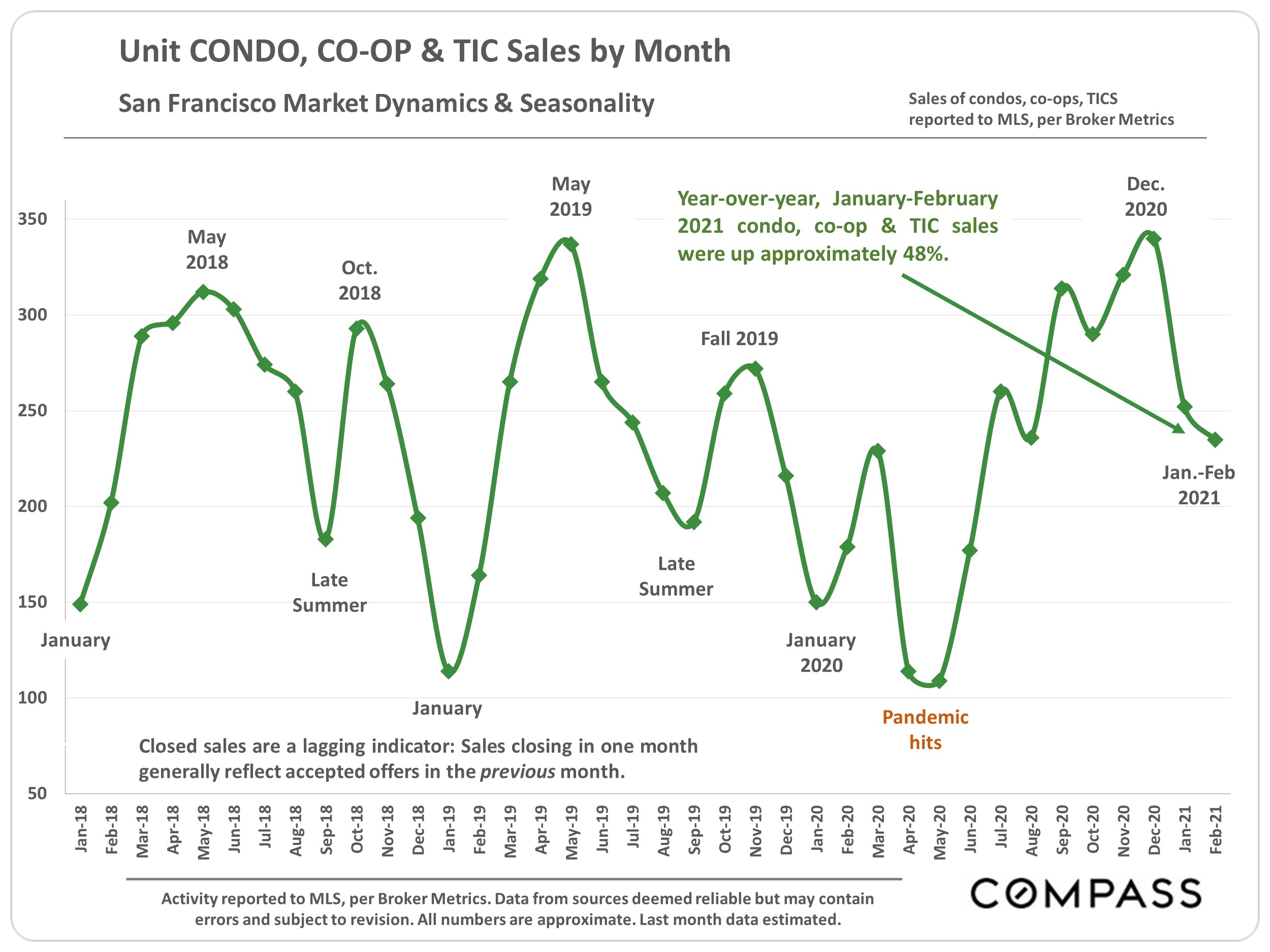

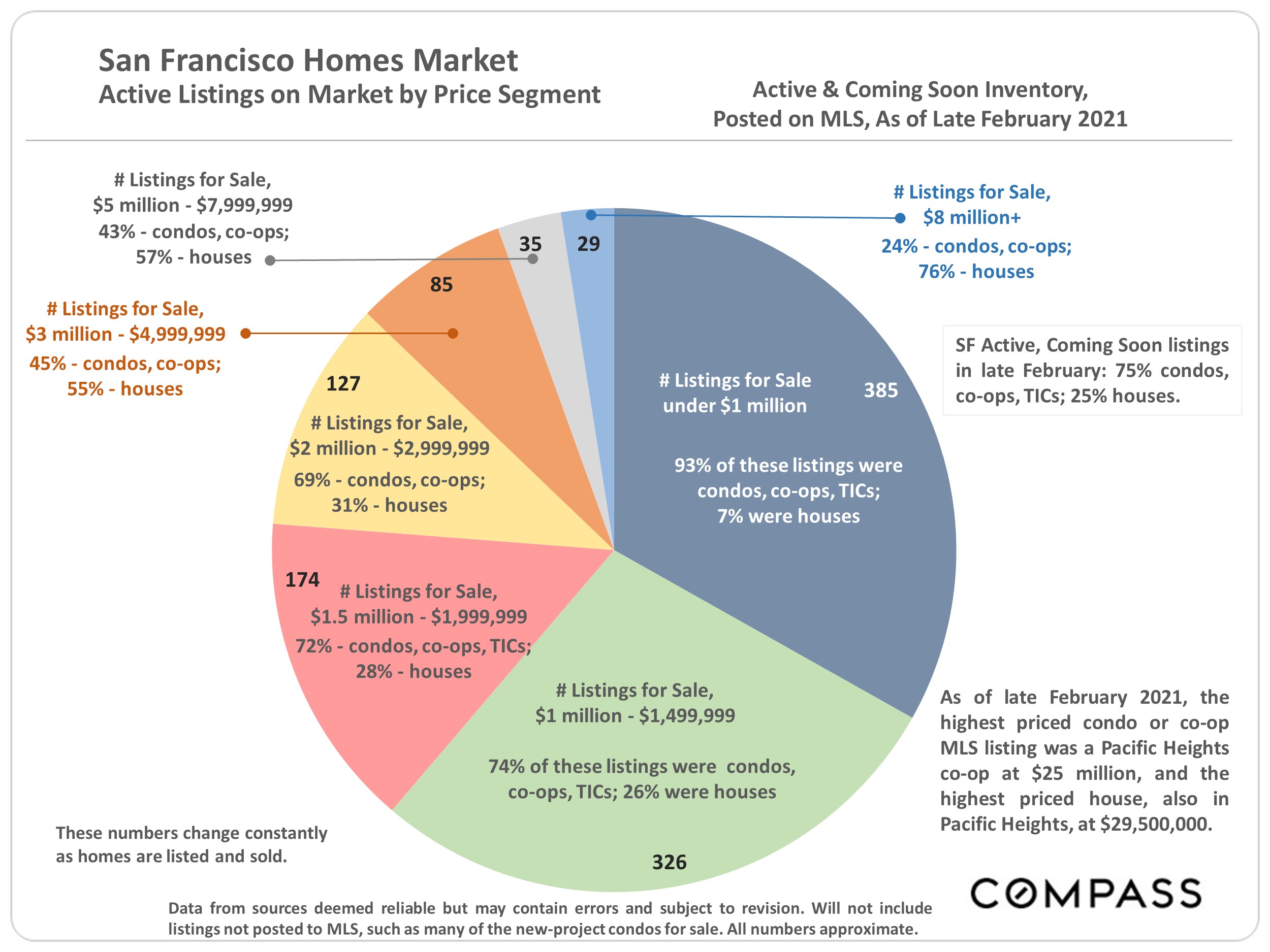

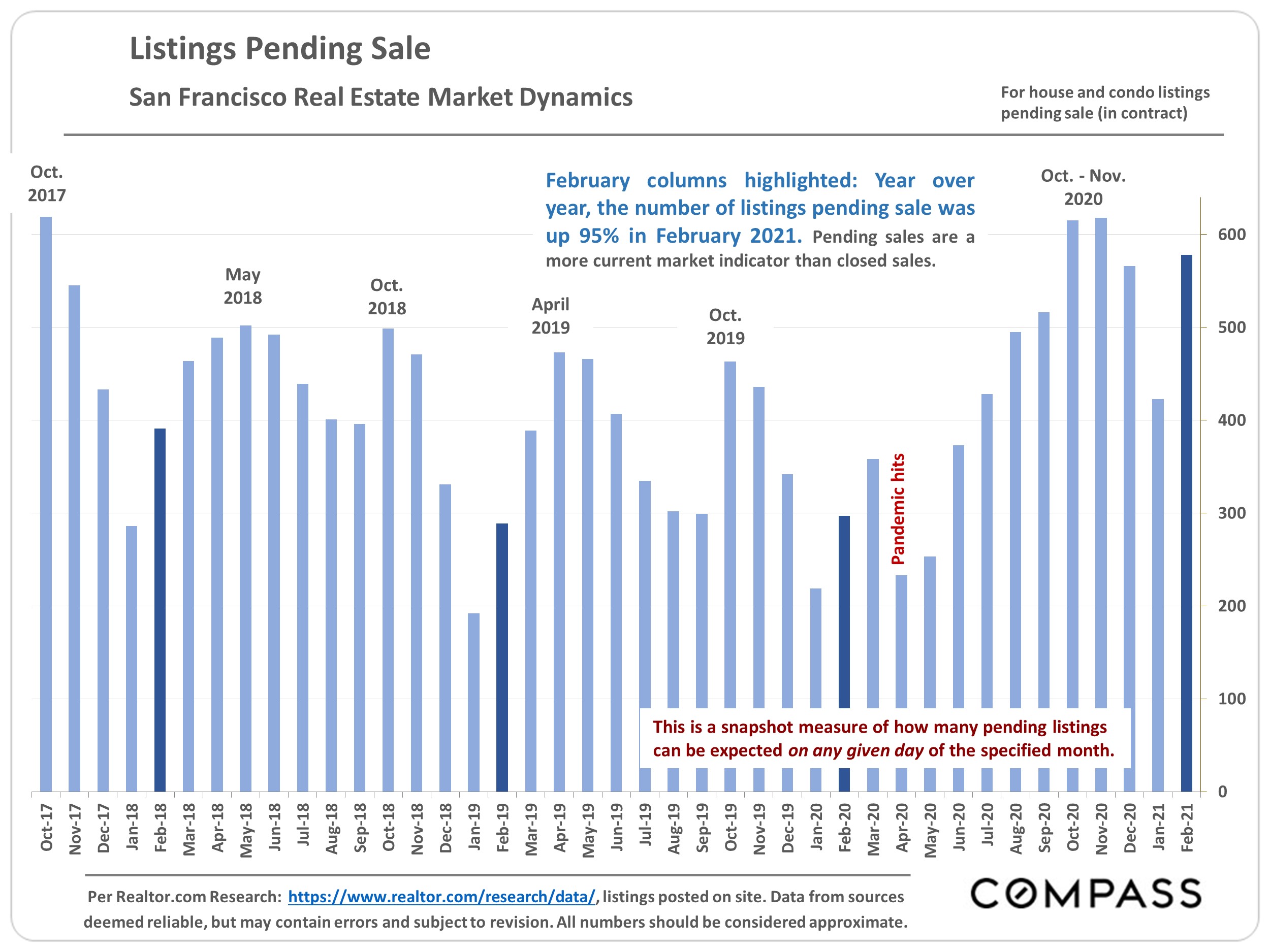

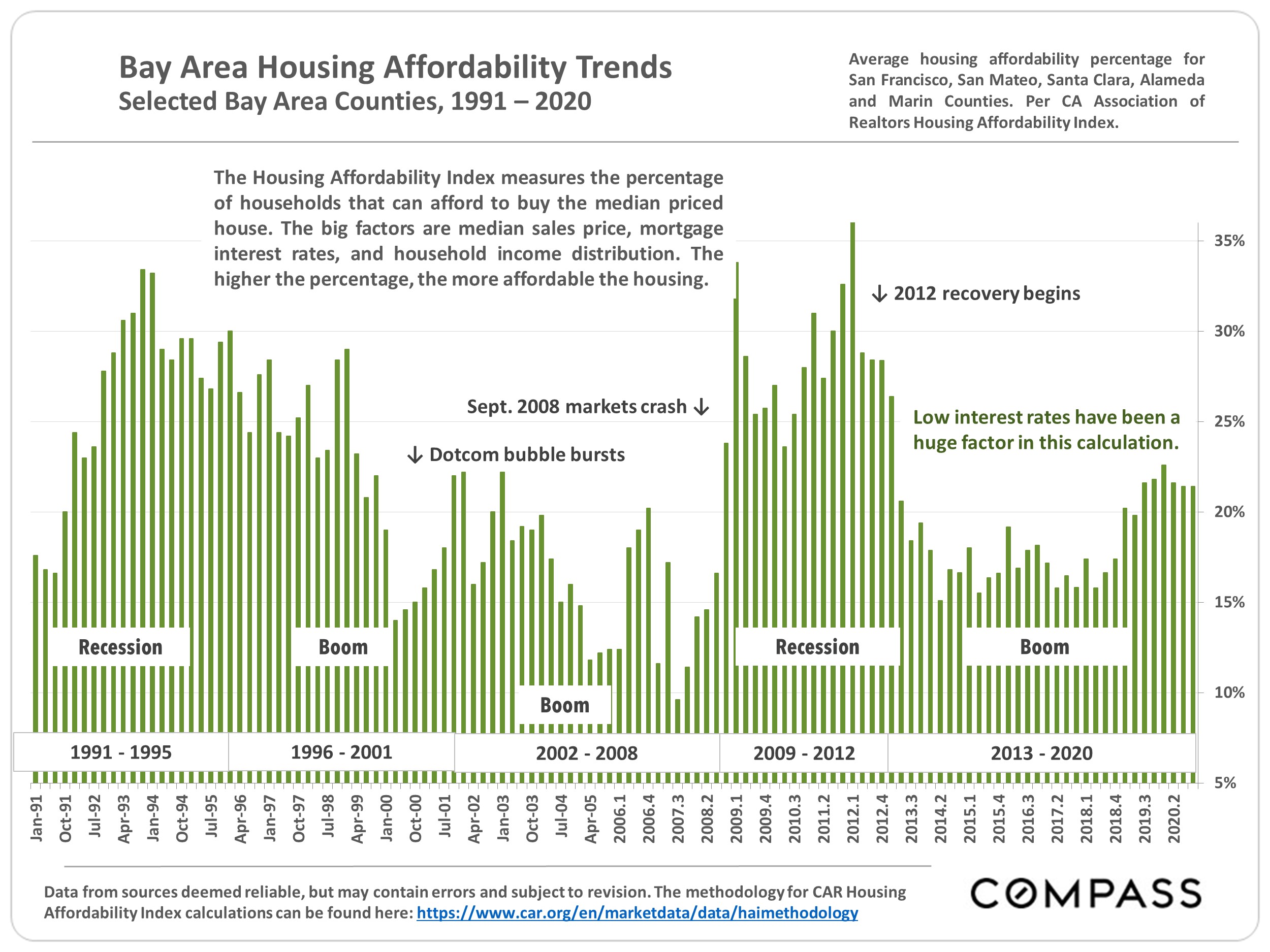

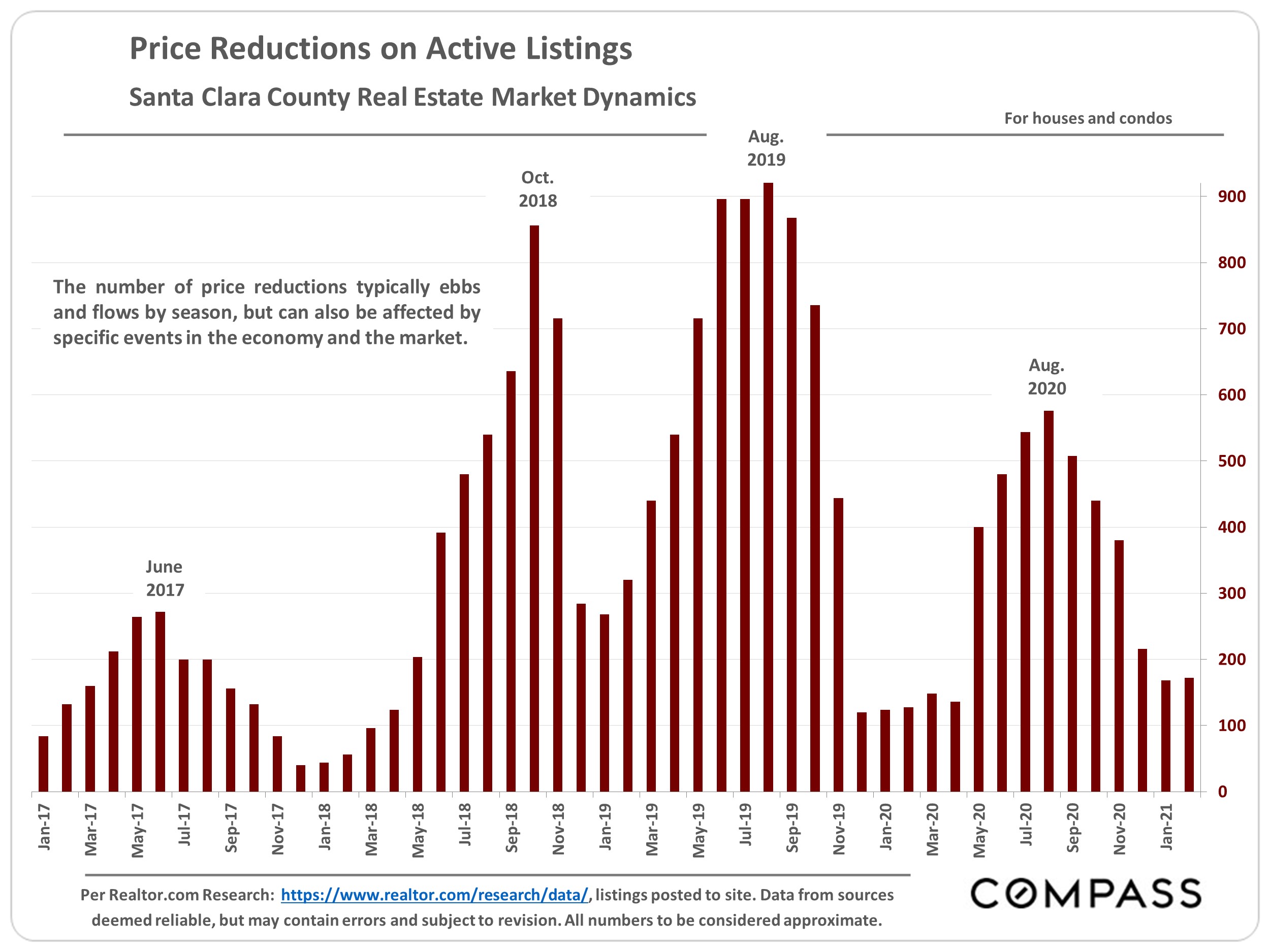

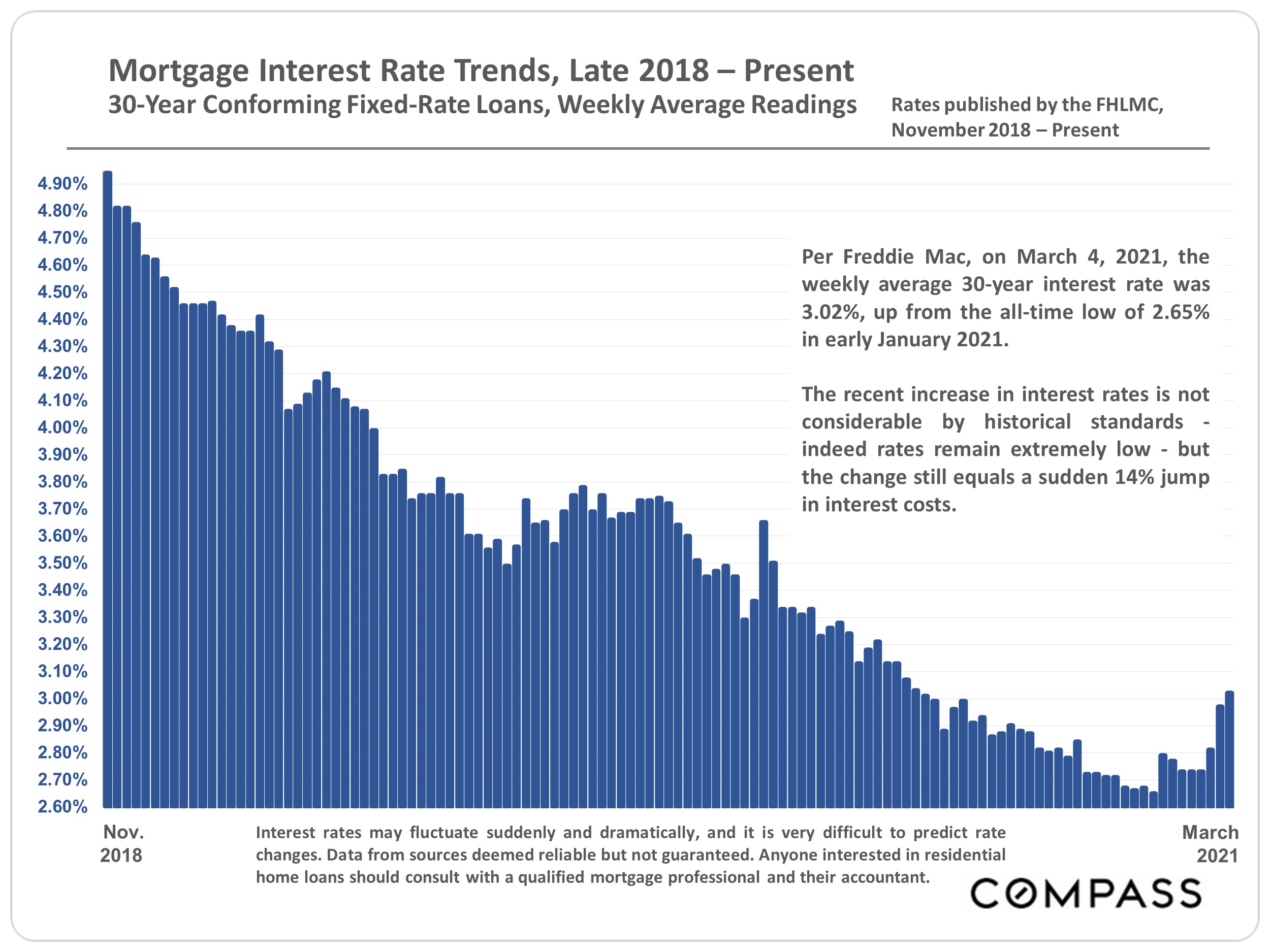

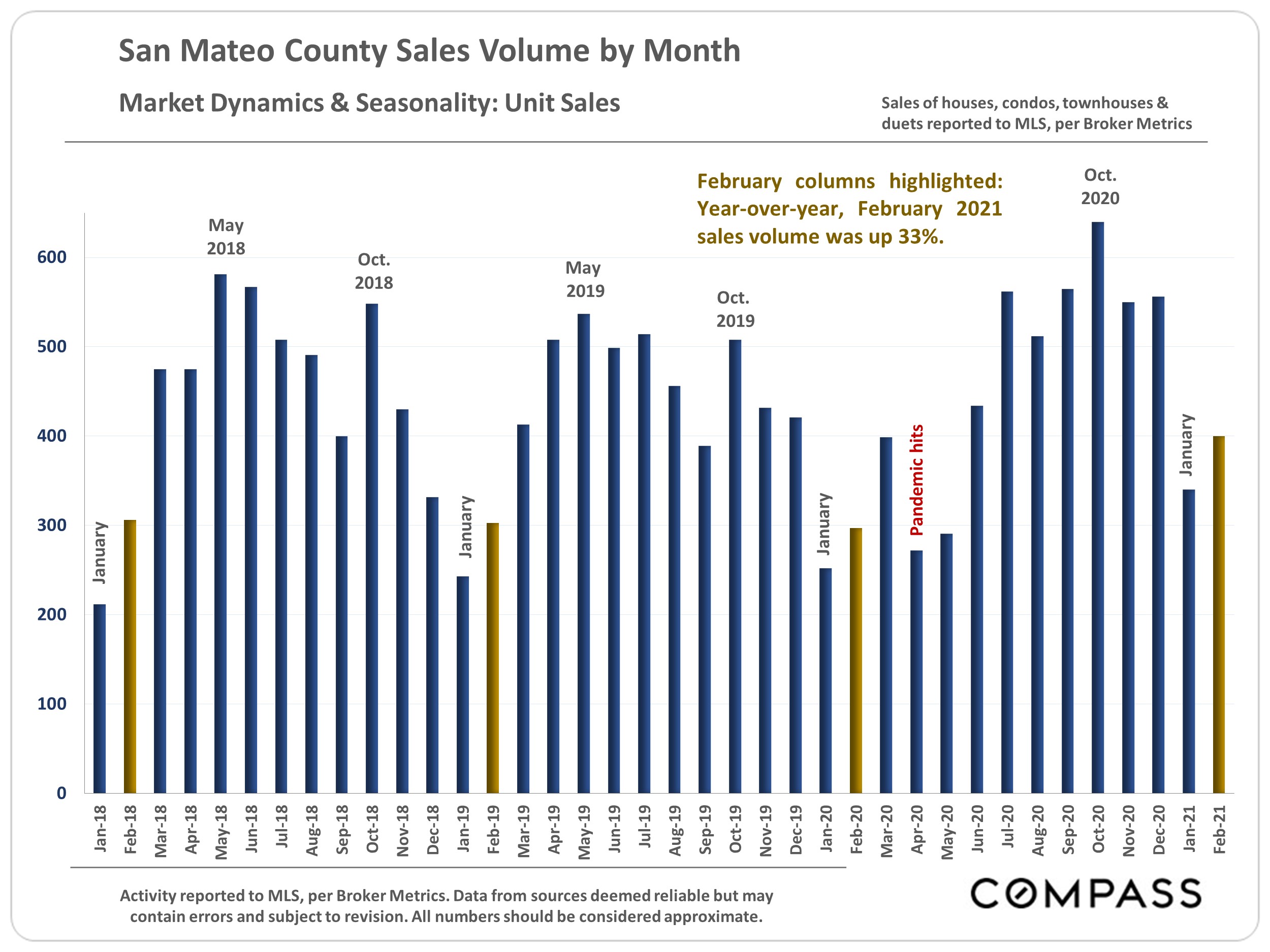

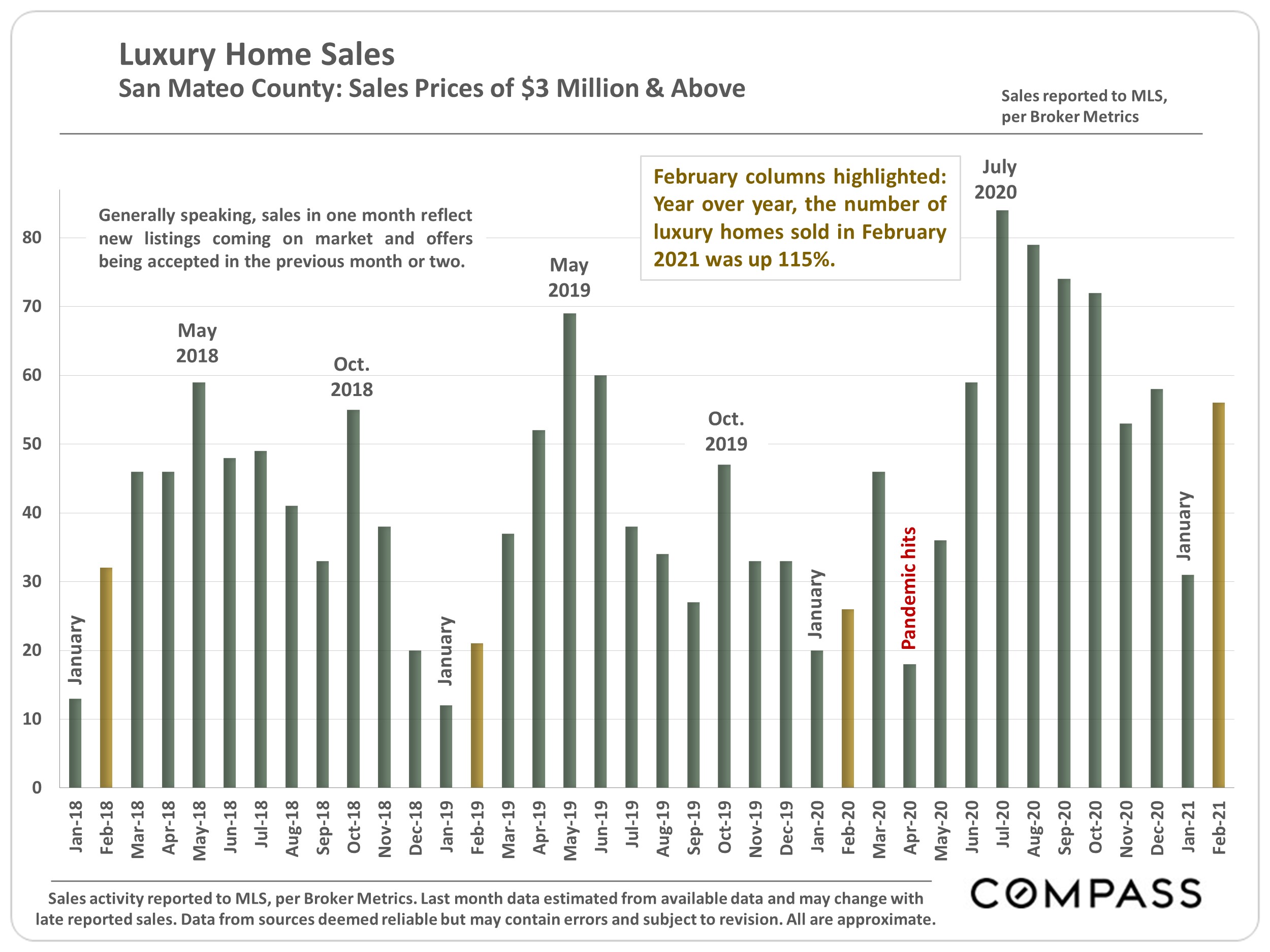

The Spring Market Began in January & Continues to Accelerate

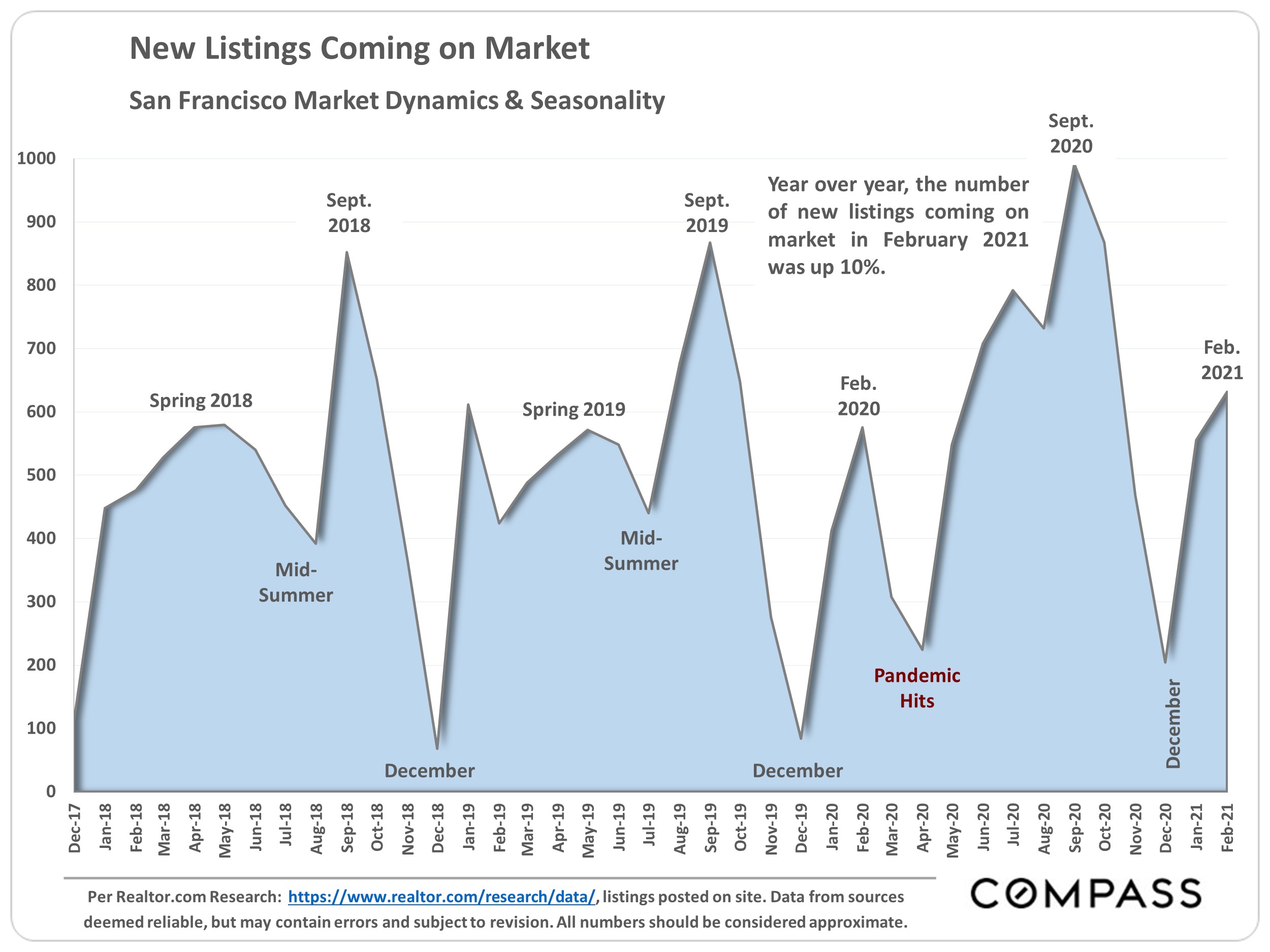

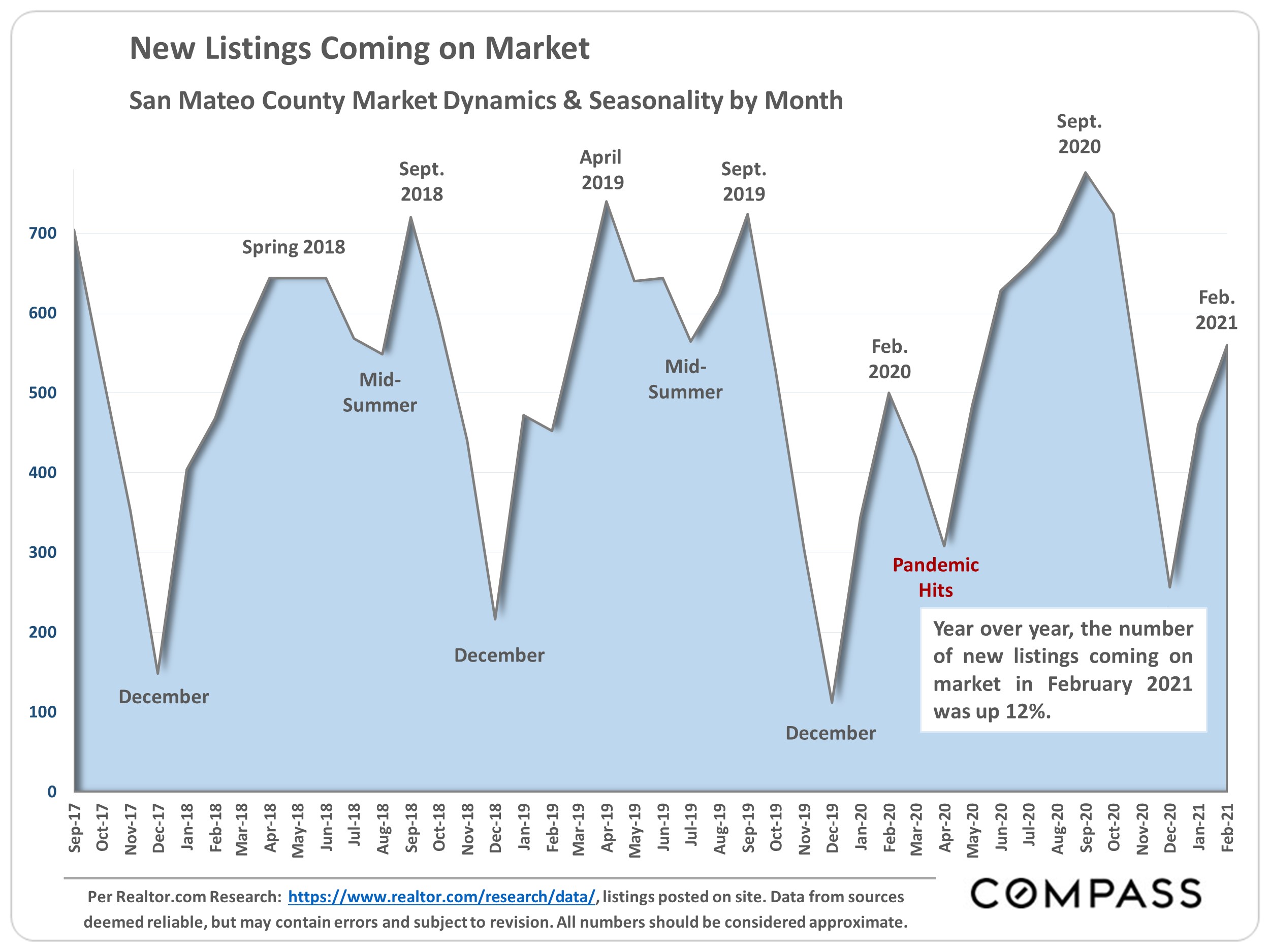

