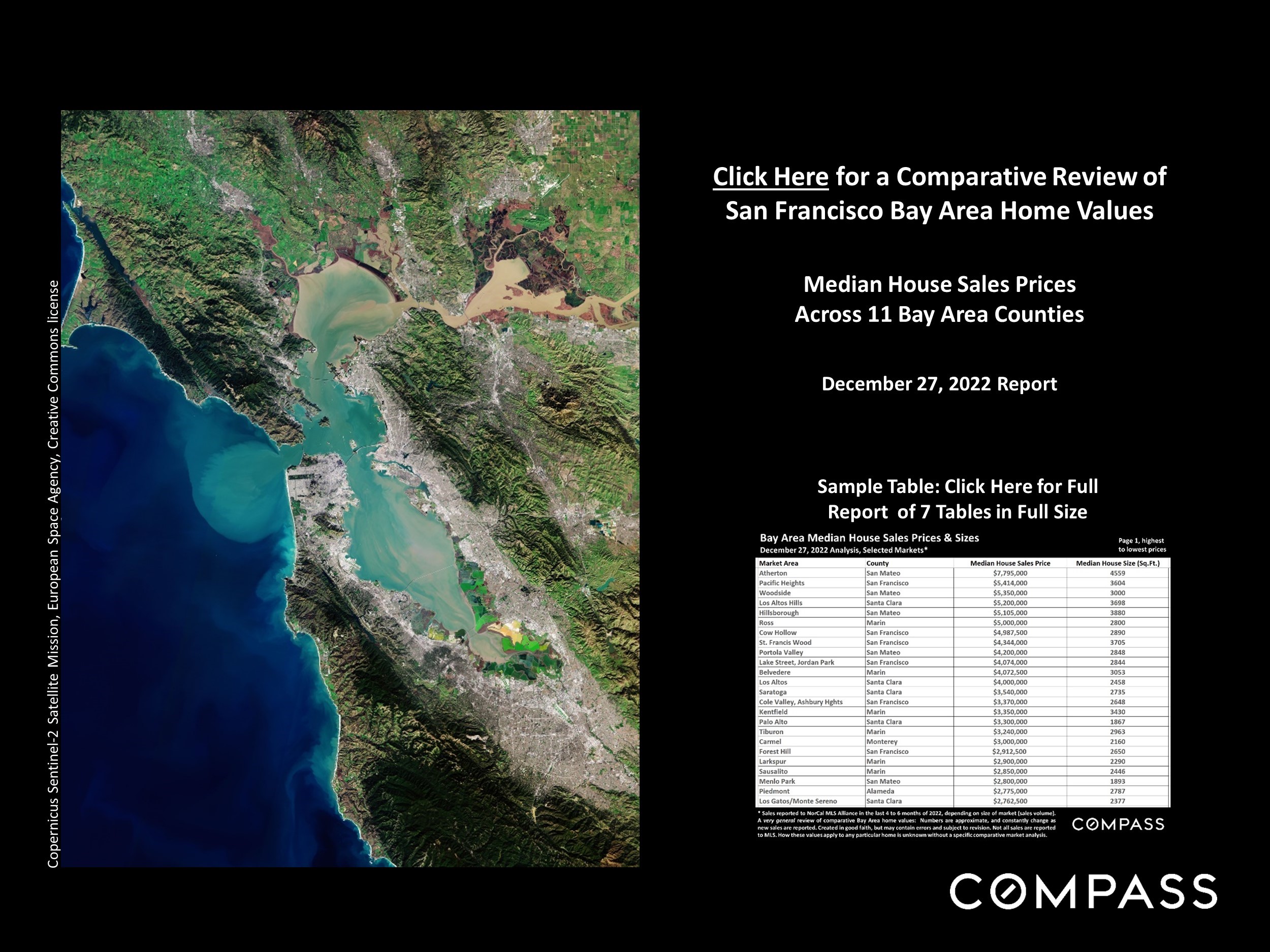

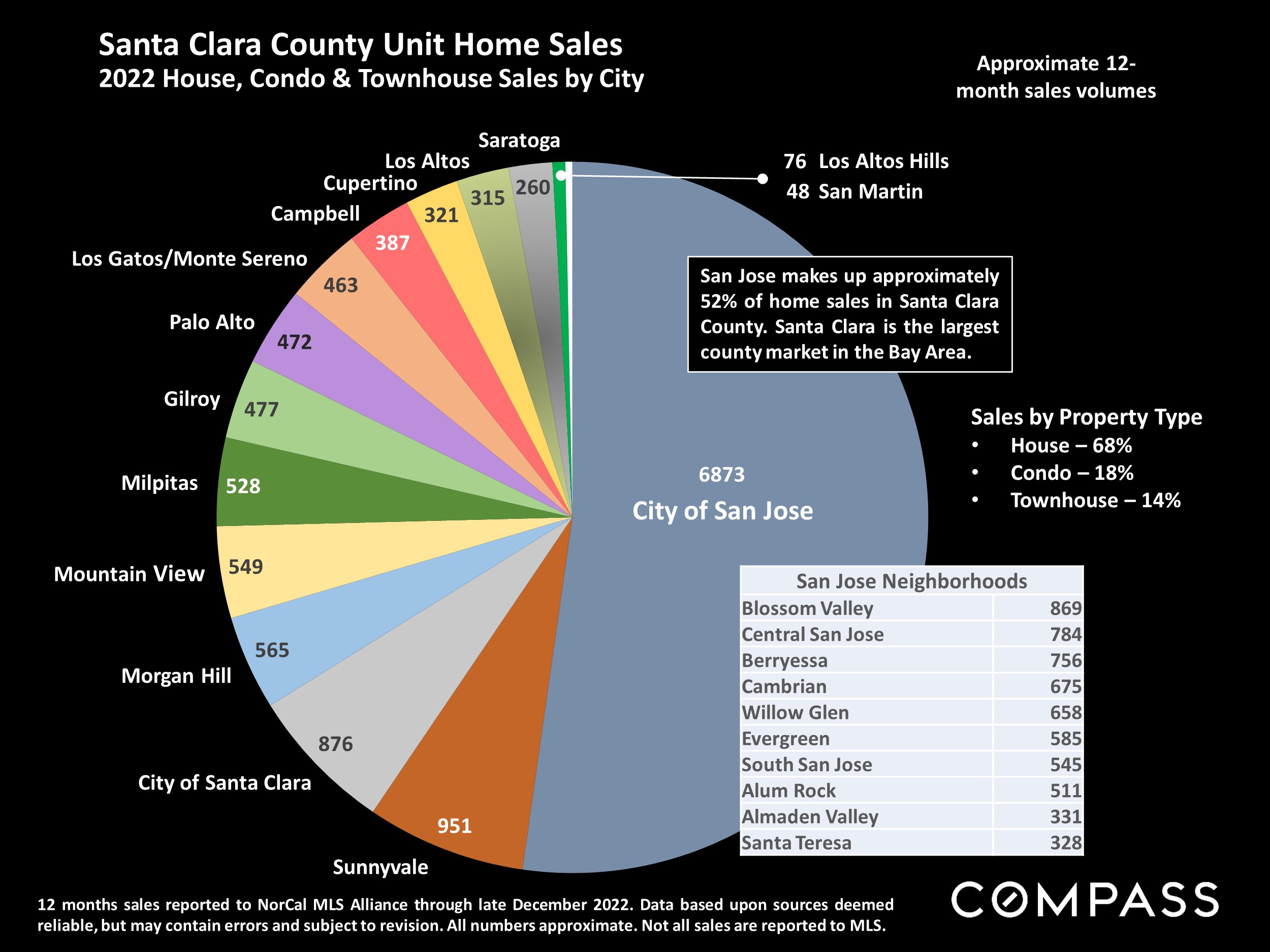

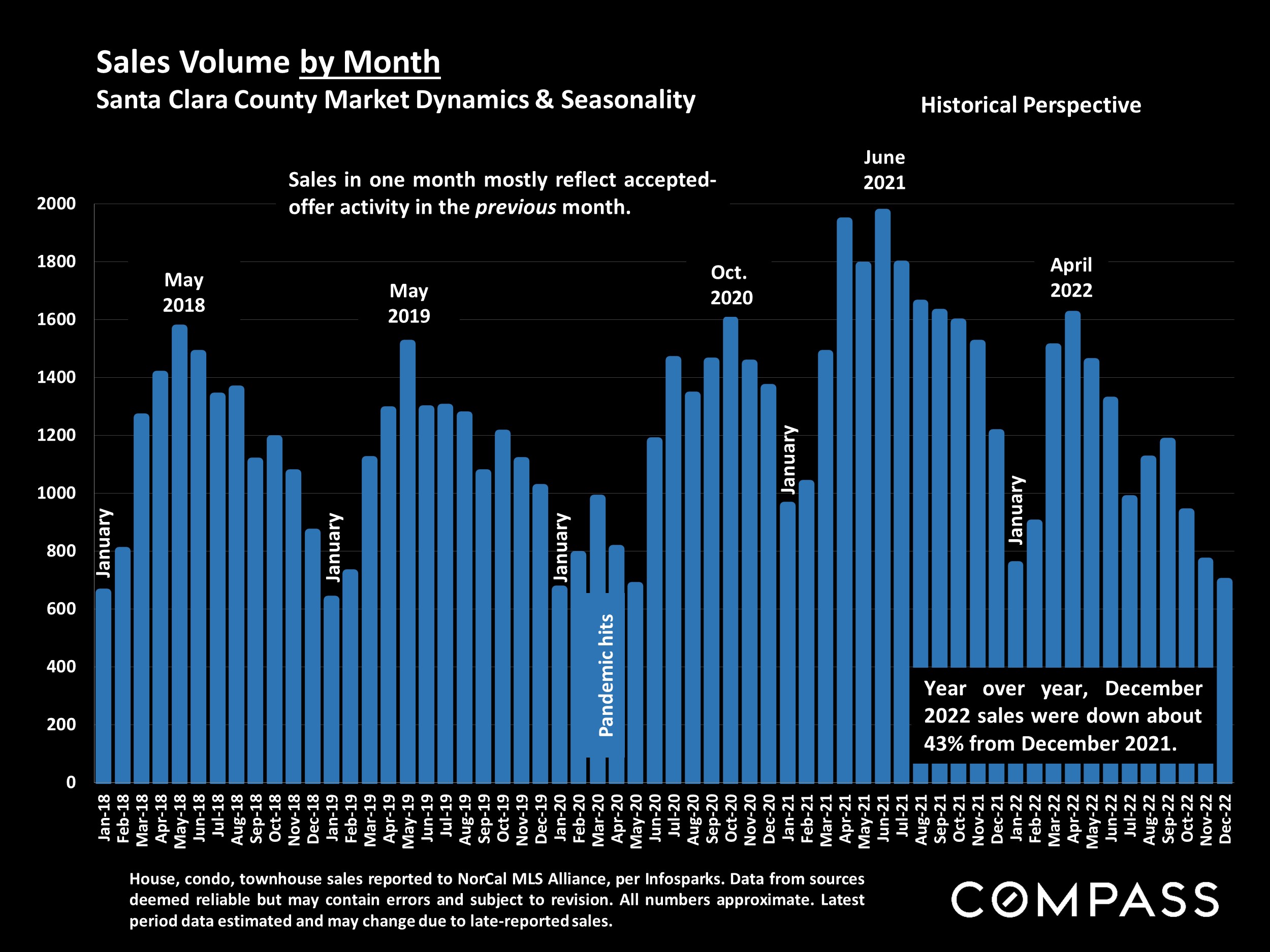

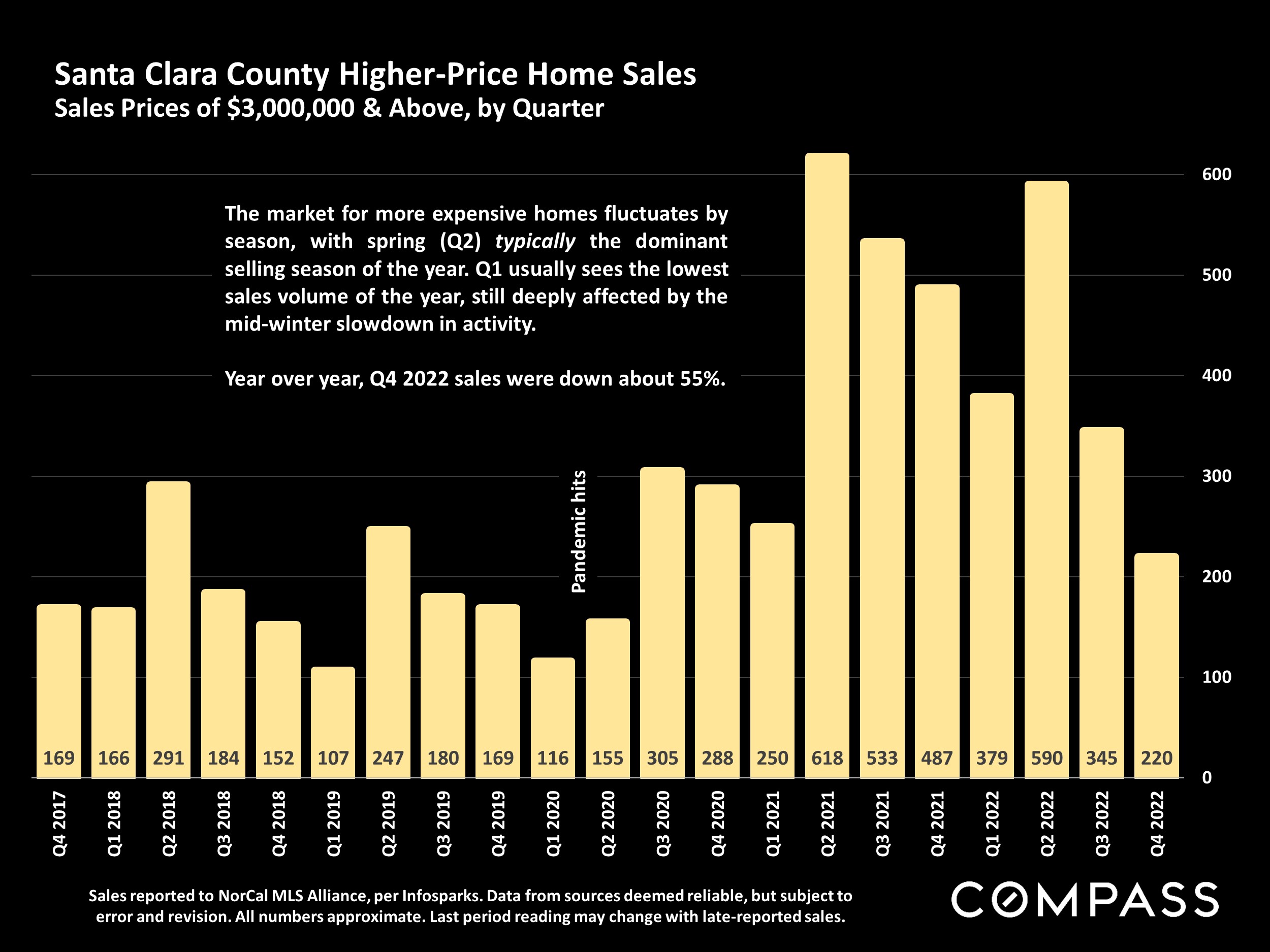

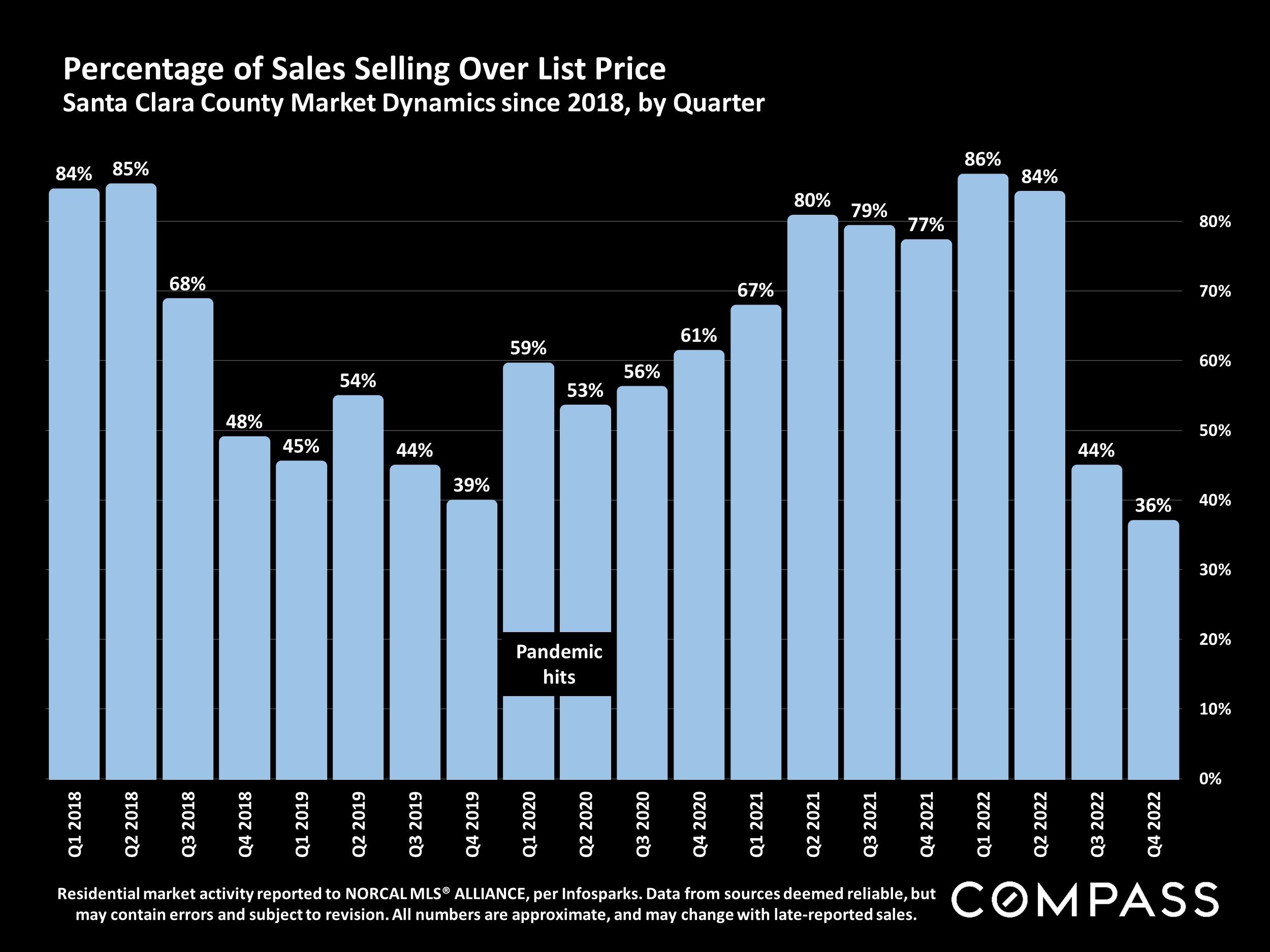

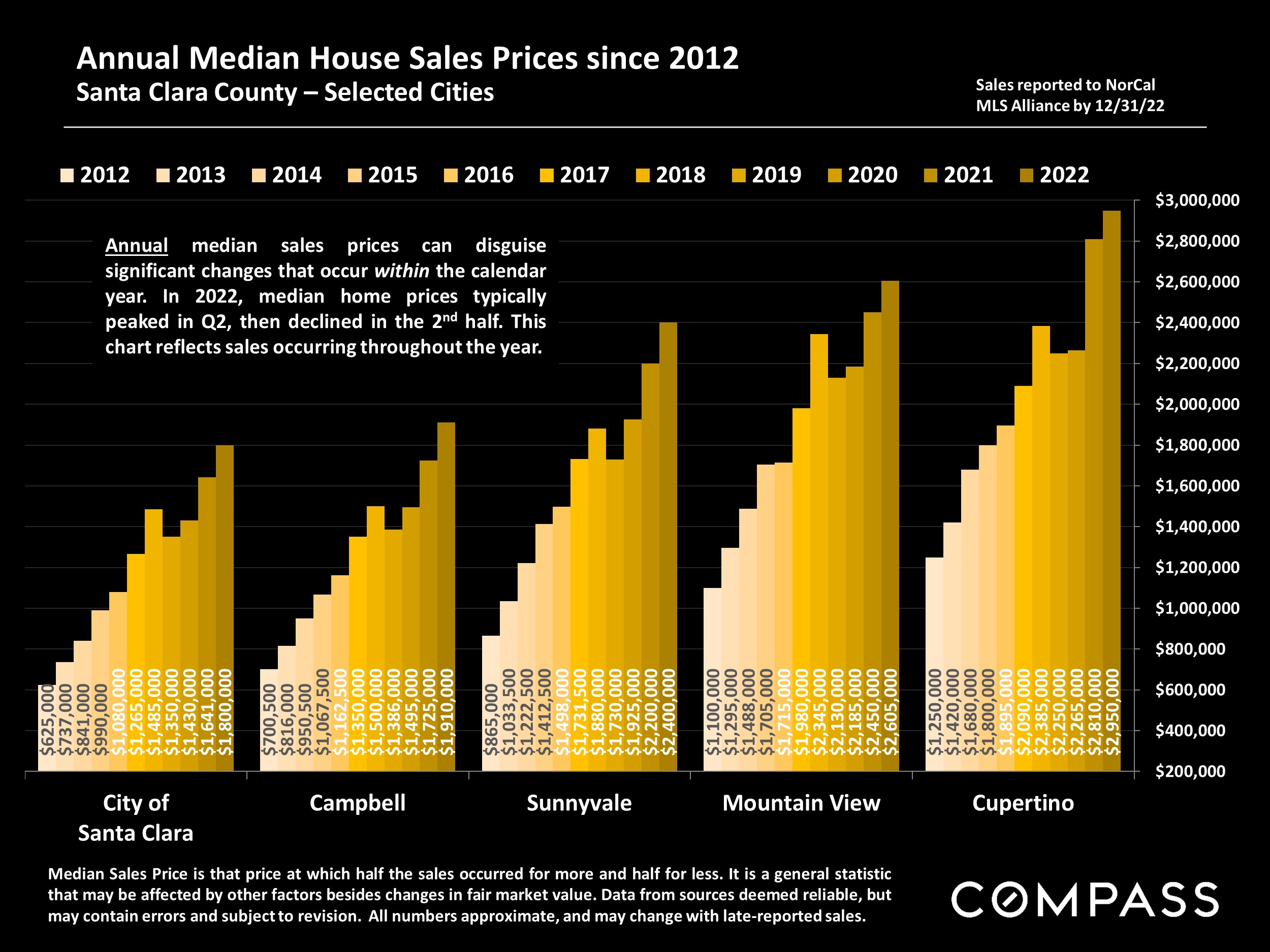