New Listings up 10%

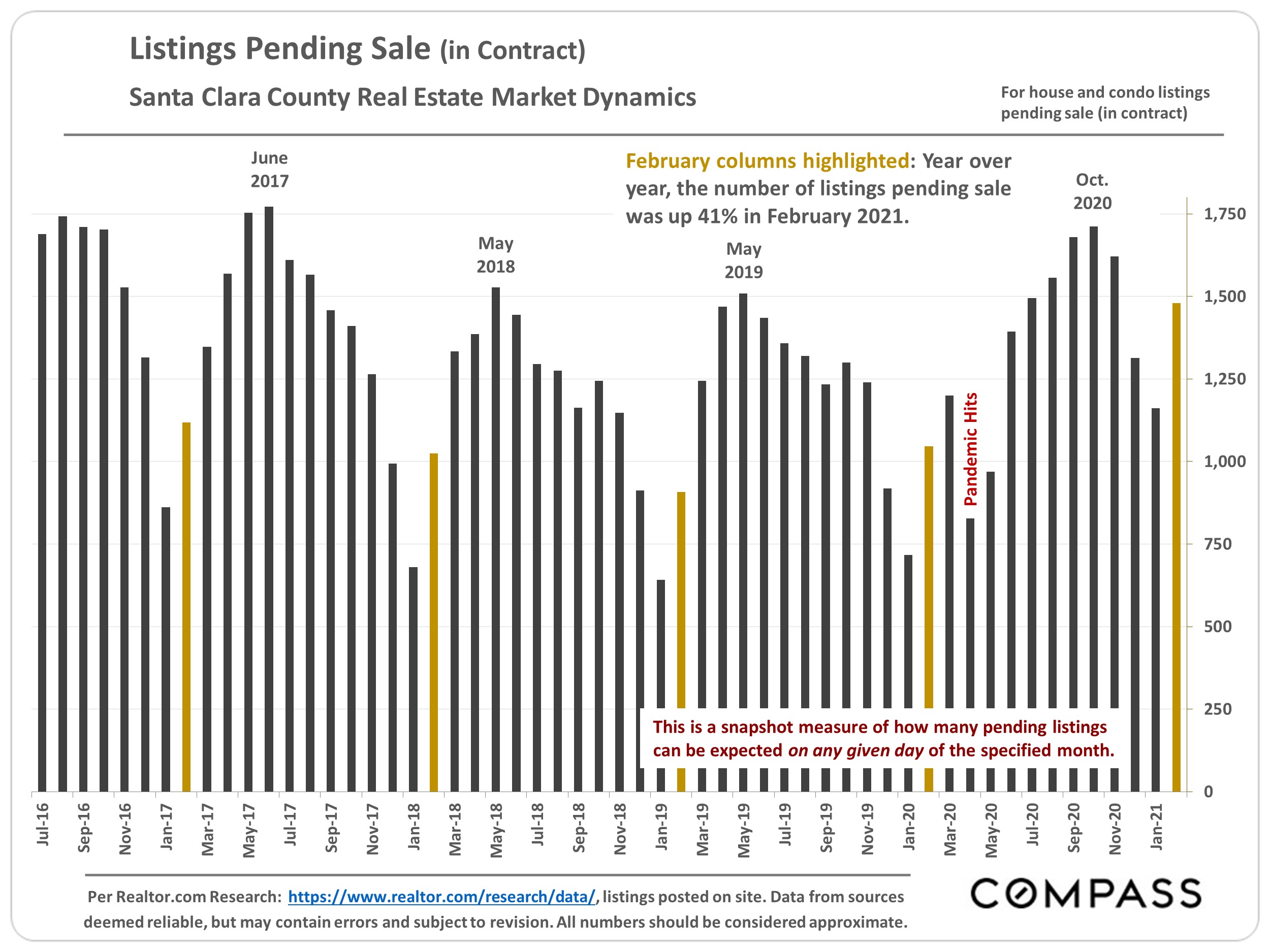

Listings Pending Sale up 95%

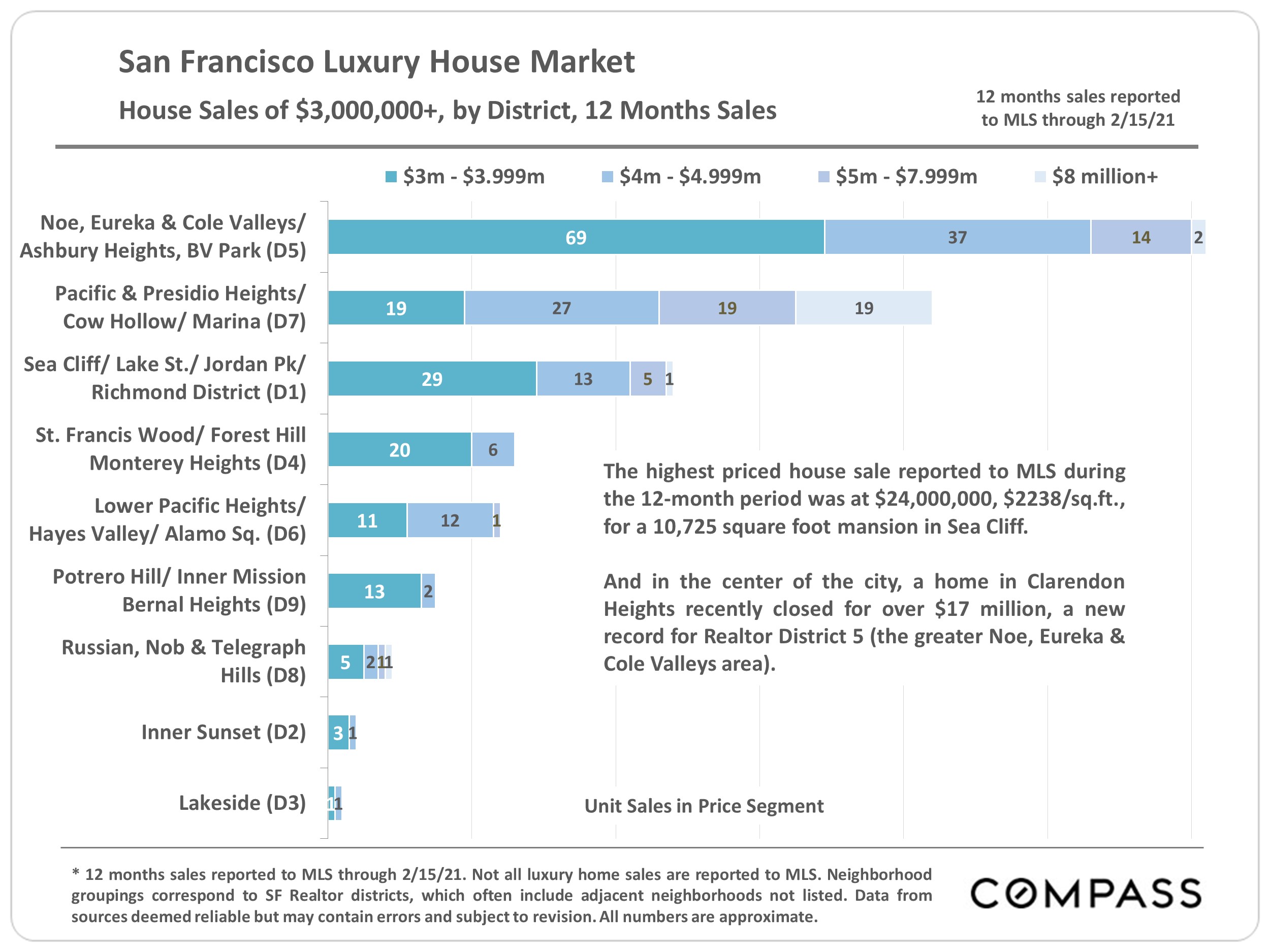

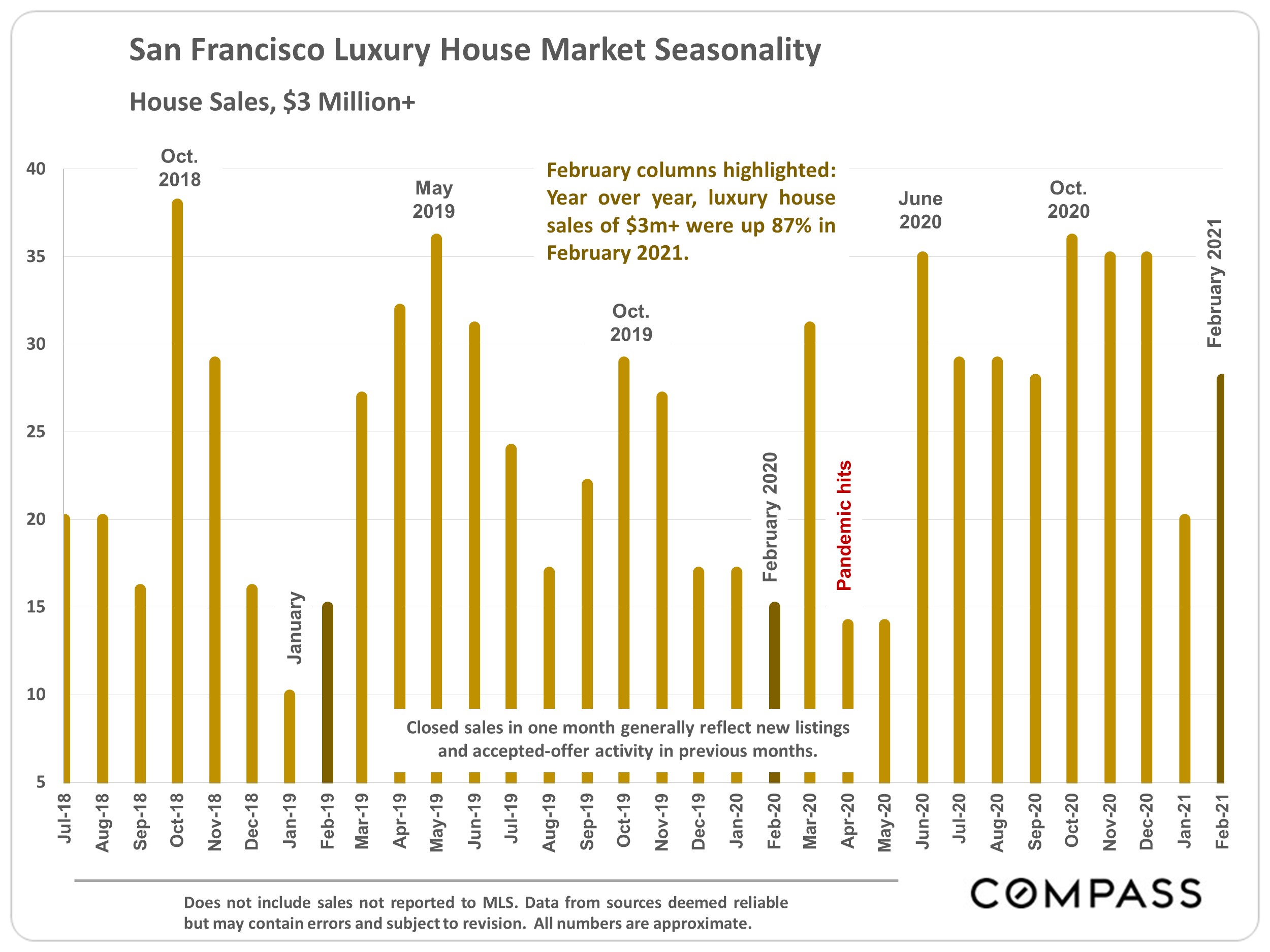

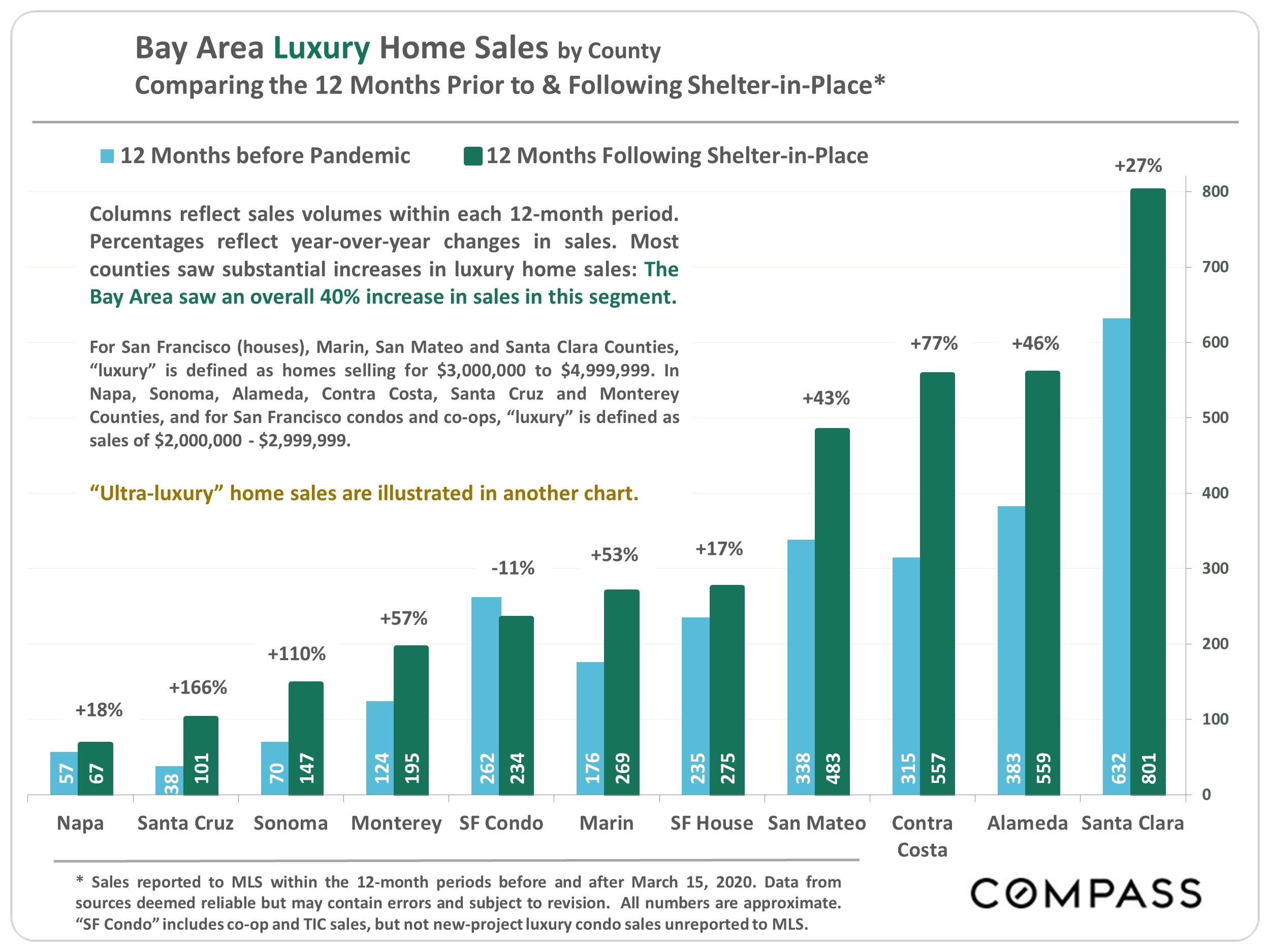

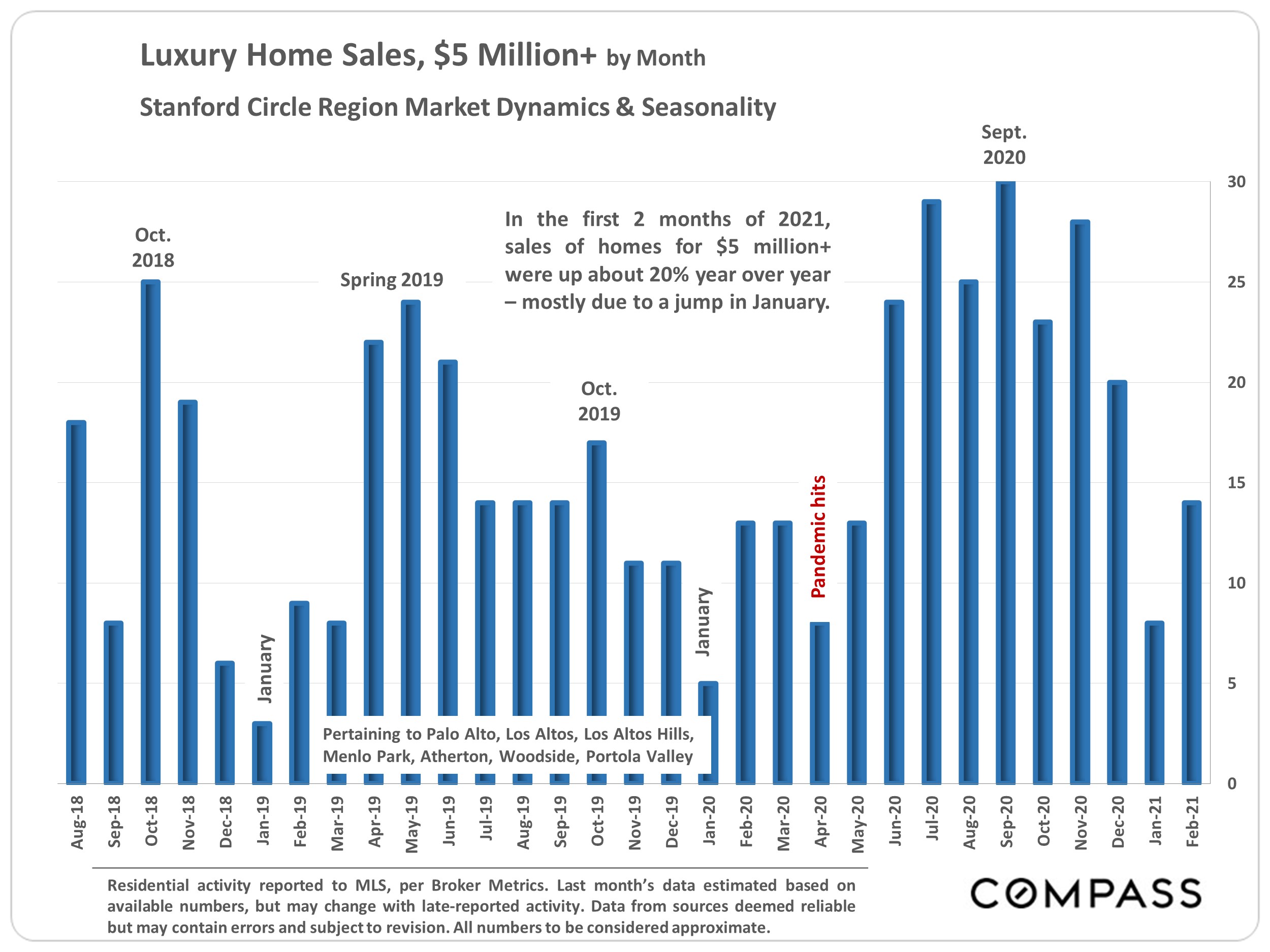

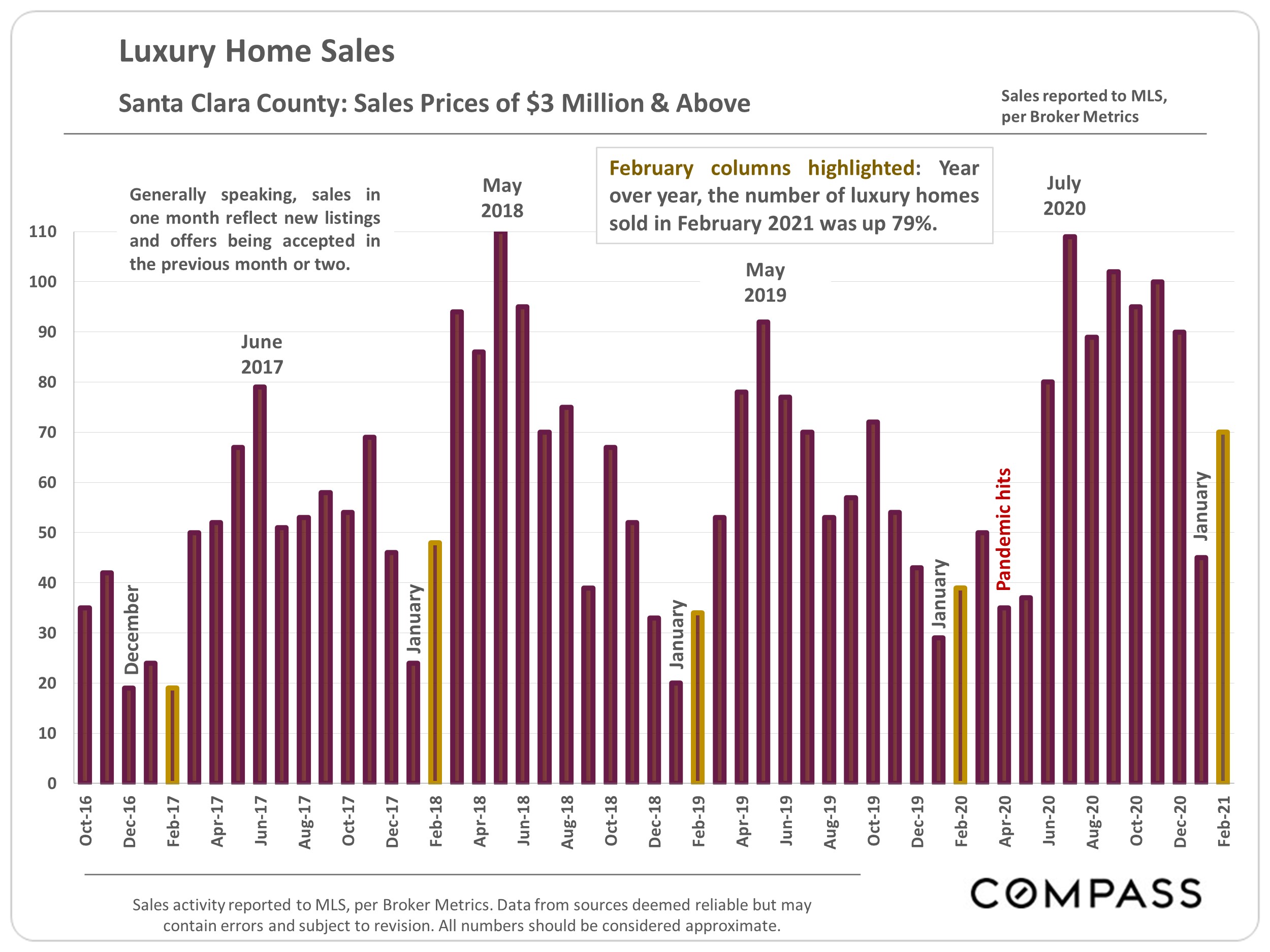

Luxury House Sales up 87%

At the beginning of the new year, it is not unusual for buyers (demand) to jump back in much sooner than sellers (new listings – supply), a dynamic which commonly

accelerates as spring gets underway. When demand surges while new listings lag behind, buyers must increasingly compete, often heatedly, for appealing homes. This

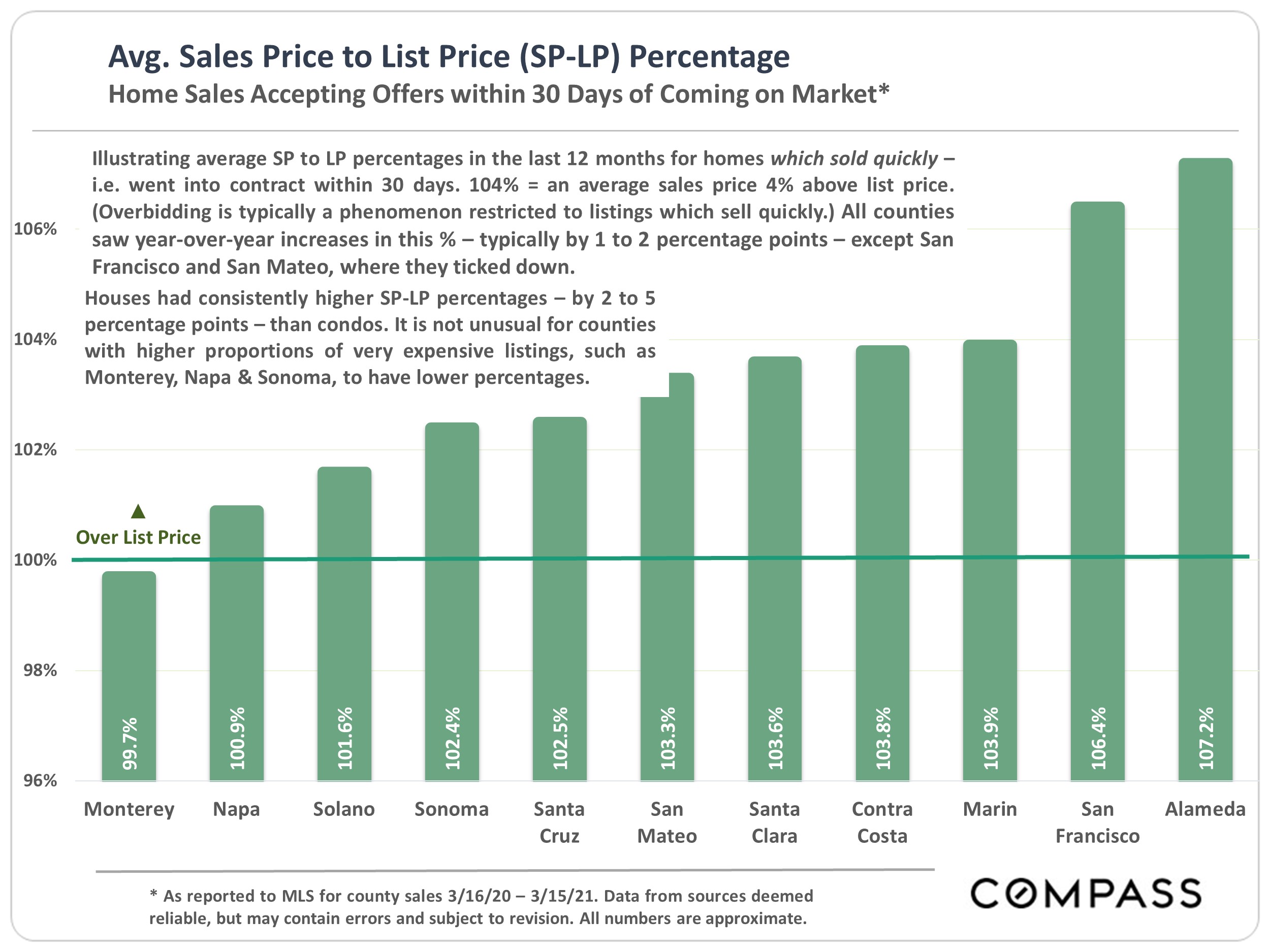

imbalance in supply and demand adds considerable pressure to the market, with overbidding and price increases becoming much more common. And this has occurred

with a vengeance in early 2021, especially within the city’s house market.