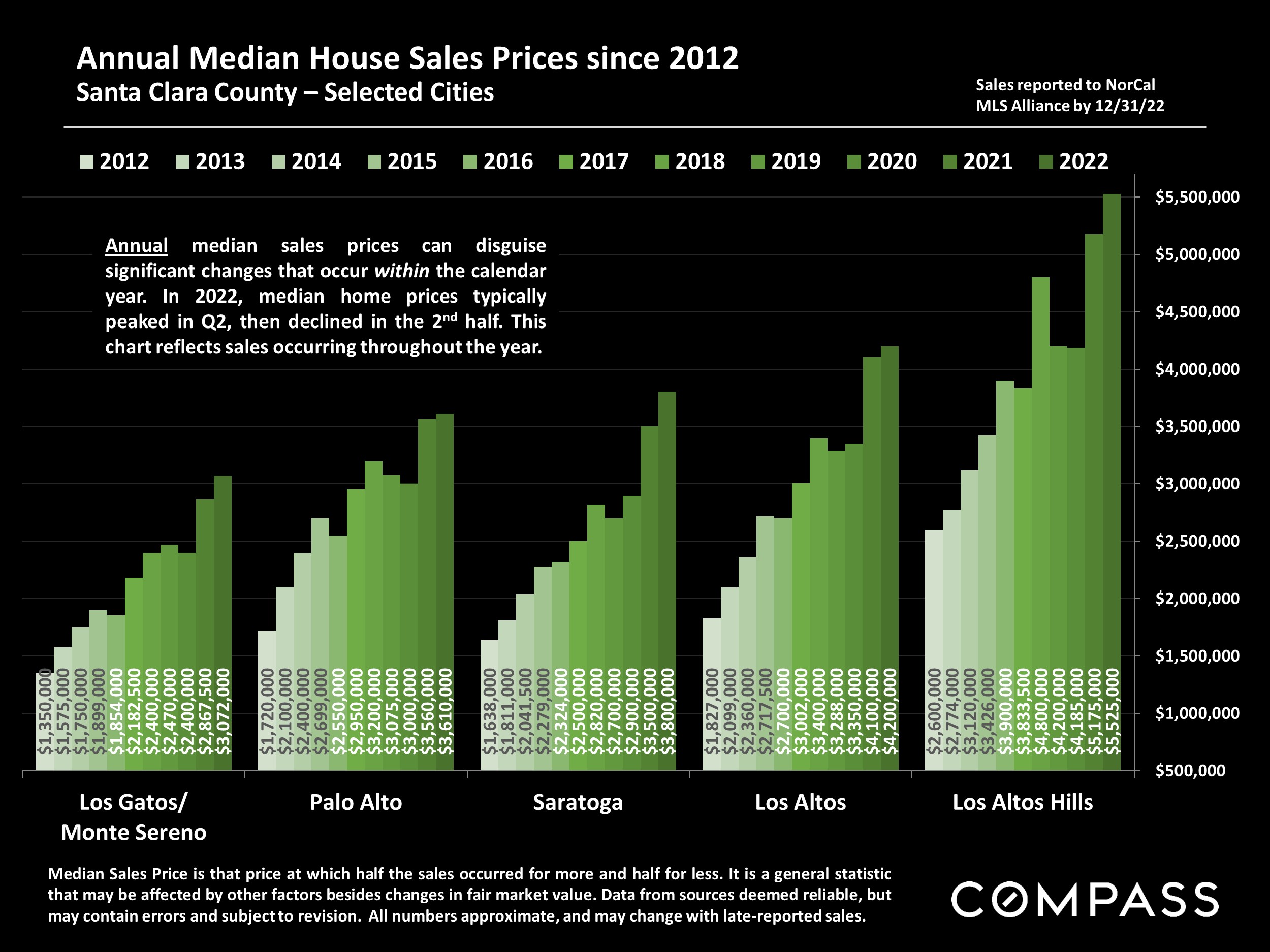

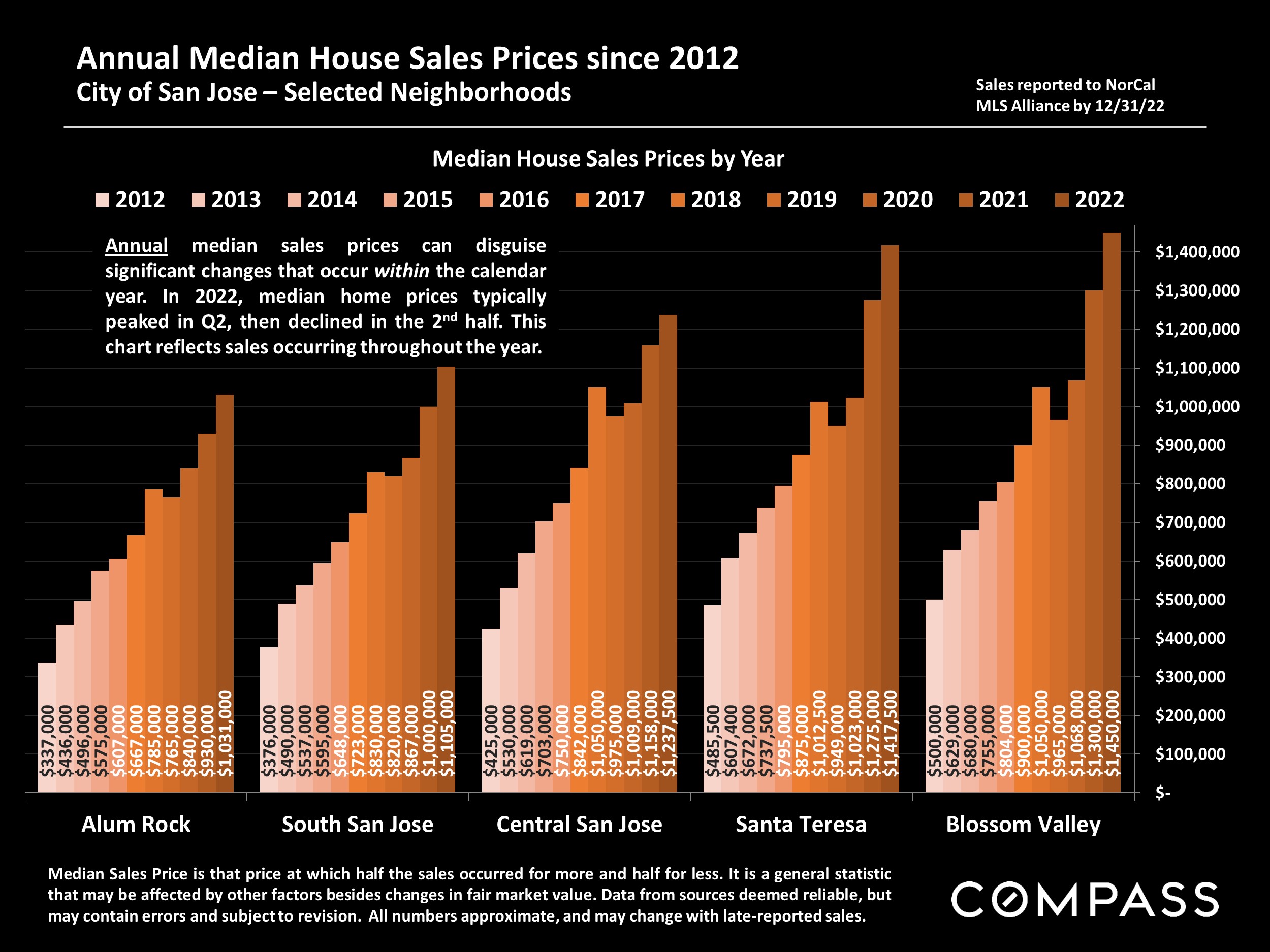

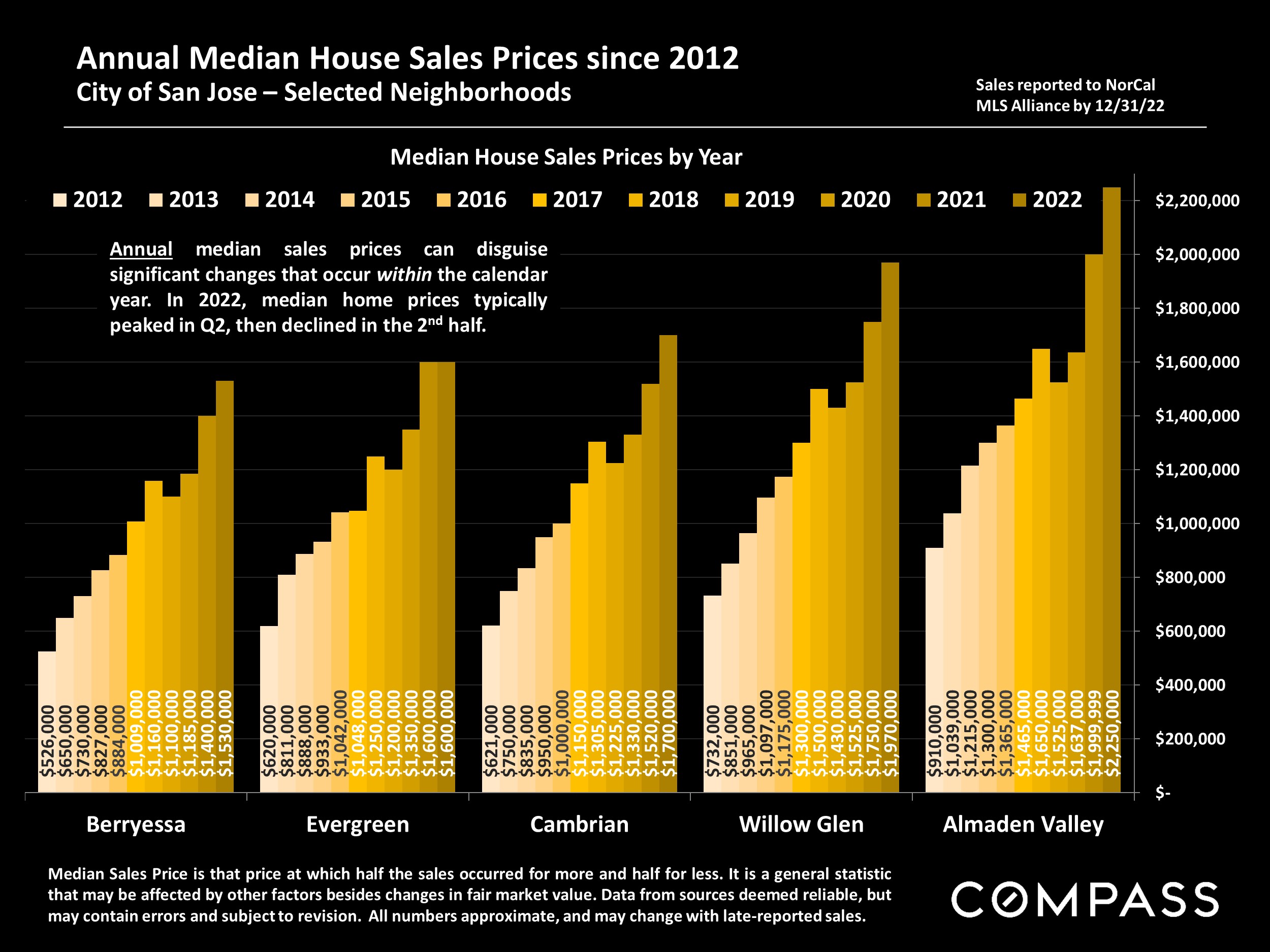

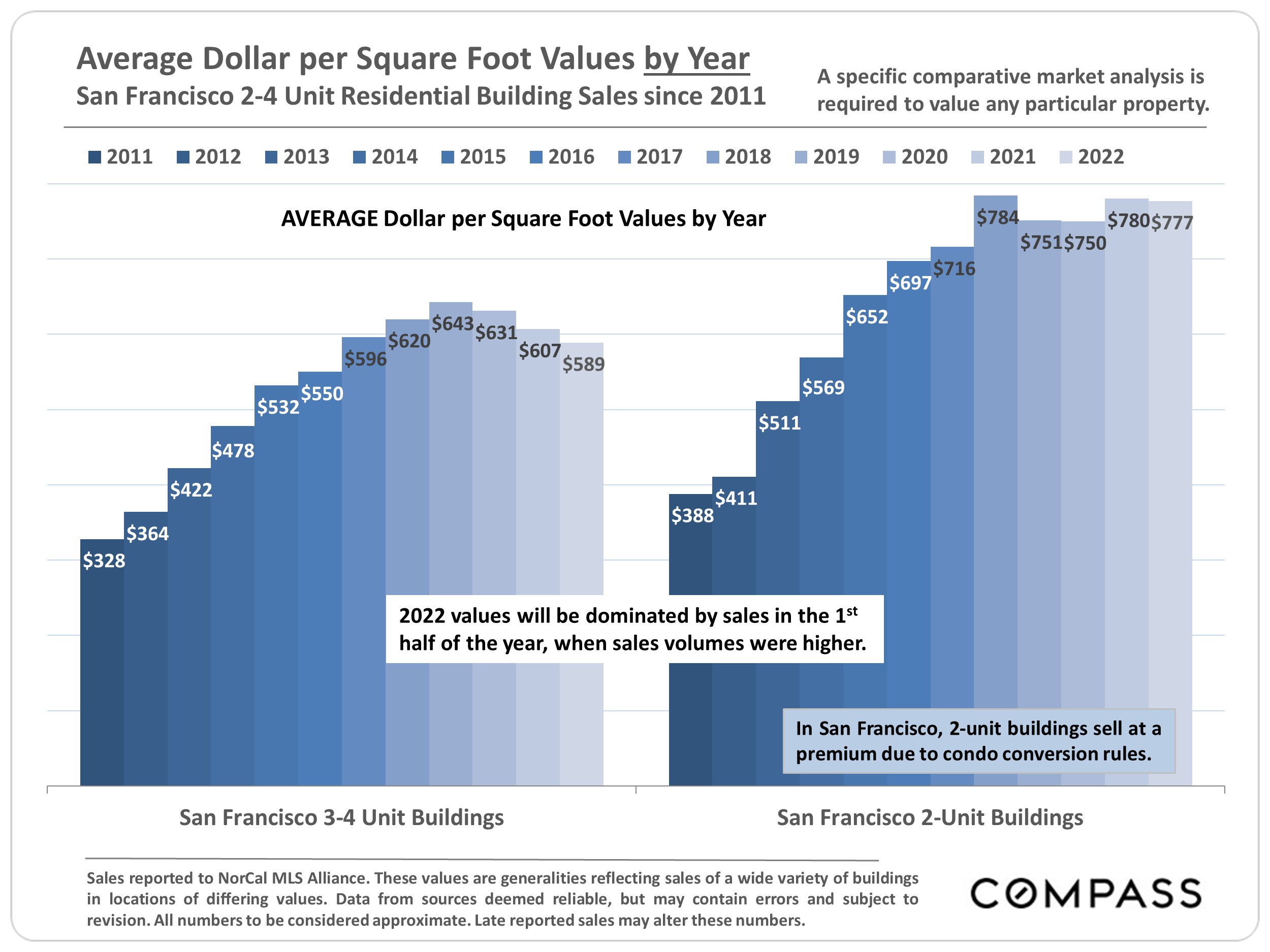

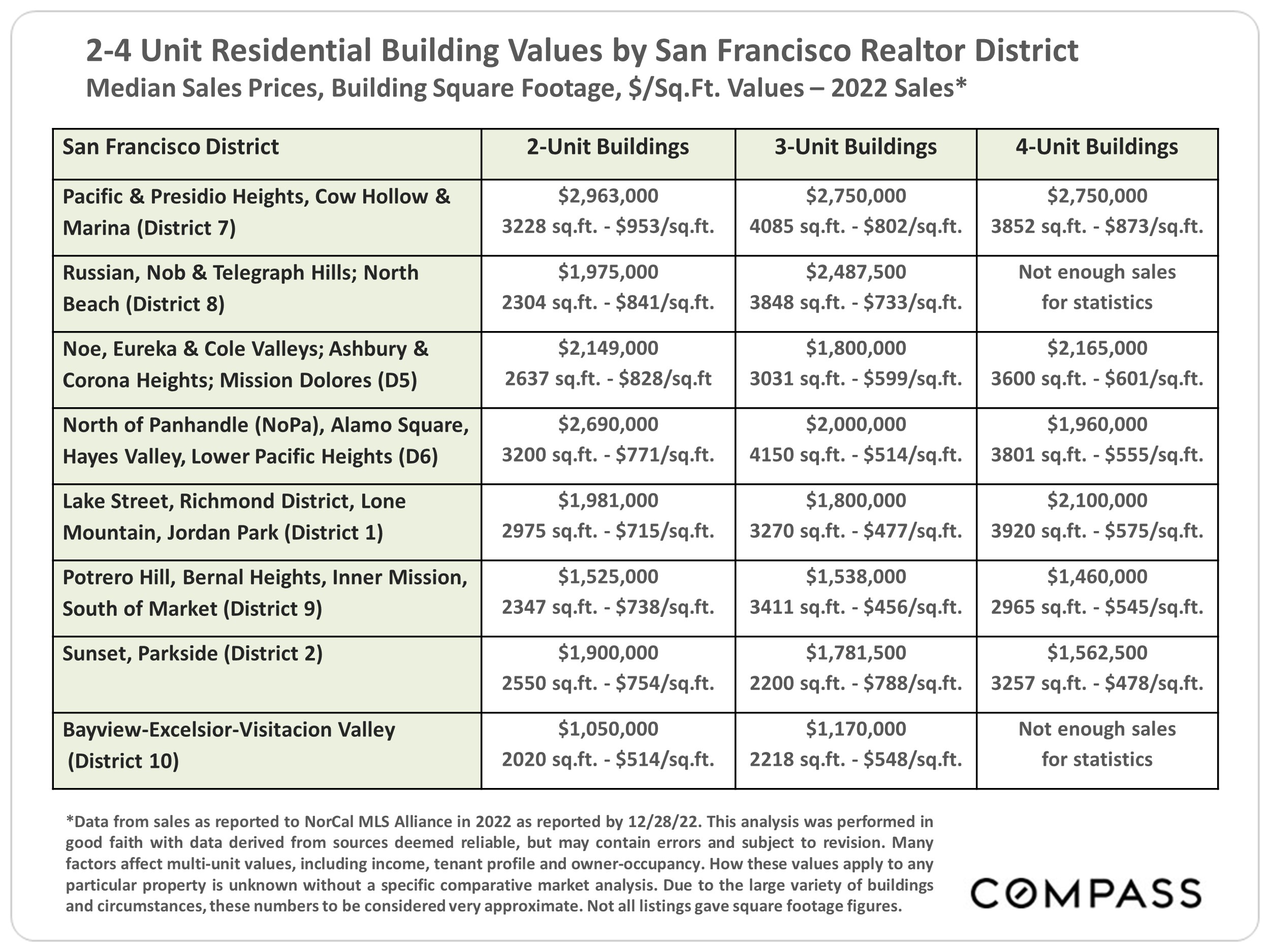

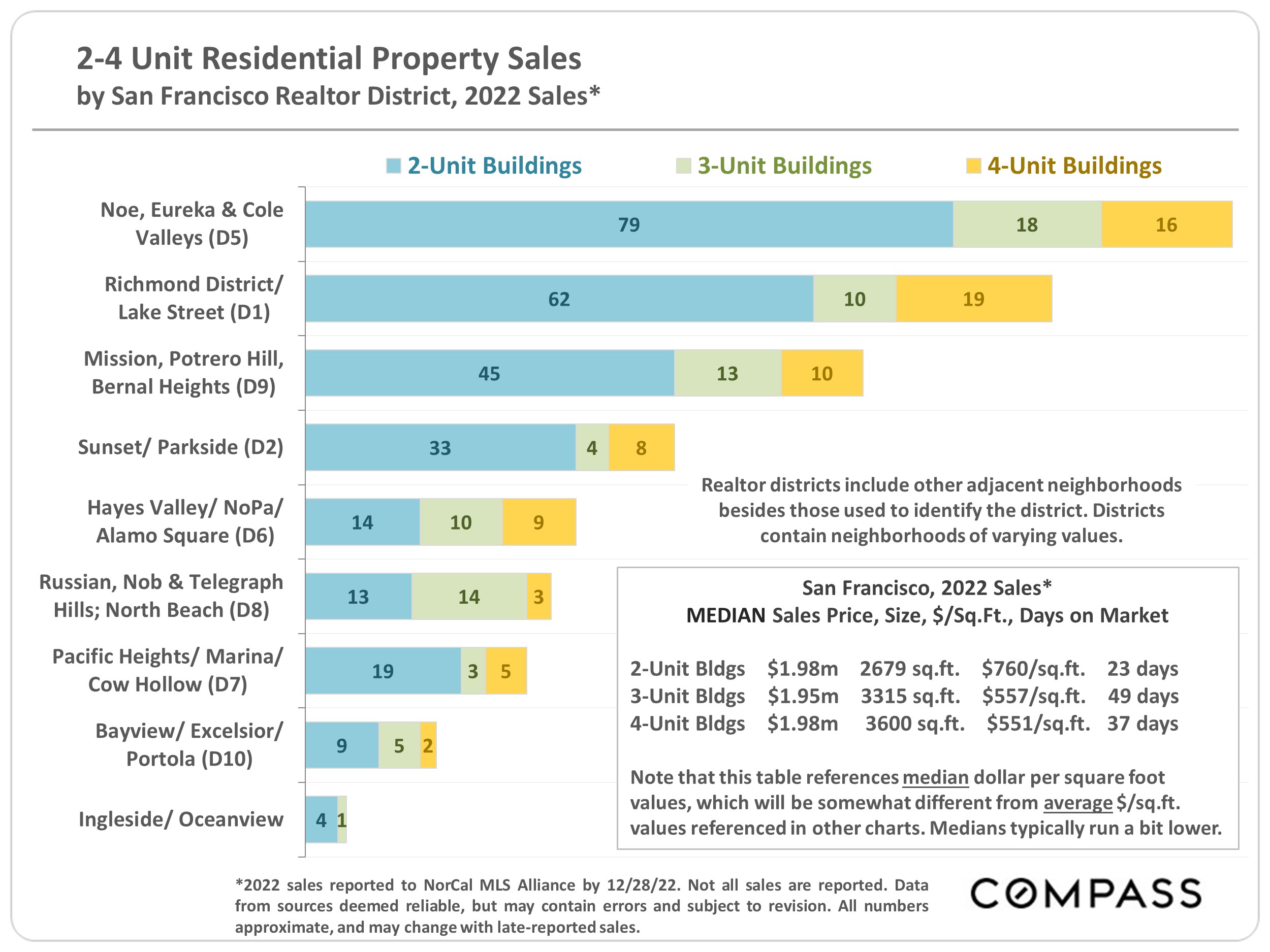

Data reported to regional MLS associations. Q4 2022 numbers are estimates using data available in early January 2023: Late reported sales may alter these numbers. Statistics are generalities, essentially summaries of disparate data generated by dozens, hundreds or thousands of unique, individual sales. They are best seen not as precise measurements, but as broad, comparative indicators. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers approximate. How these figures apply to any particular property is unknown without a specific comparative market analysis.

Note that the quantity of sales in any given local submarket is usually relatively small and/or the number of sales that report the necessary financial information can be limited. Buildings of different ages, qualities and sizes selling in different periods can cause these average and median figures to fluctuate significantly. Furthermore, the reliability of some of these calculations depends upon the quality of the income and expense figures provided by the listing agents, and sometimes instead of actual numbers, much less meaningful projected or scheduled figures are used. Therefore, the above statistics should be considered very general indicators, and how they apply to any particular property without a specific comparative market analysis is unknown.

These analyses were made in good faith with data from sources deemed reliable, but they may contain errors and are subject to revision. Statistics are generalities and all numbers should be considered approximate.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.