This report will look at median house and condo list and sales prices, supply and demand from a variety of angles, the surge in luxury home sales, home prices along

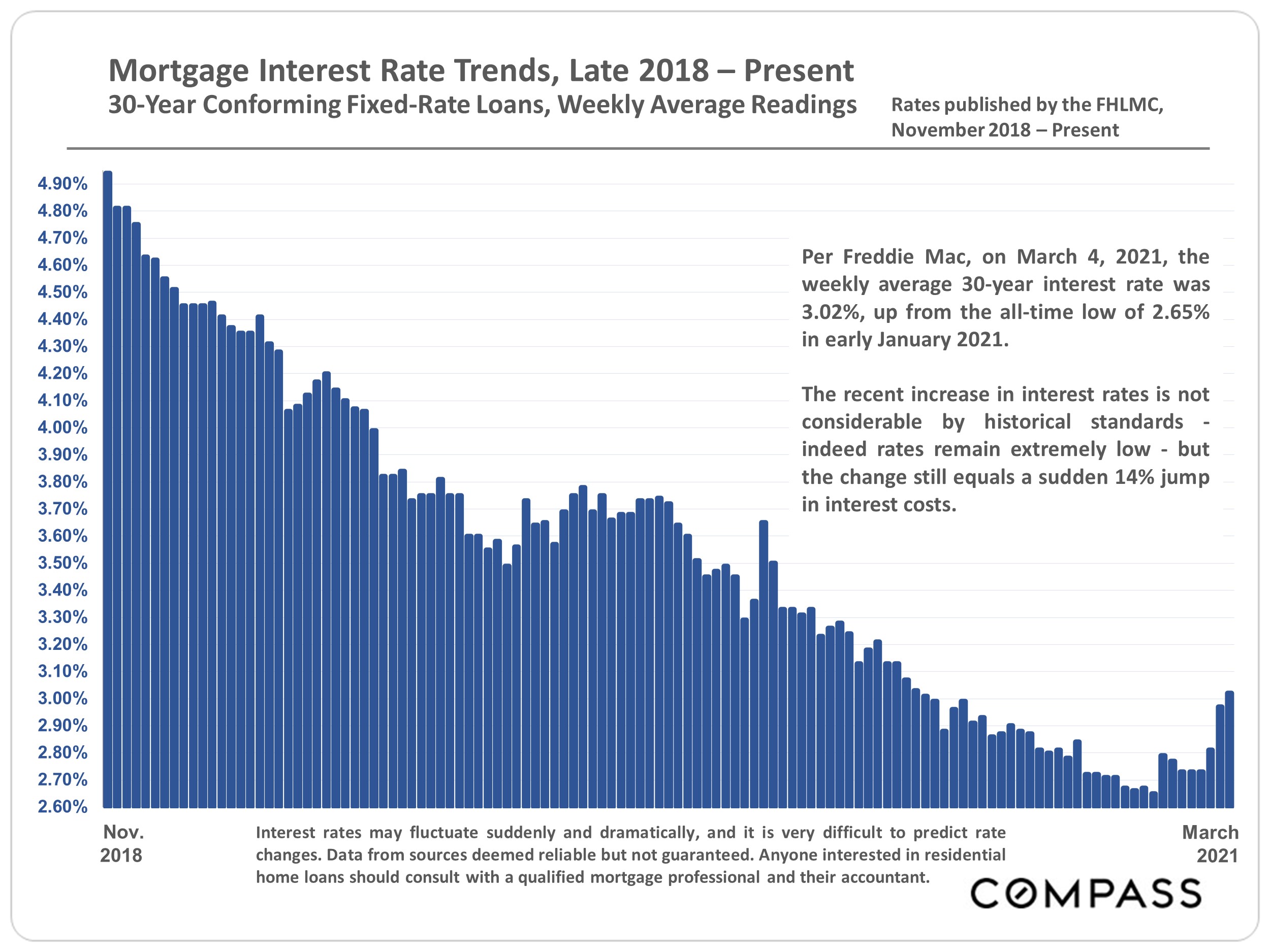

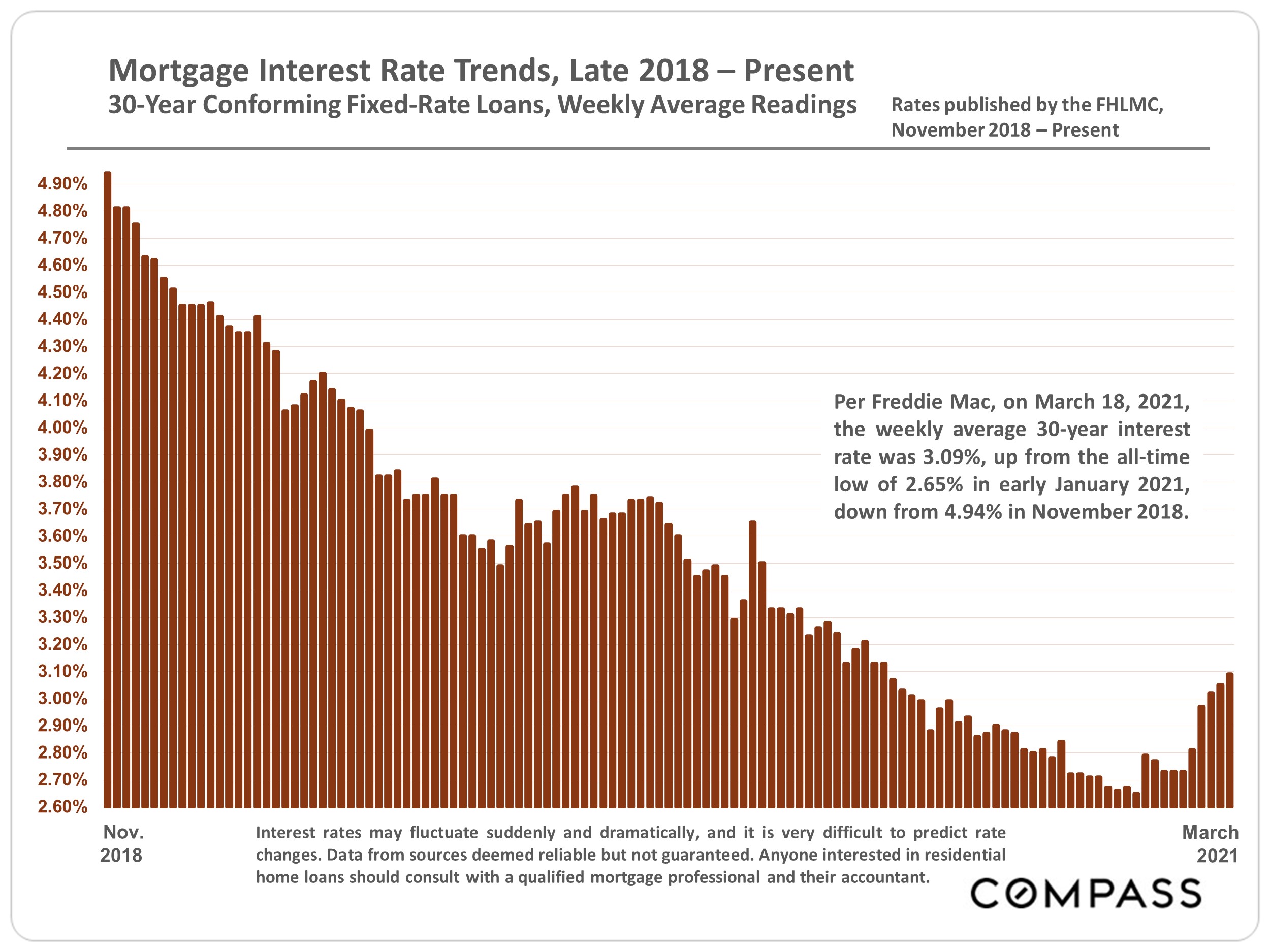

the Bay Area coast, and the recent jump in interest rates.

The charts are meant to be self-explanatory, but your questions are always welcome.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

Statistics are generalities, essentially summaries of data generated by dozens, hundreds or thousands of unique, individual sales. They are best seen not as precise measurements, but as broad, comparative indicators with reasonable margins of error – and how they apply to any particular property is unknown without a specific comparative market analysis. Anomalous fluctuations in statistics are not uncommon, especially in smaller markets with fewer sales and wide ranges in sales prices. Longer-term trends are typically more meaningful than short-term changes. Data from sources deemed reliable, but may contain errors and subject to revision. Some analyses pertain to different selections of counties, depending on data source. All numbers are approximate.

Selected Highlights:

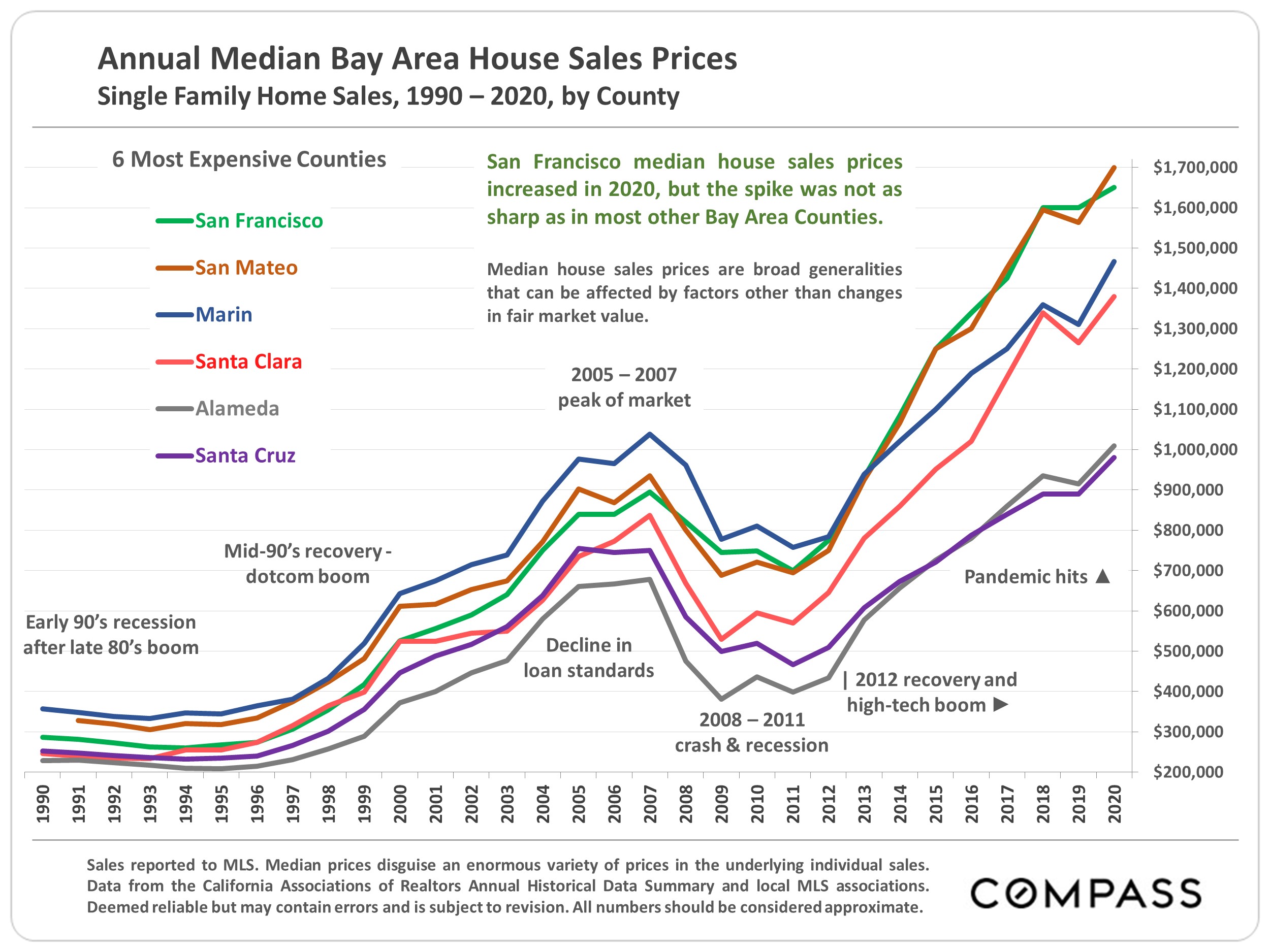

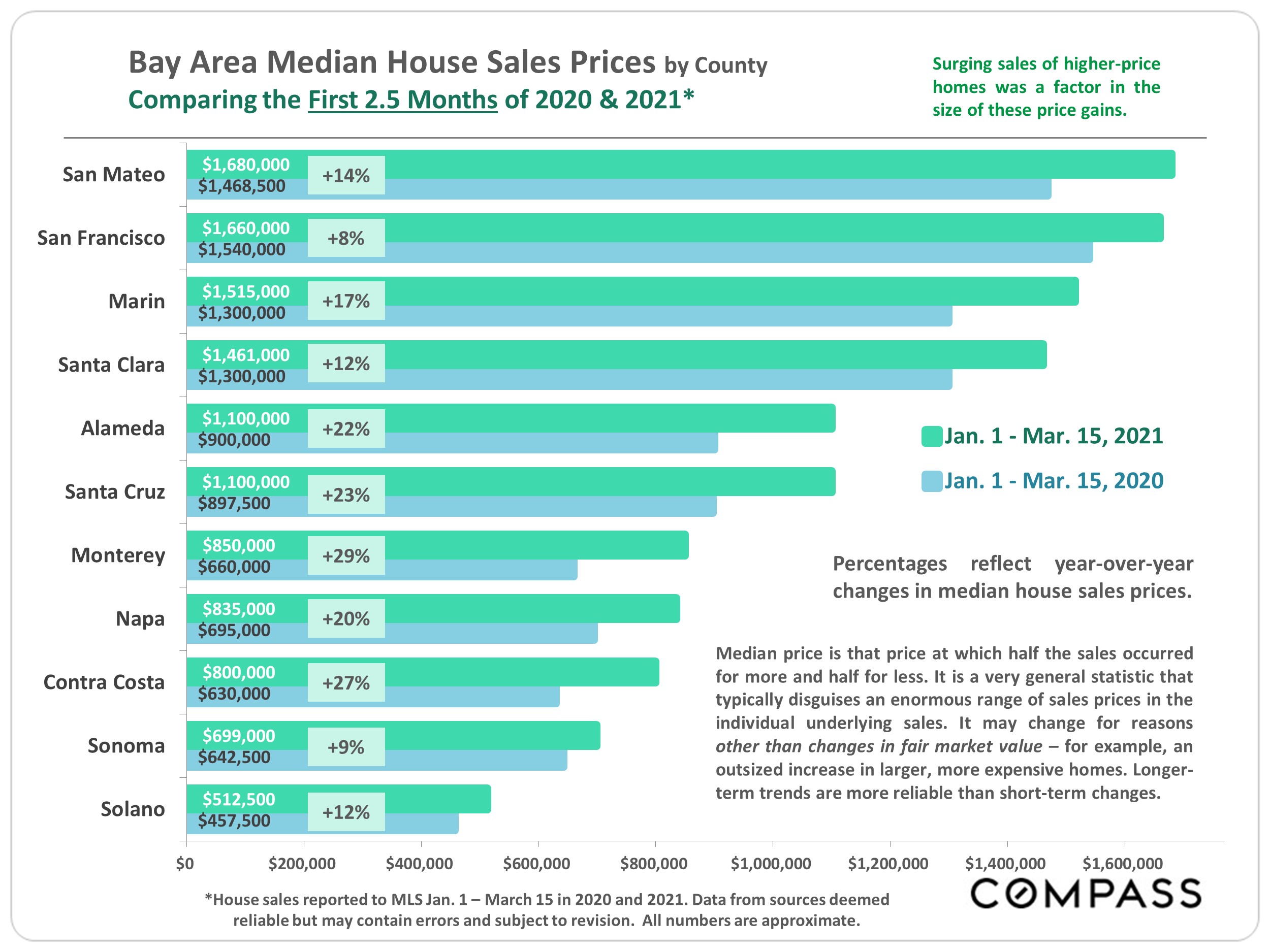

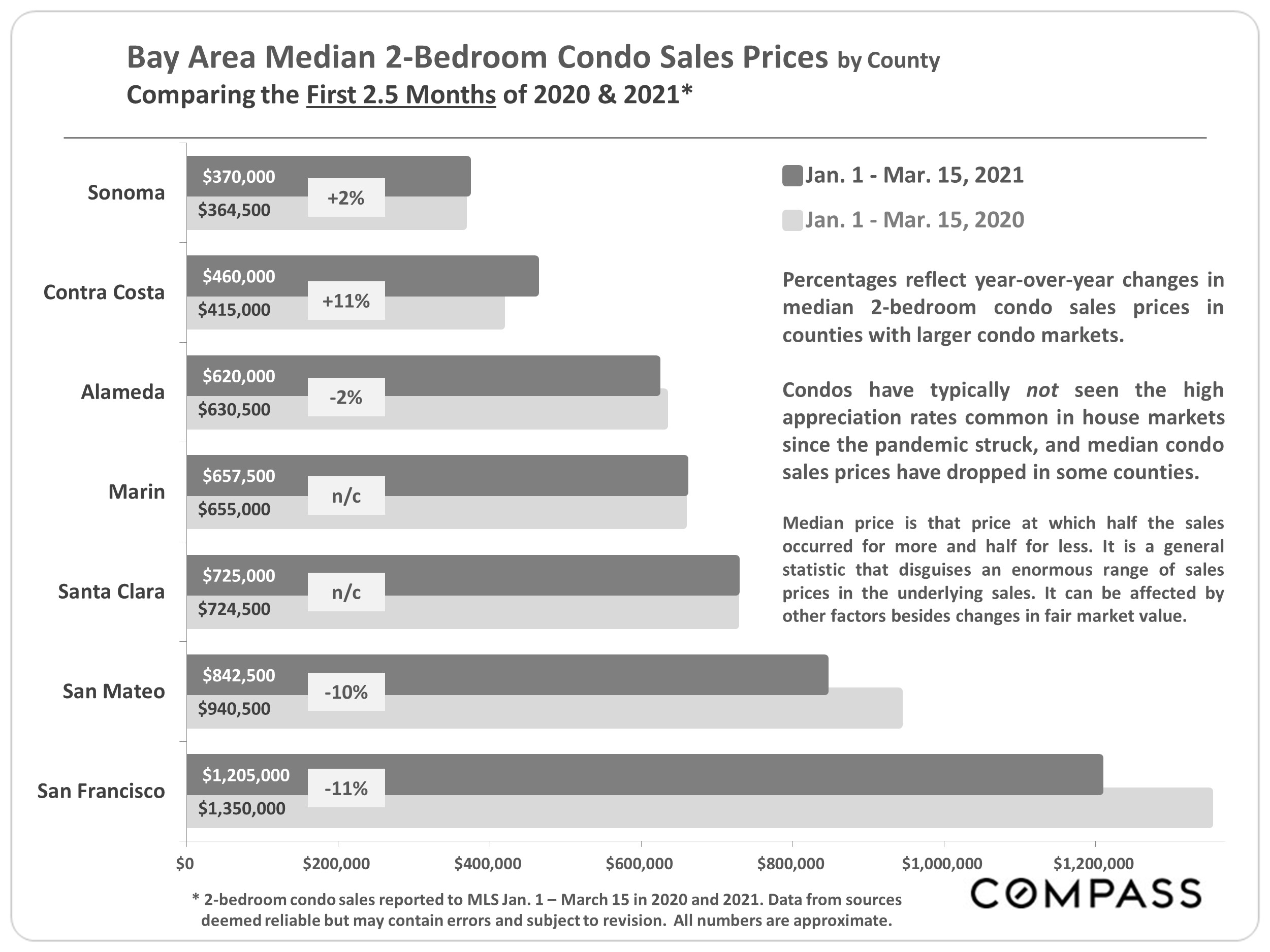

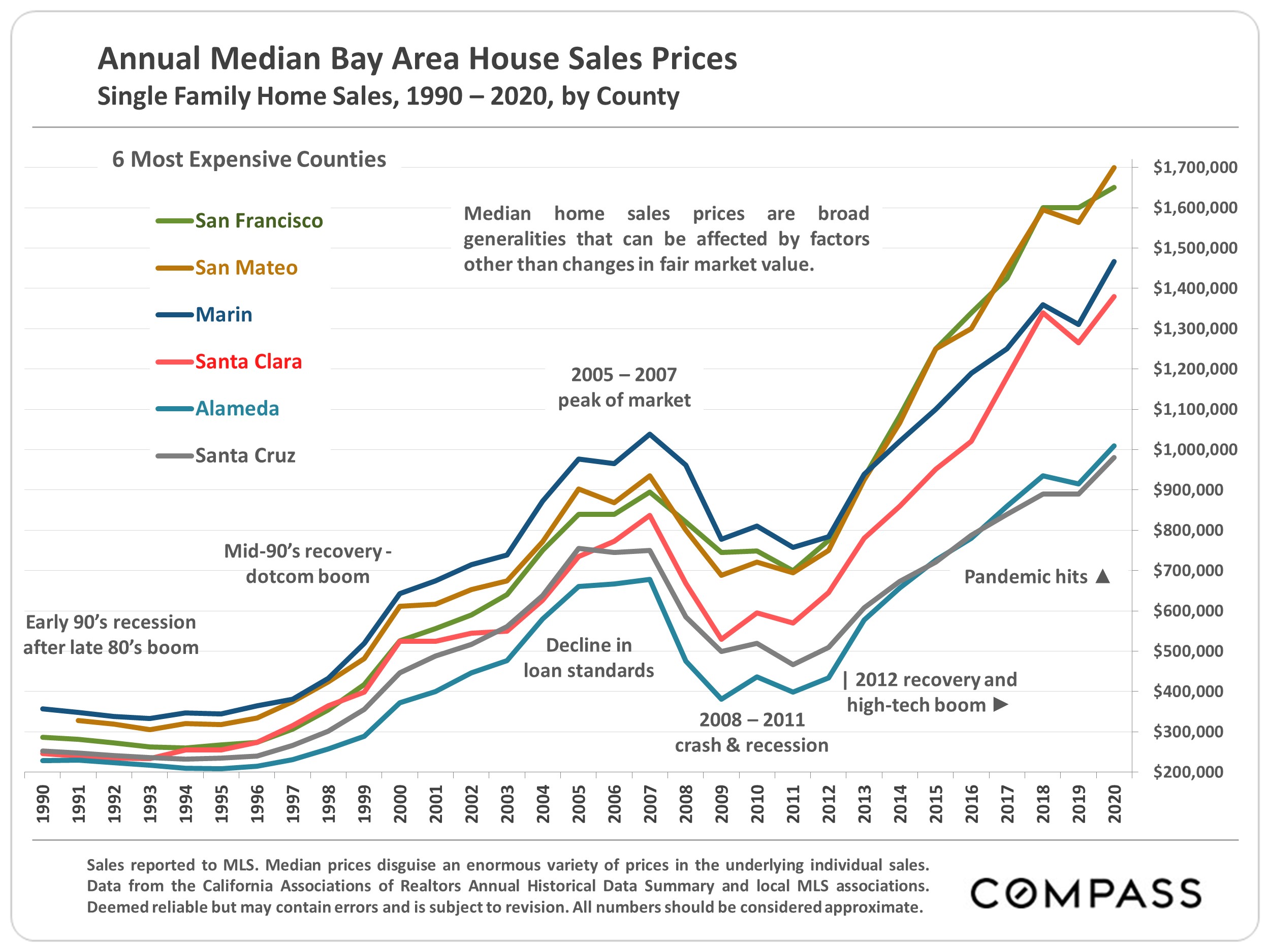

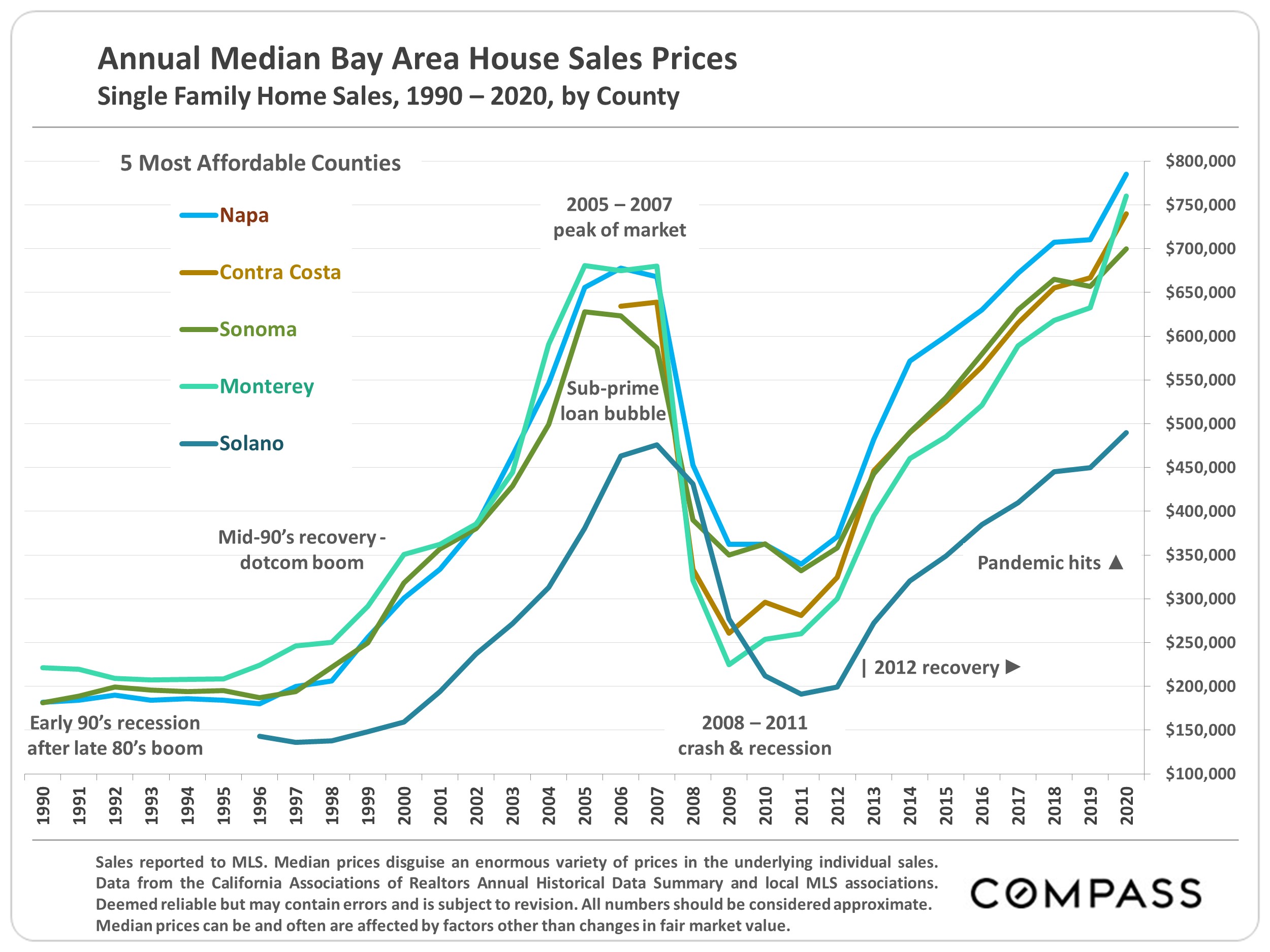

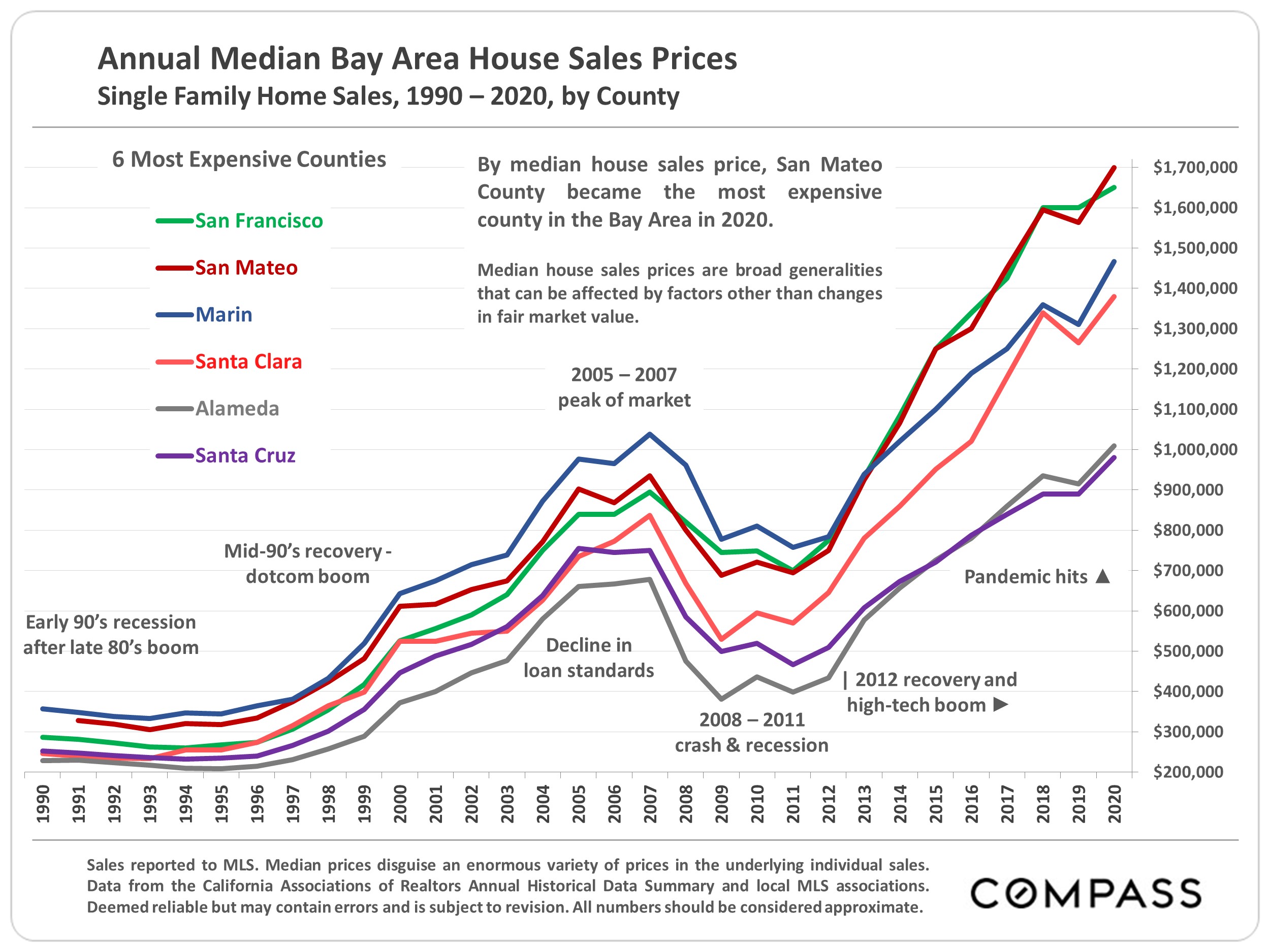

The first 21⁄2 months of 2021 saw year-over-year, median house sales price increases of 8% to 29% depending on county. (The picture for median condo prices was different.)

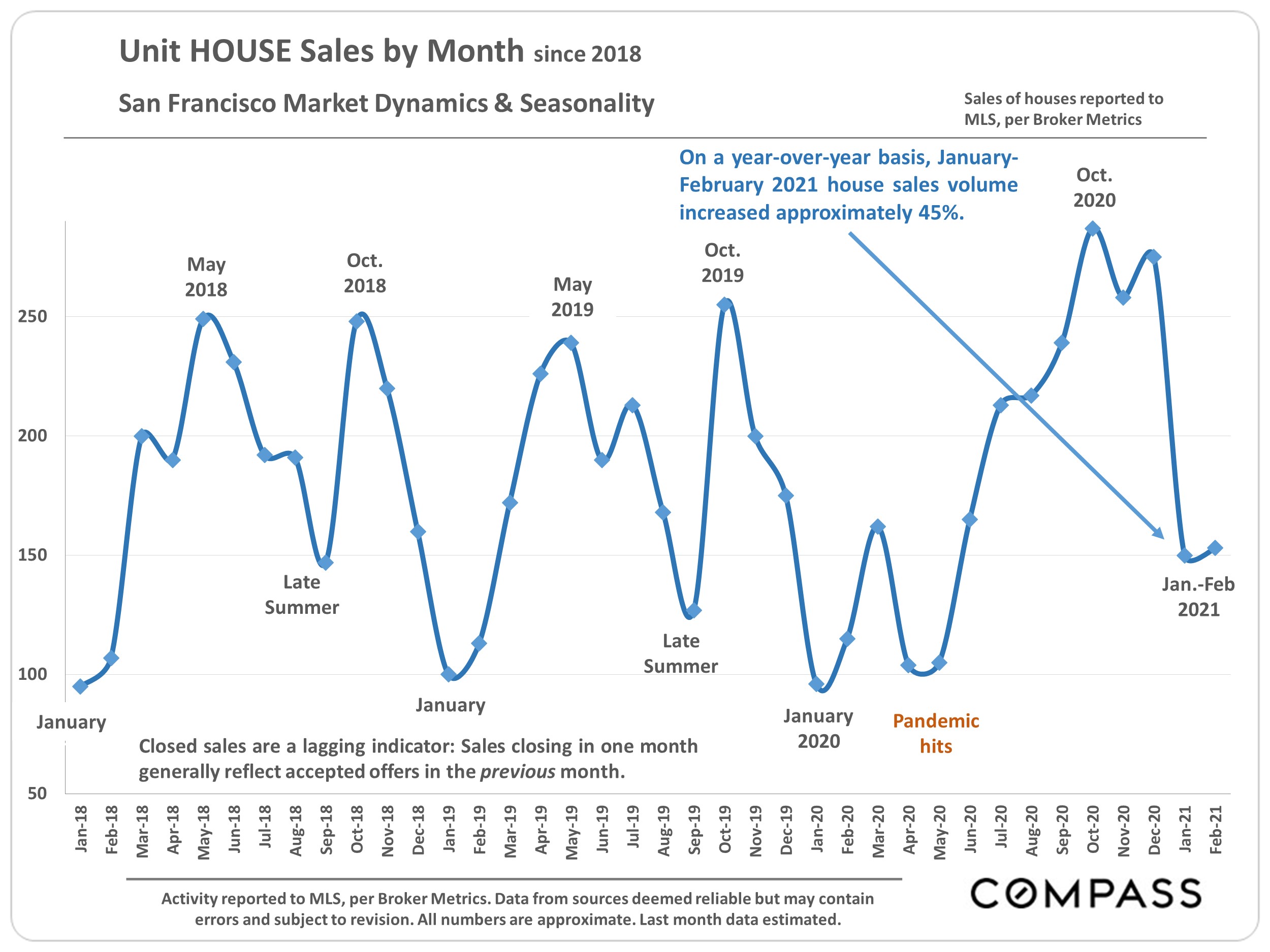

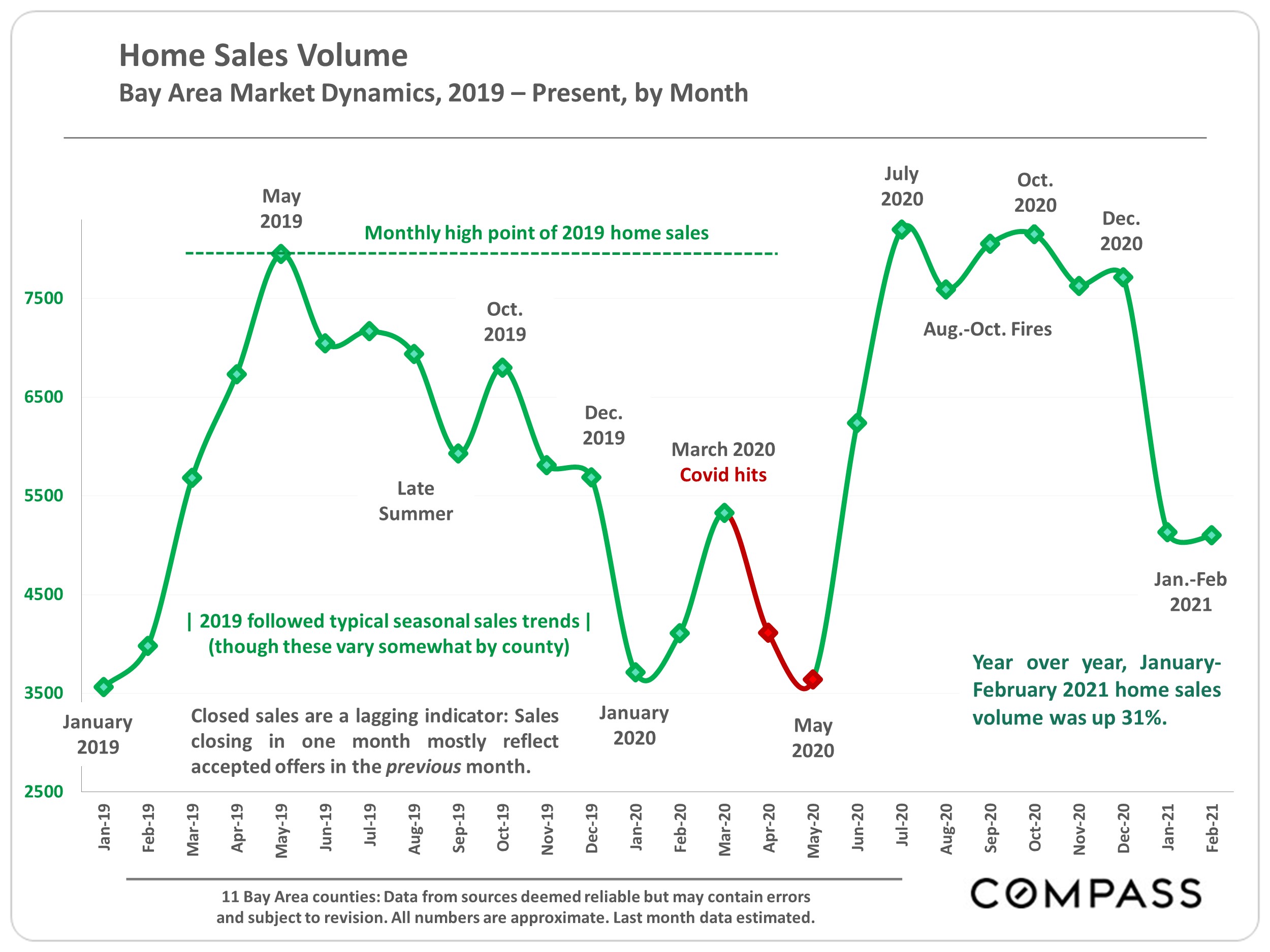

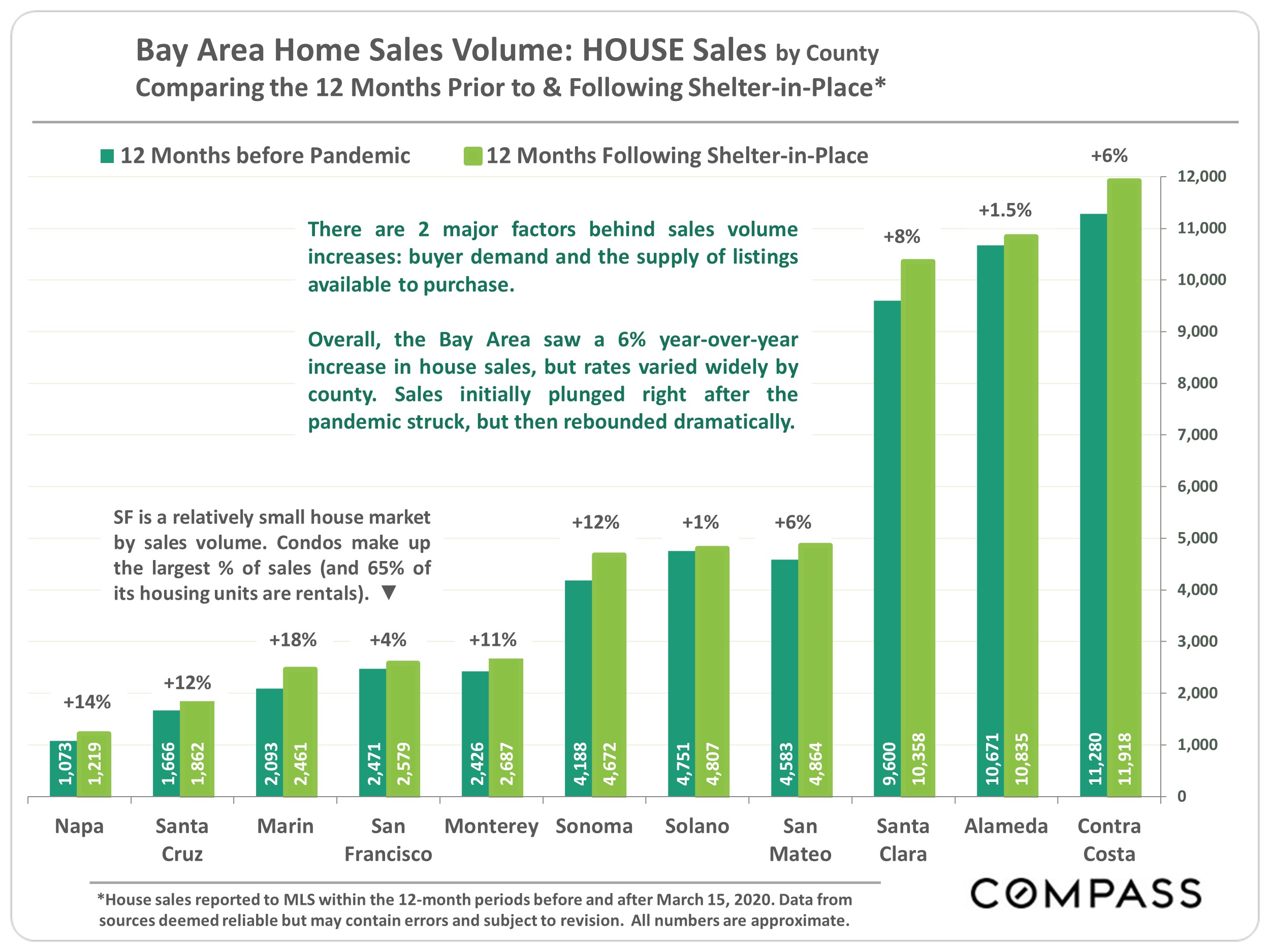

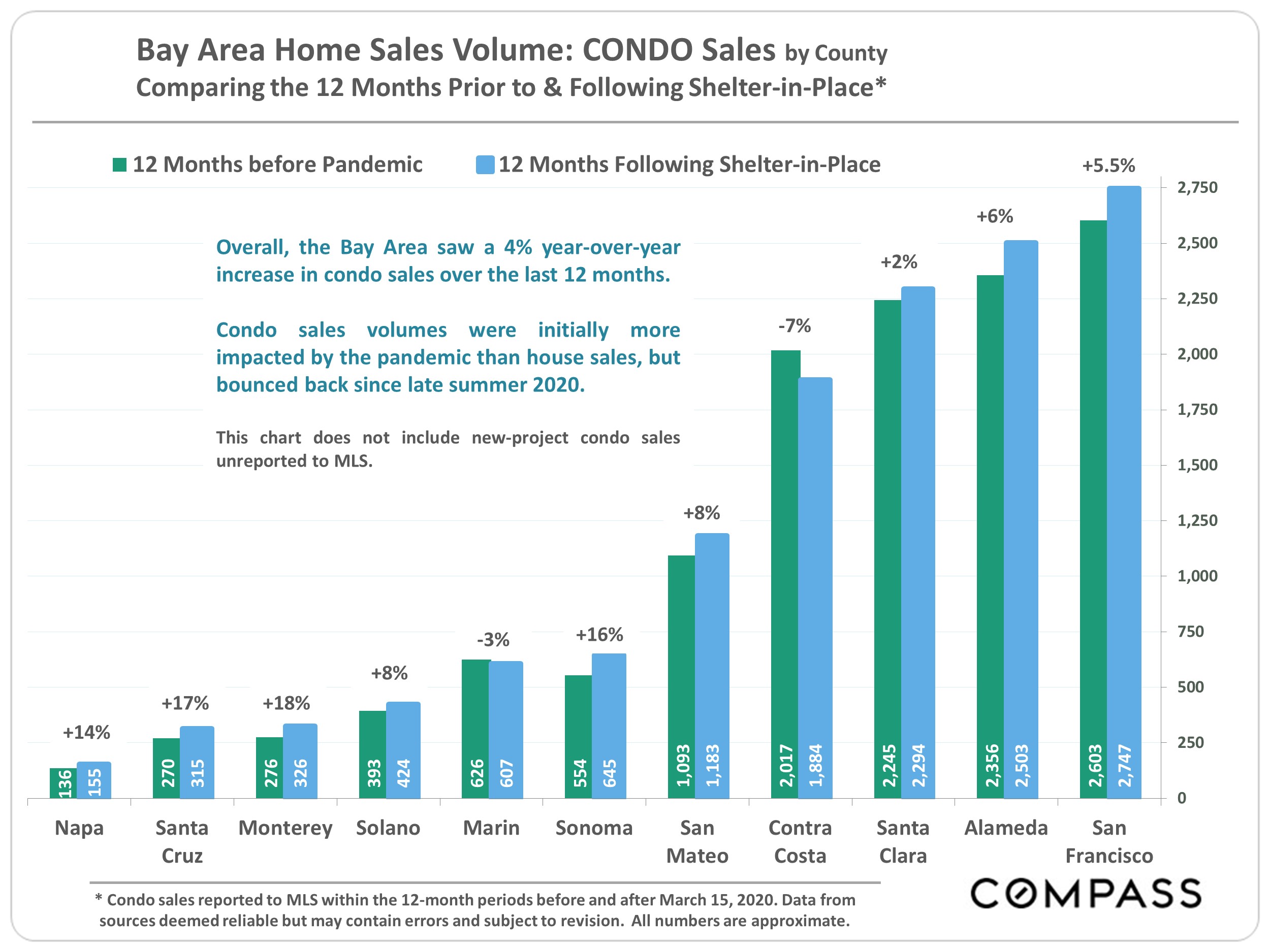

With the recovery from the initial April-May 2020 crash in activity, home sales of all prices and property types increased 6% in the 12 months since March 15, 2020.

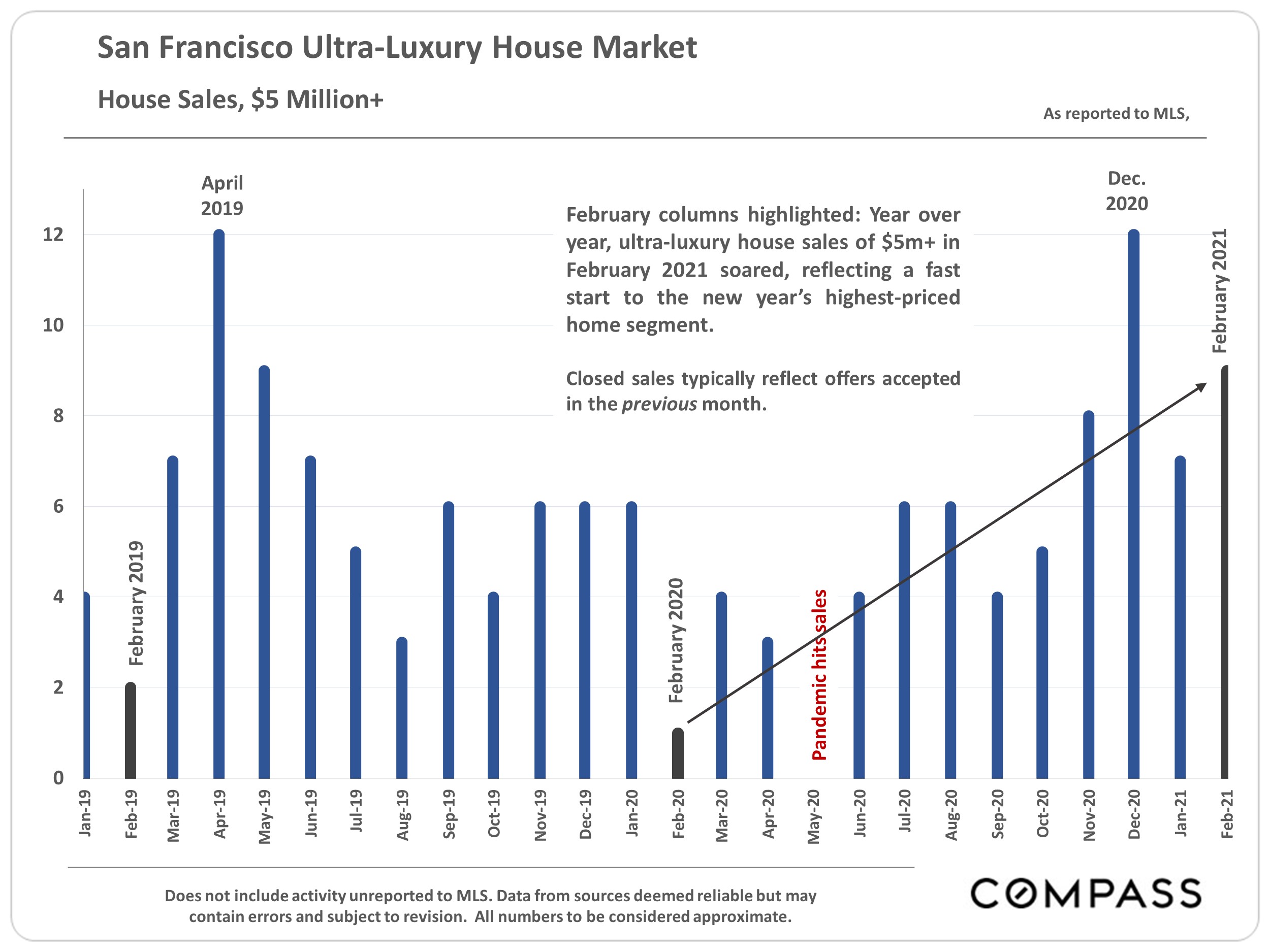

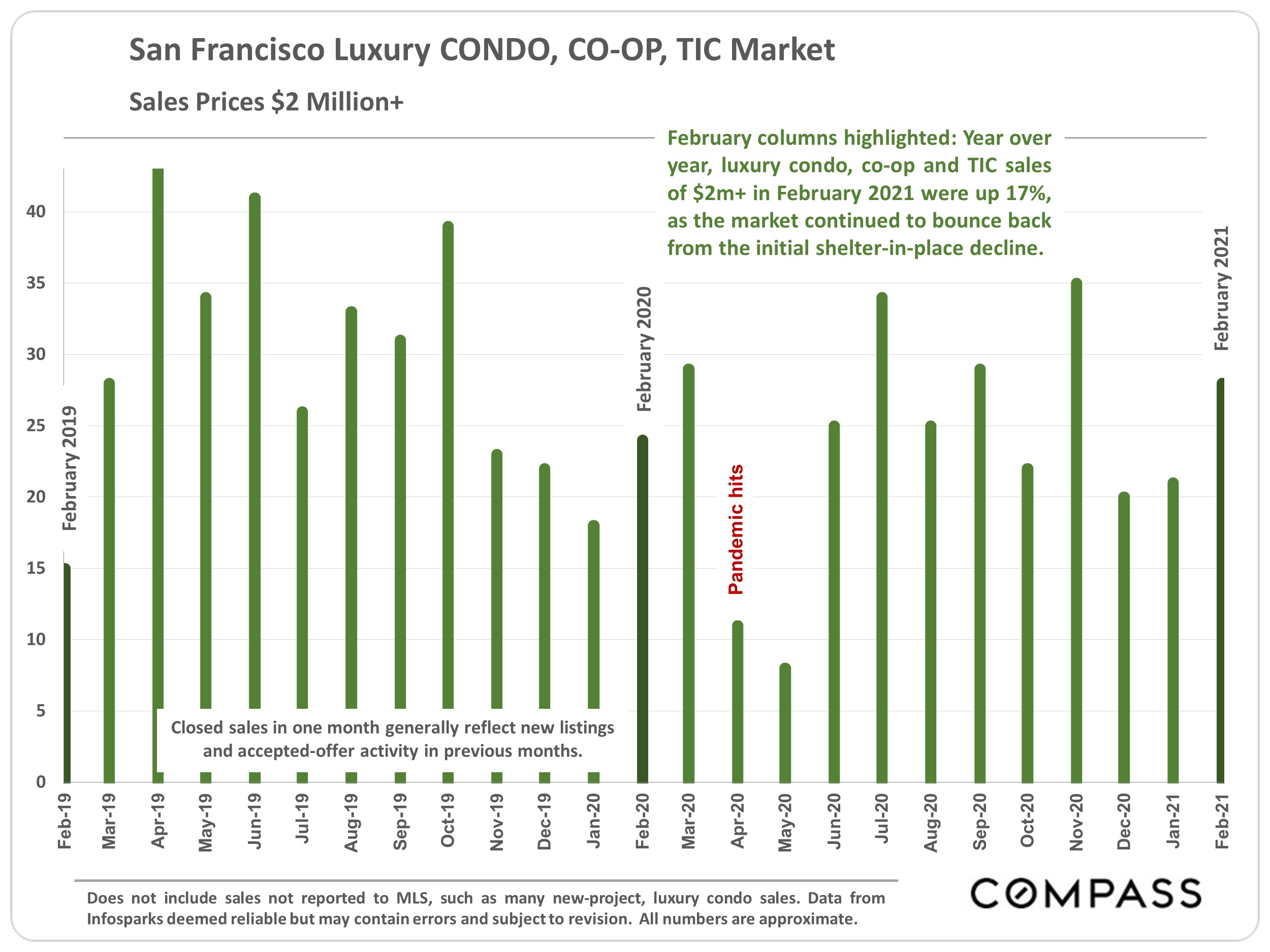

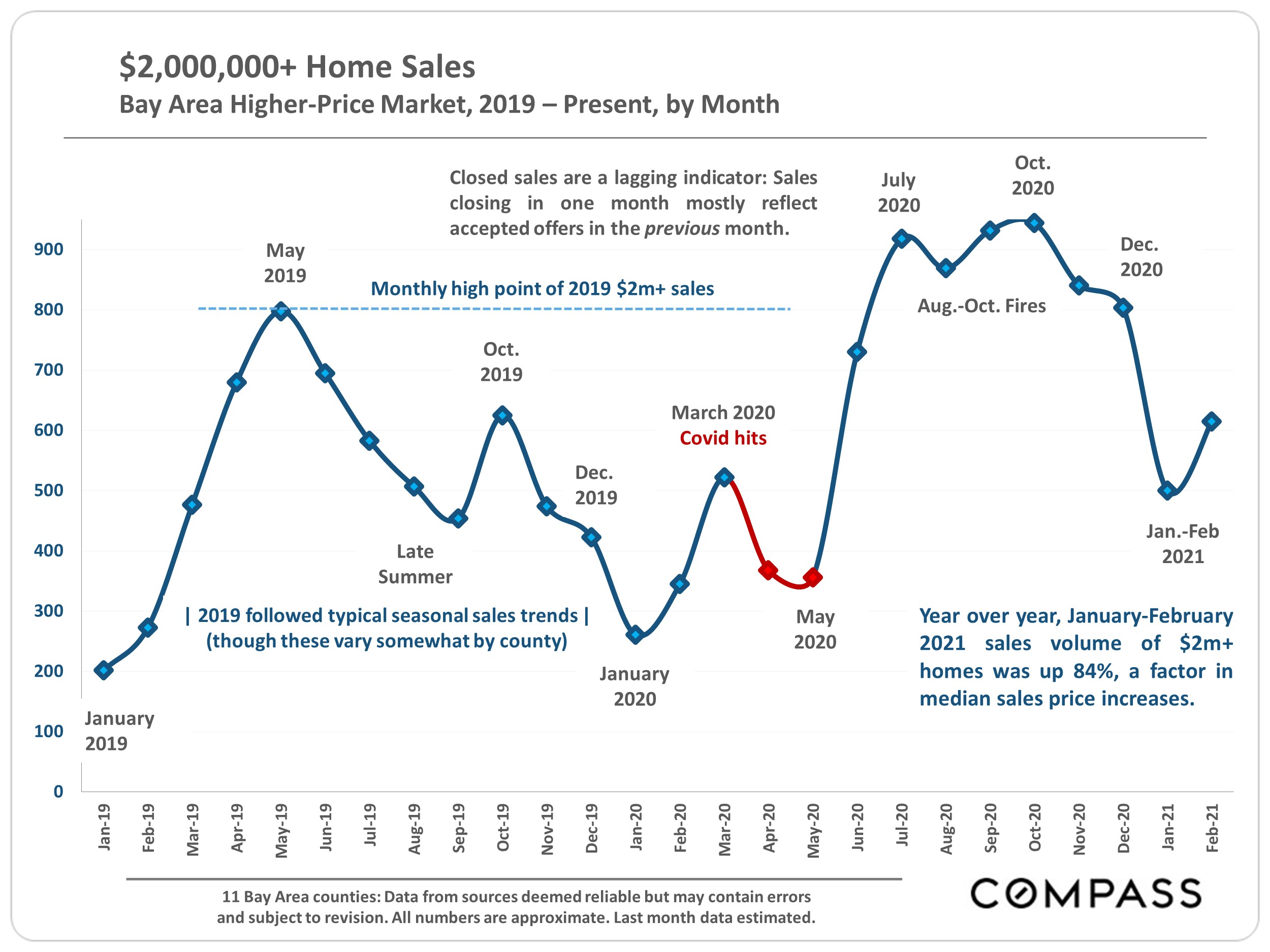

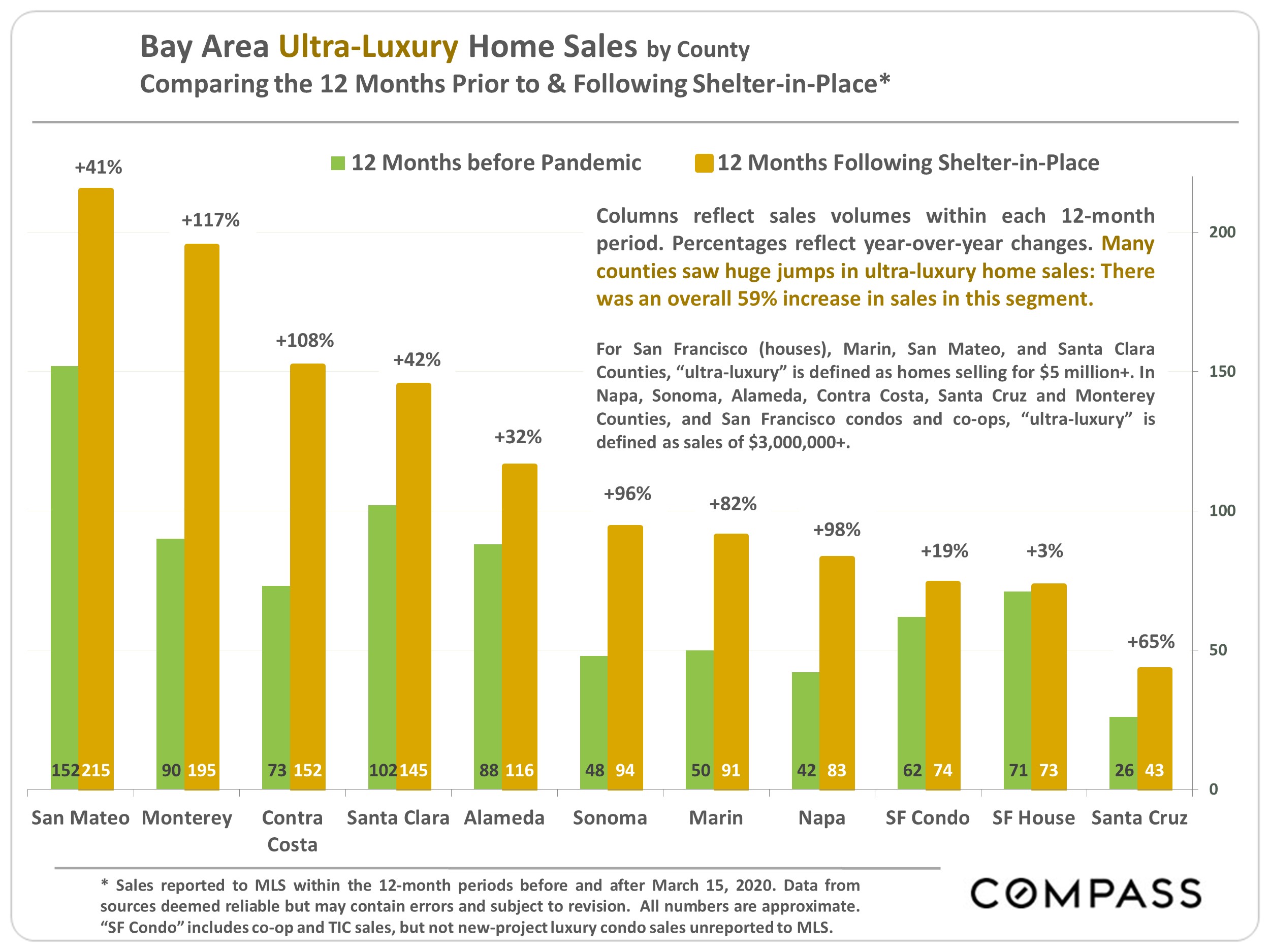

Since shelter-in-place was first introduced, luxury home sales were up 40% year-over-year and ultra-luxury home sales were up 59%. (Price thresholds for these categories are explained within the report.)

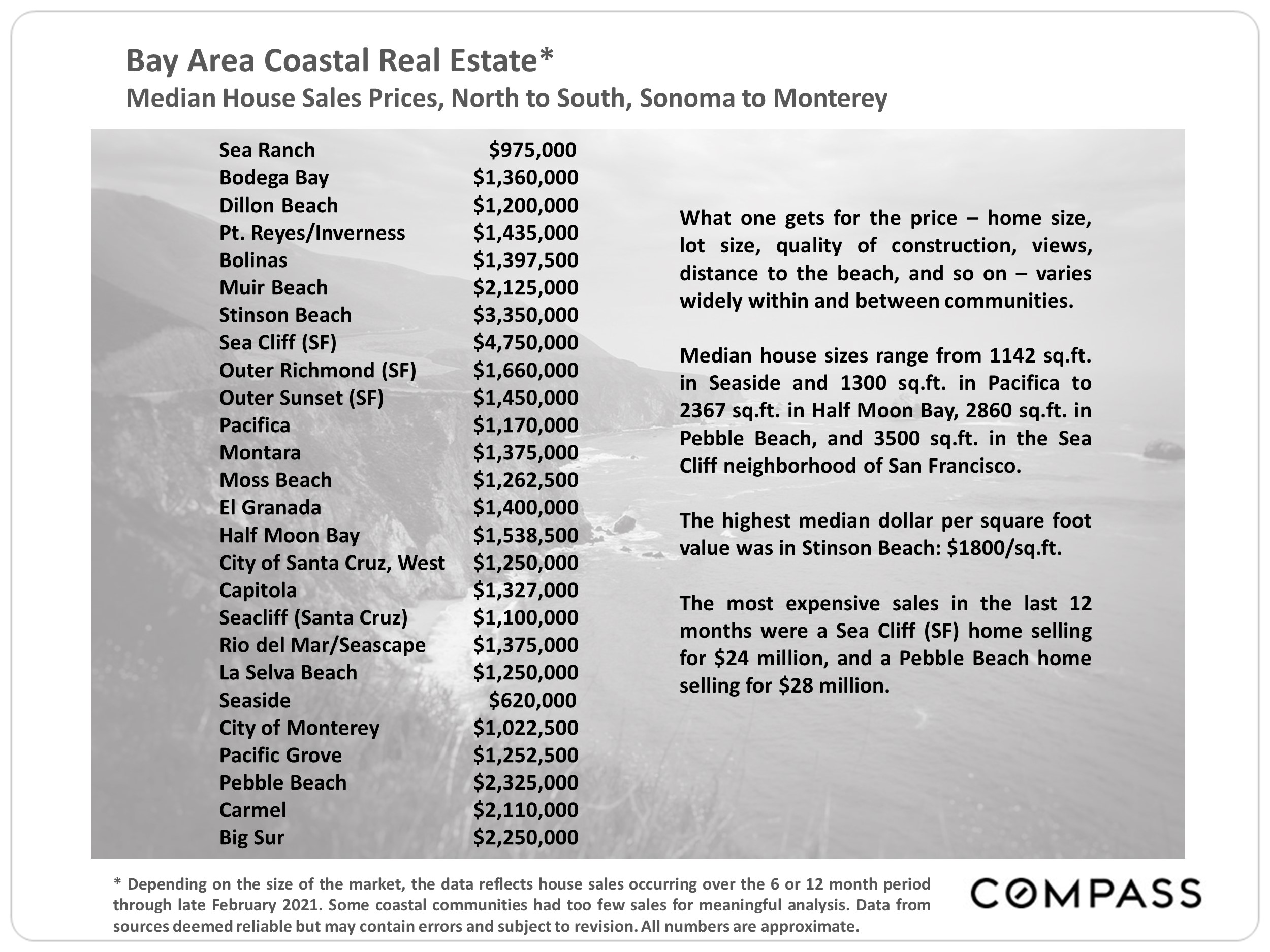

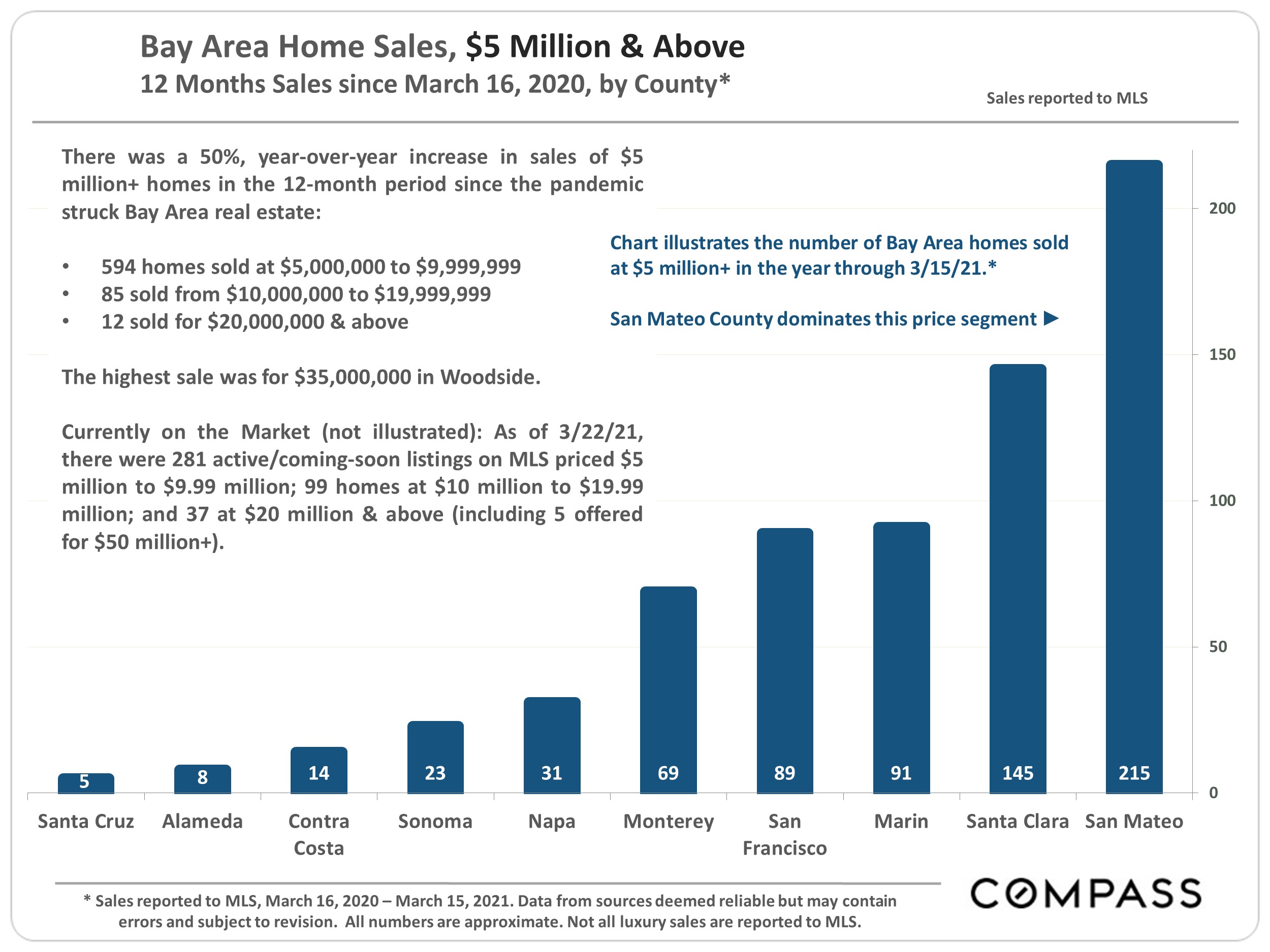

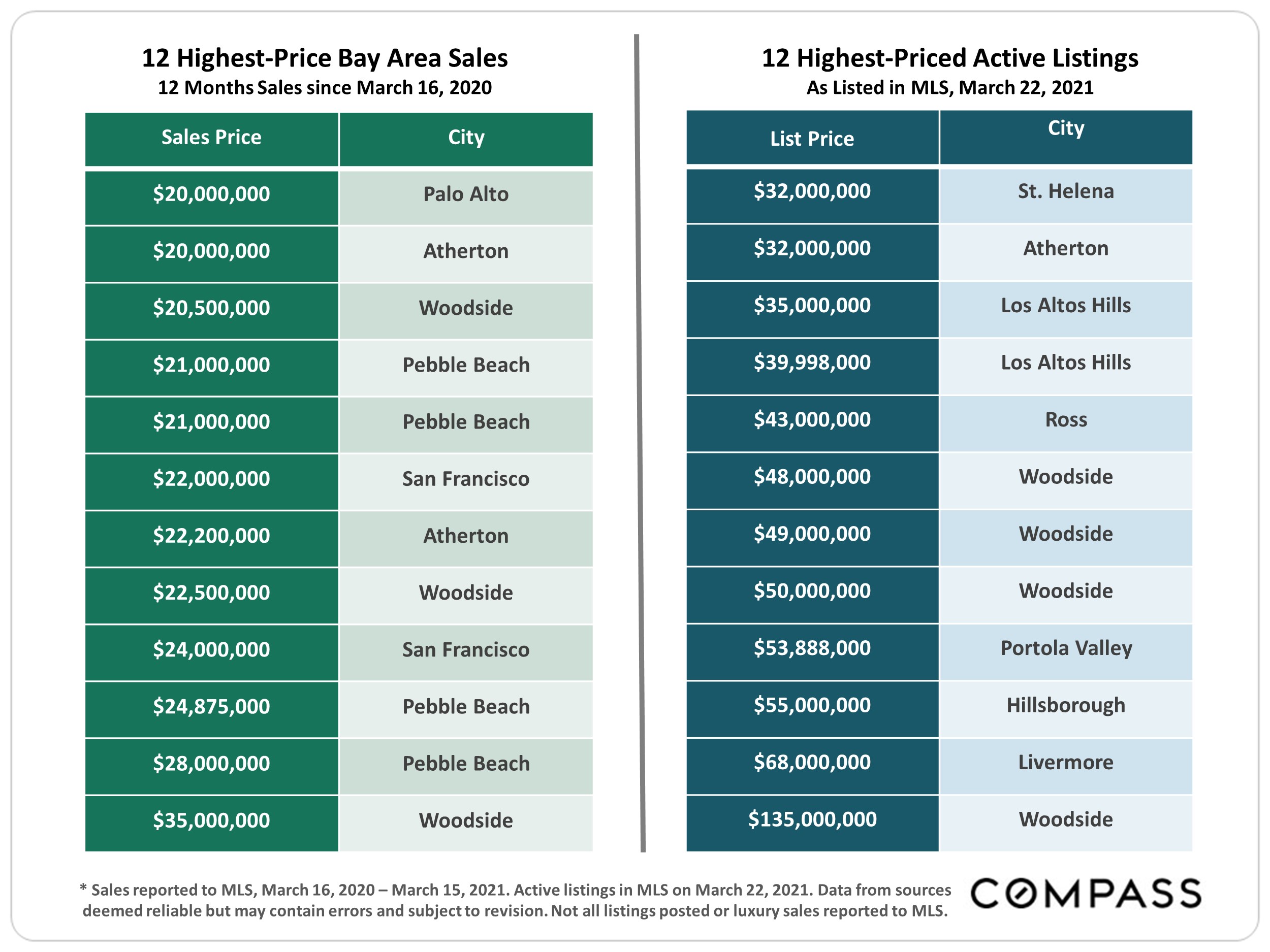

The 12 biggest sales in the greater Bay Area over the past year ranged from $20 million to $35 million. Pebble Beach in Monterey County, with 4 sales, had the highest number of these.

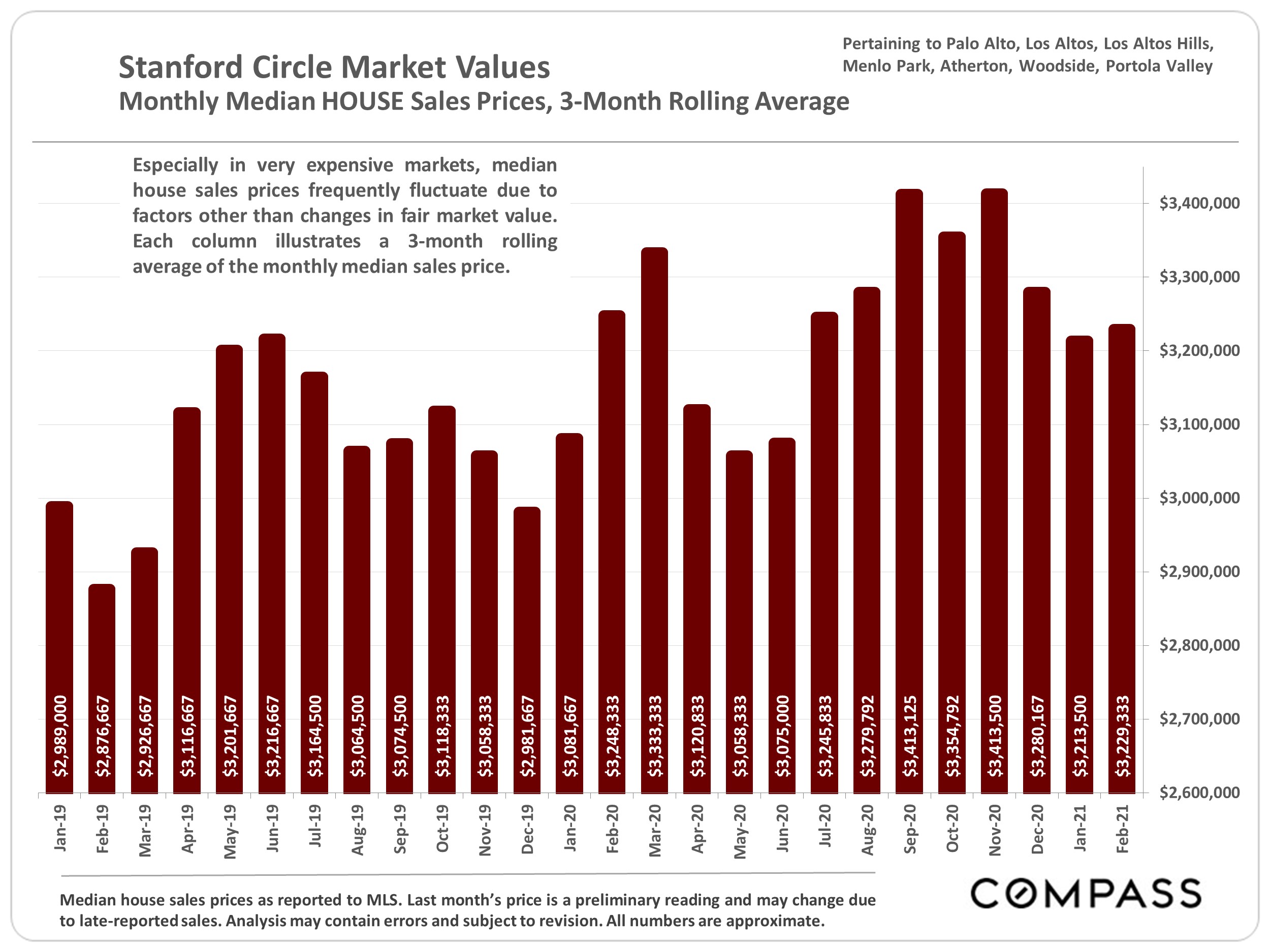

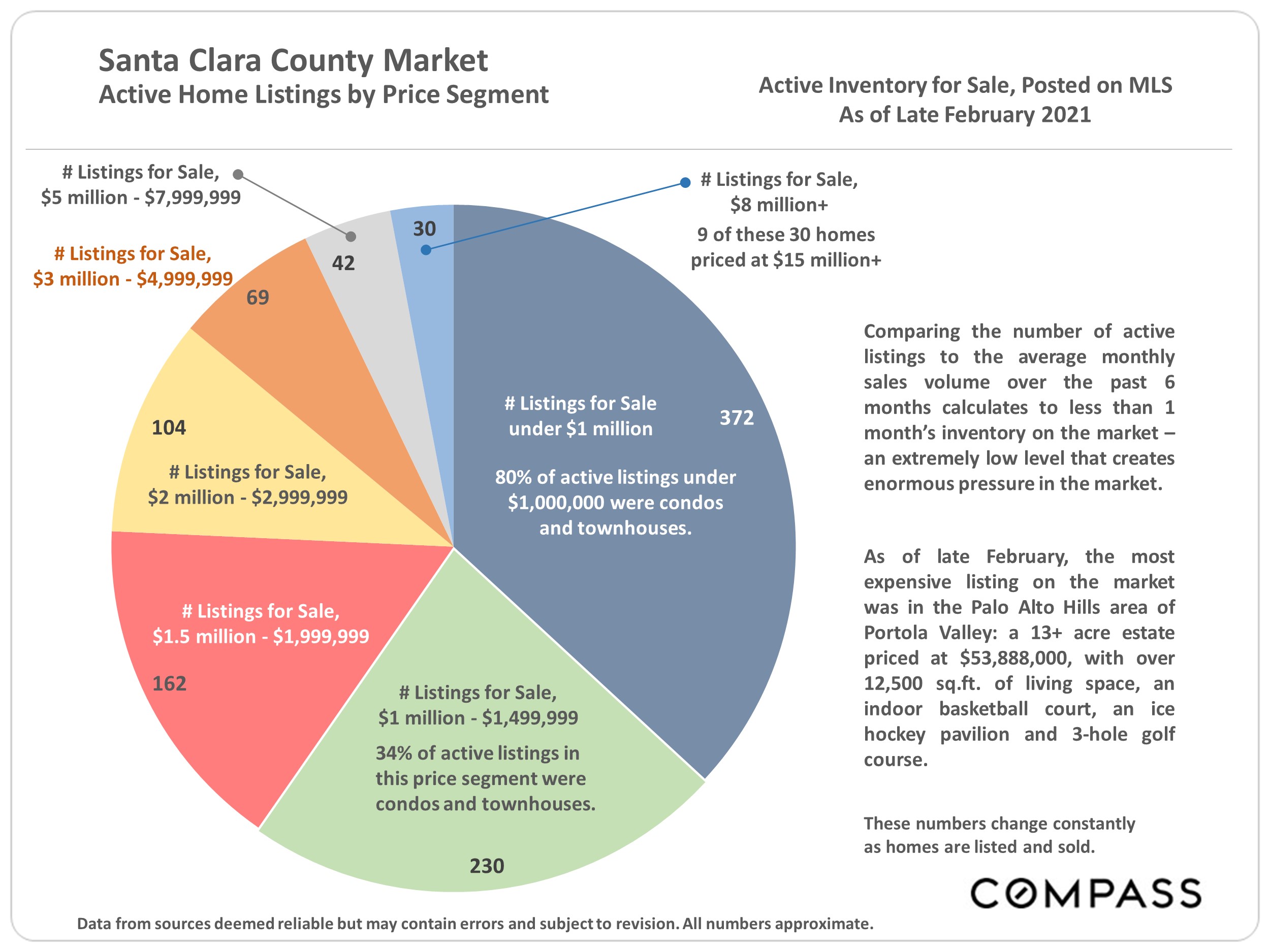

The 12 highest priced listings currently on the market range in asking price from $32 million to $135 million. Eight are located in the circle of very expensive communities surrounding Stanford

University.

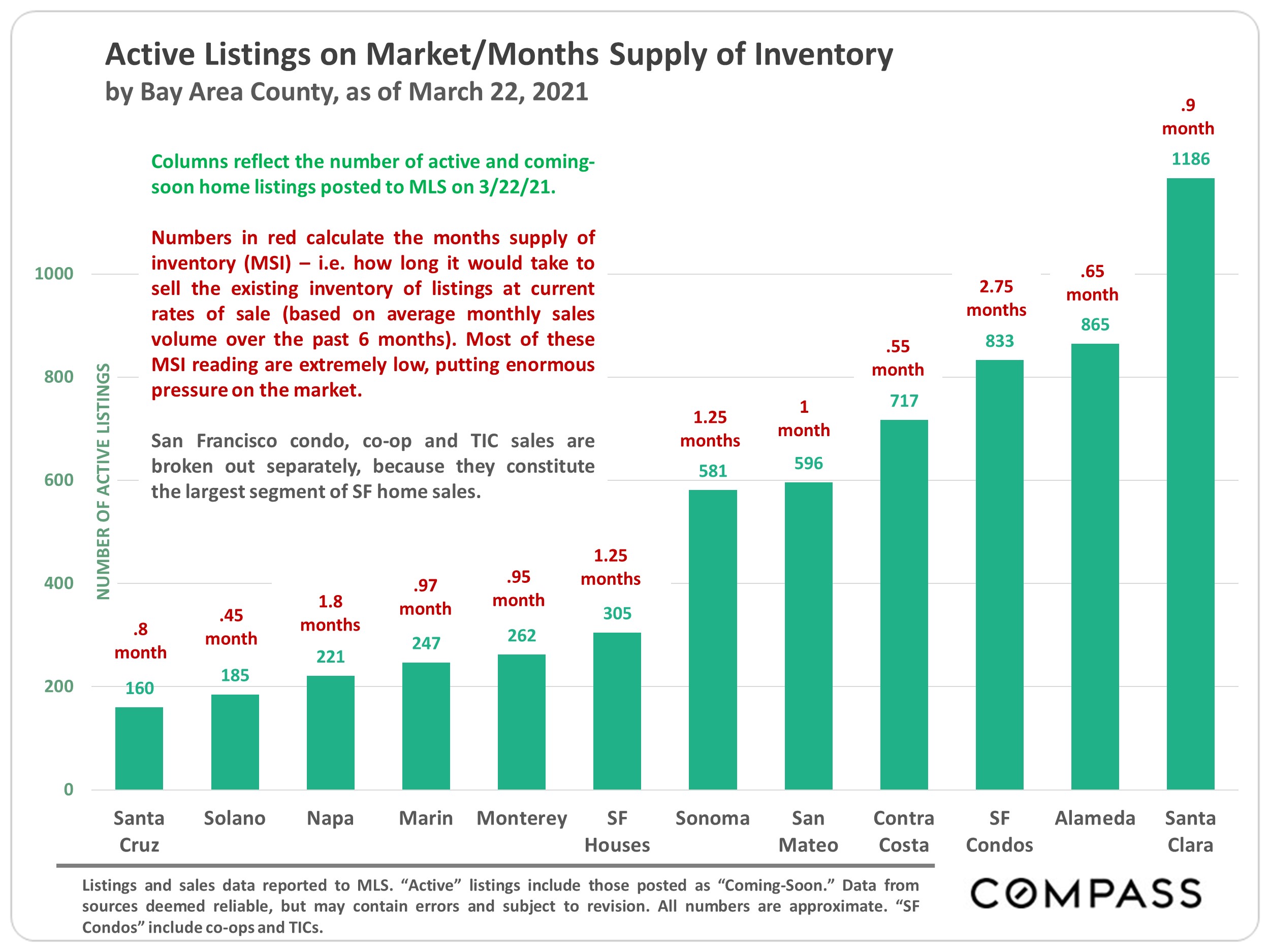

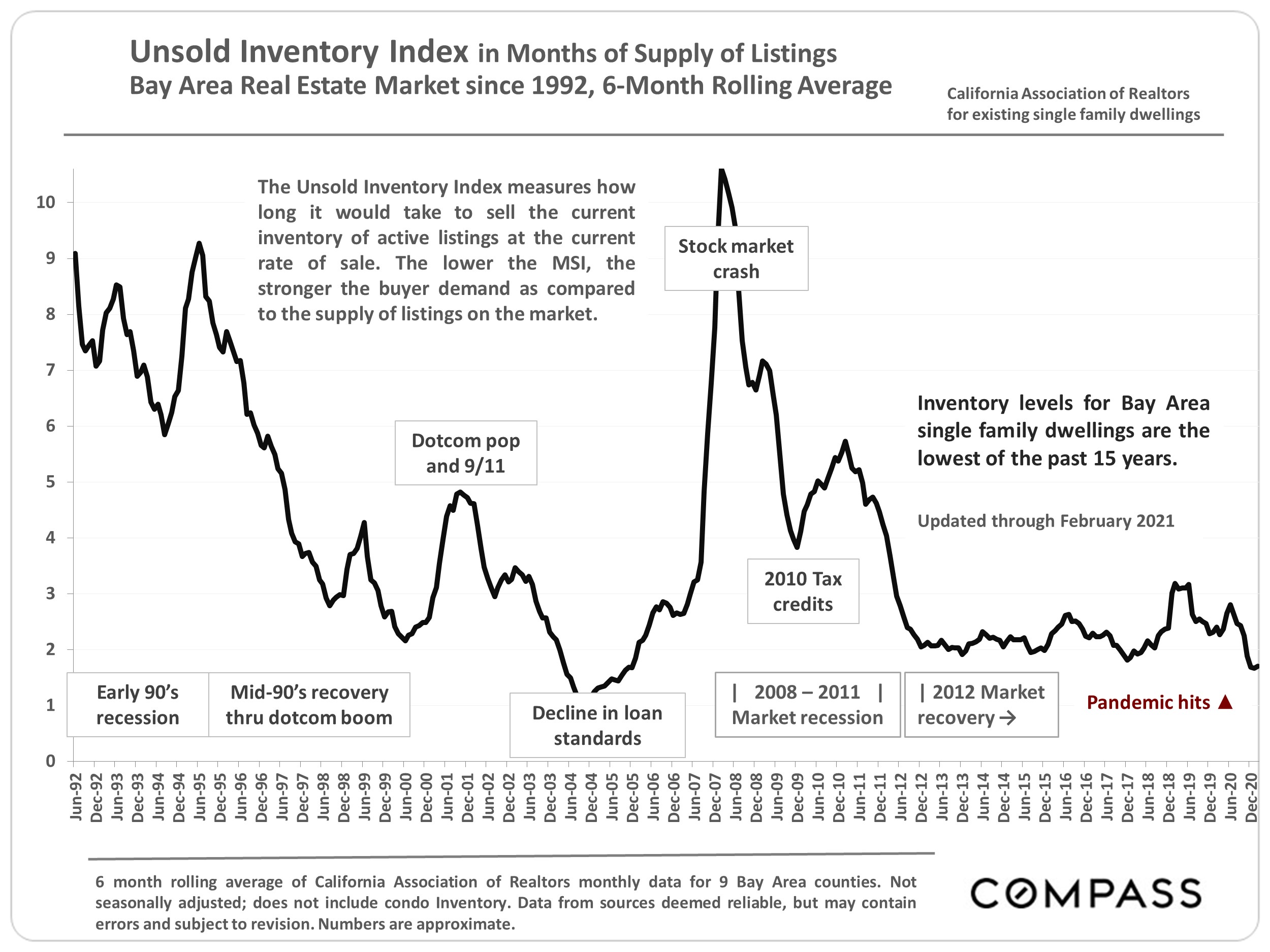

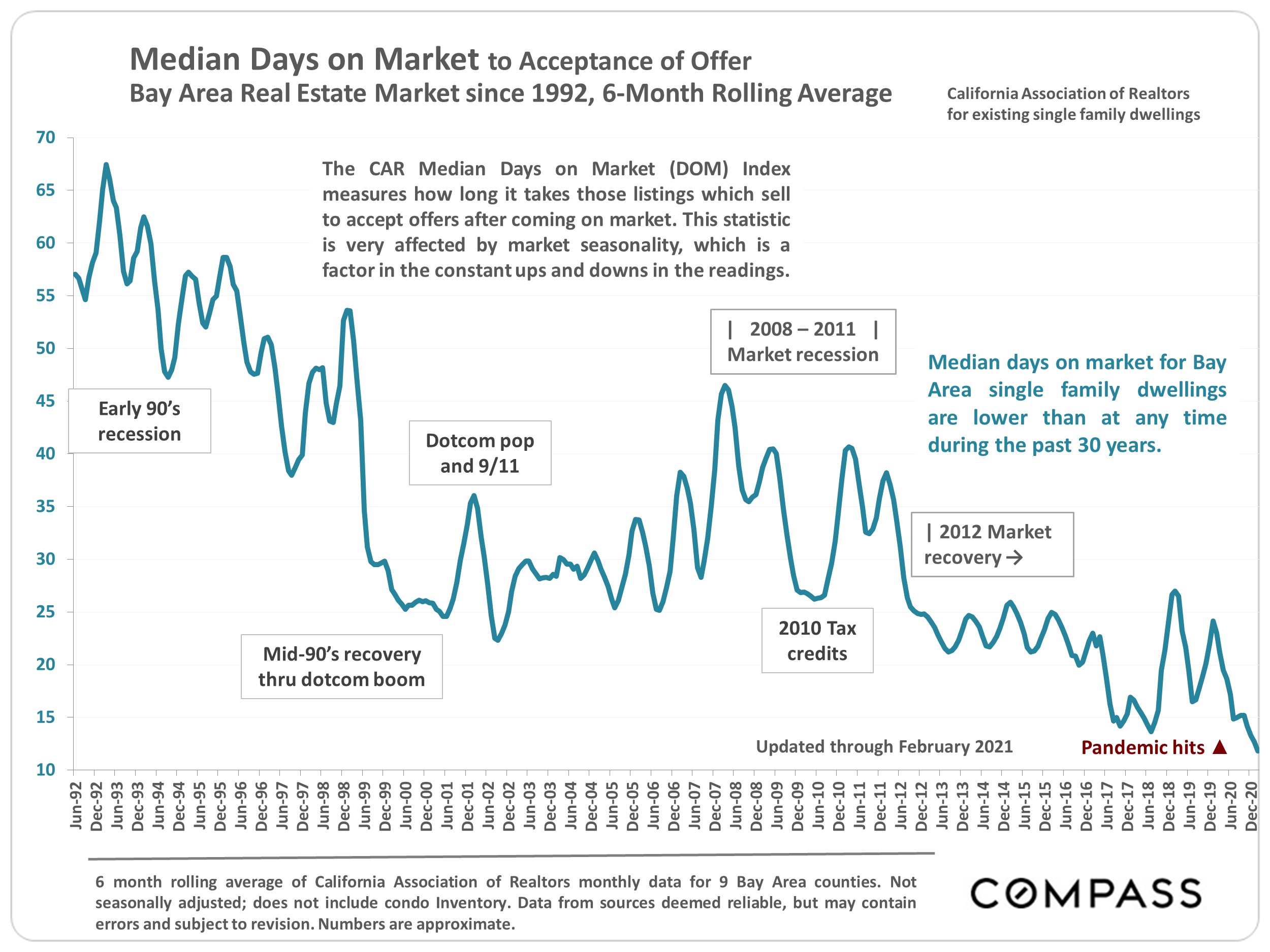

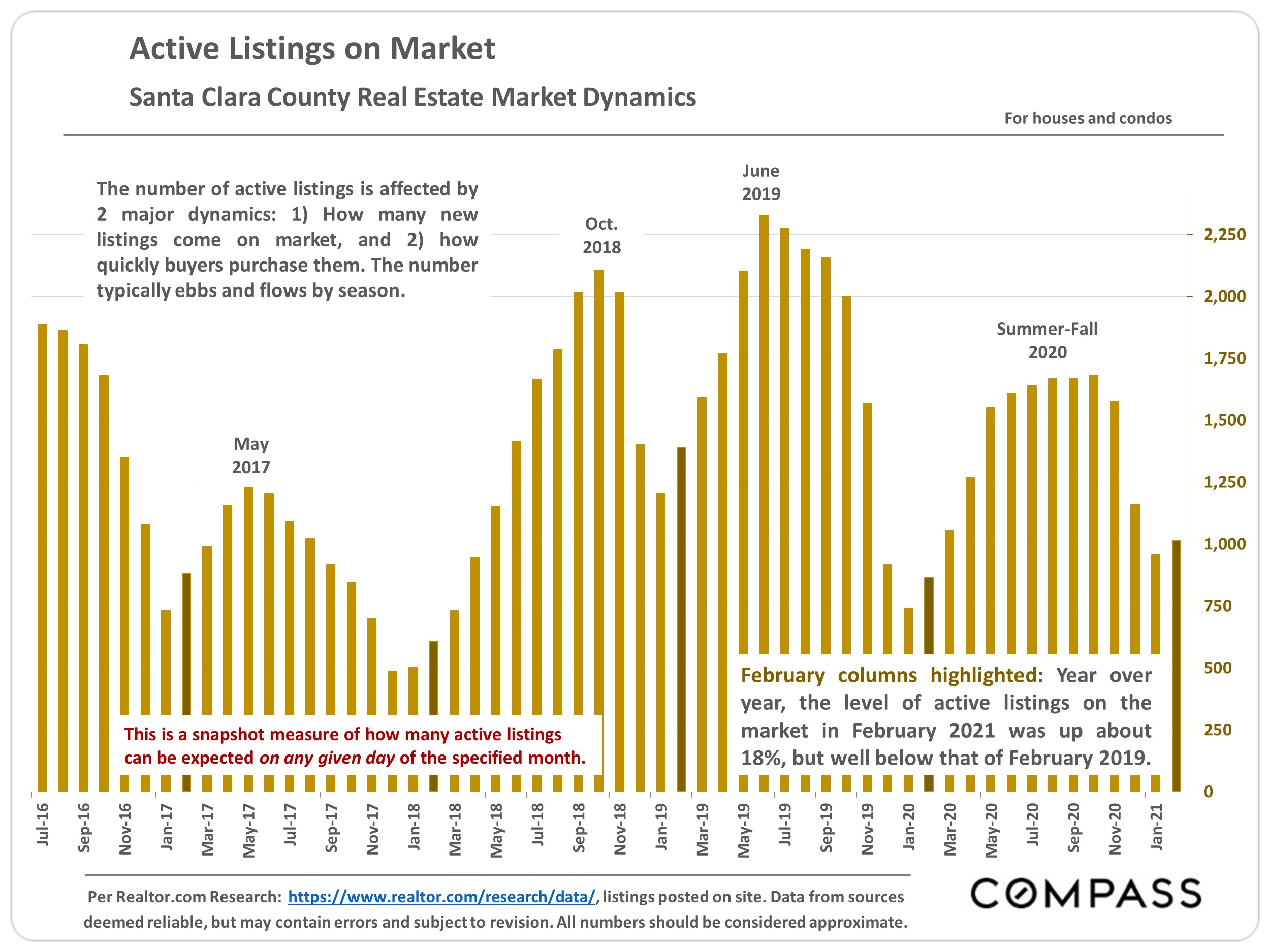

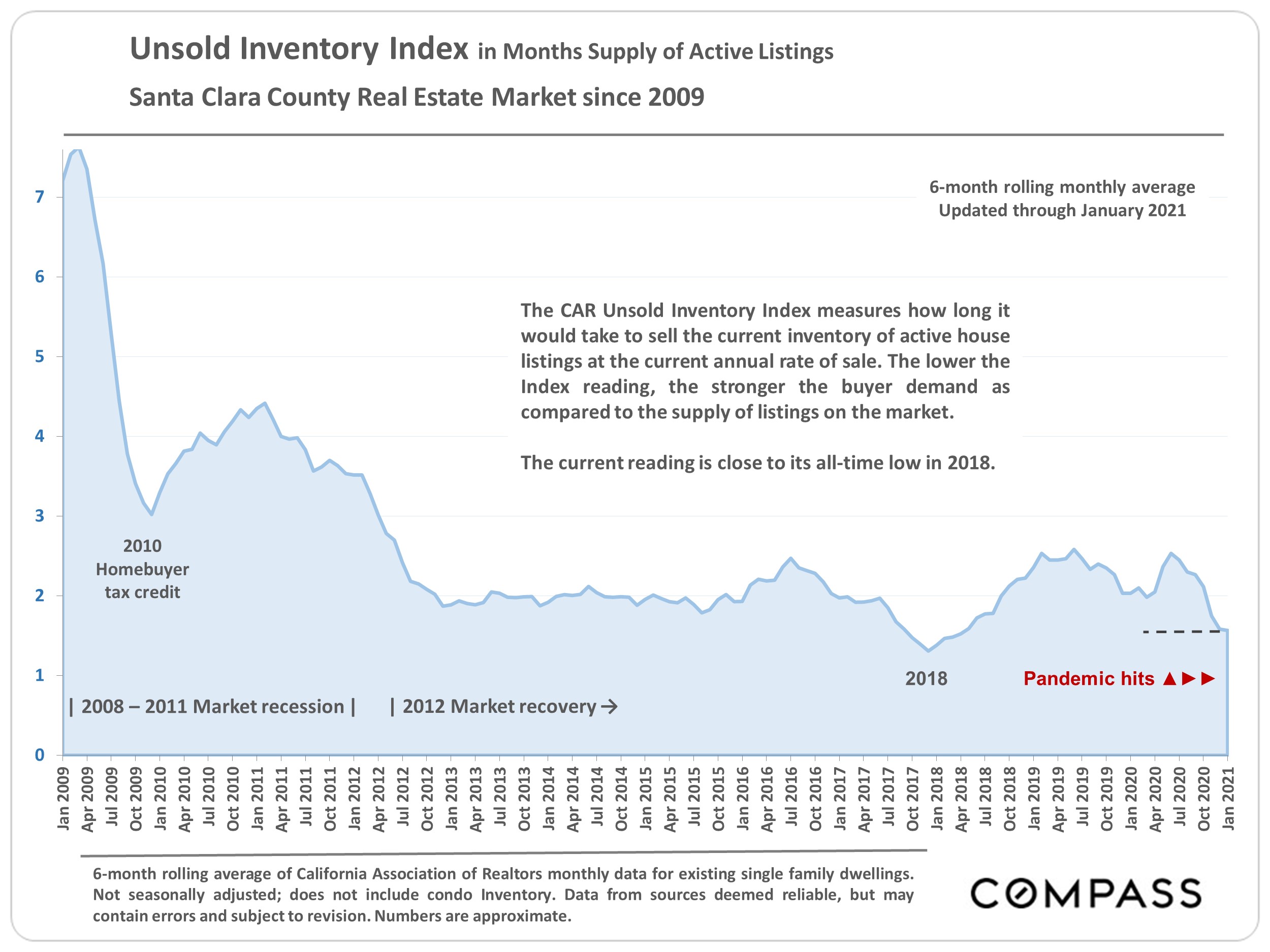

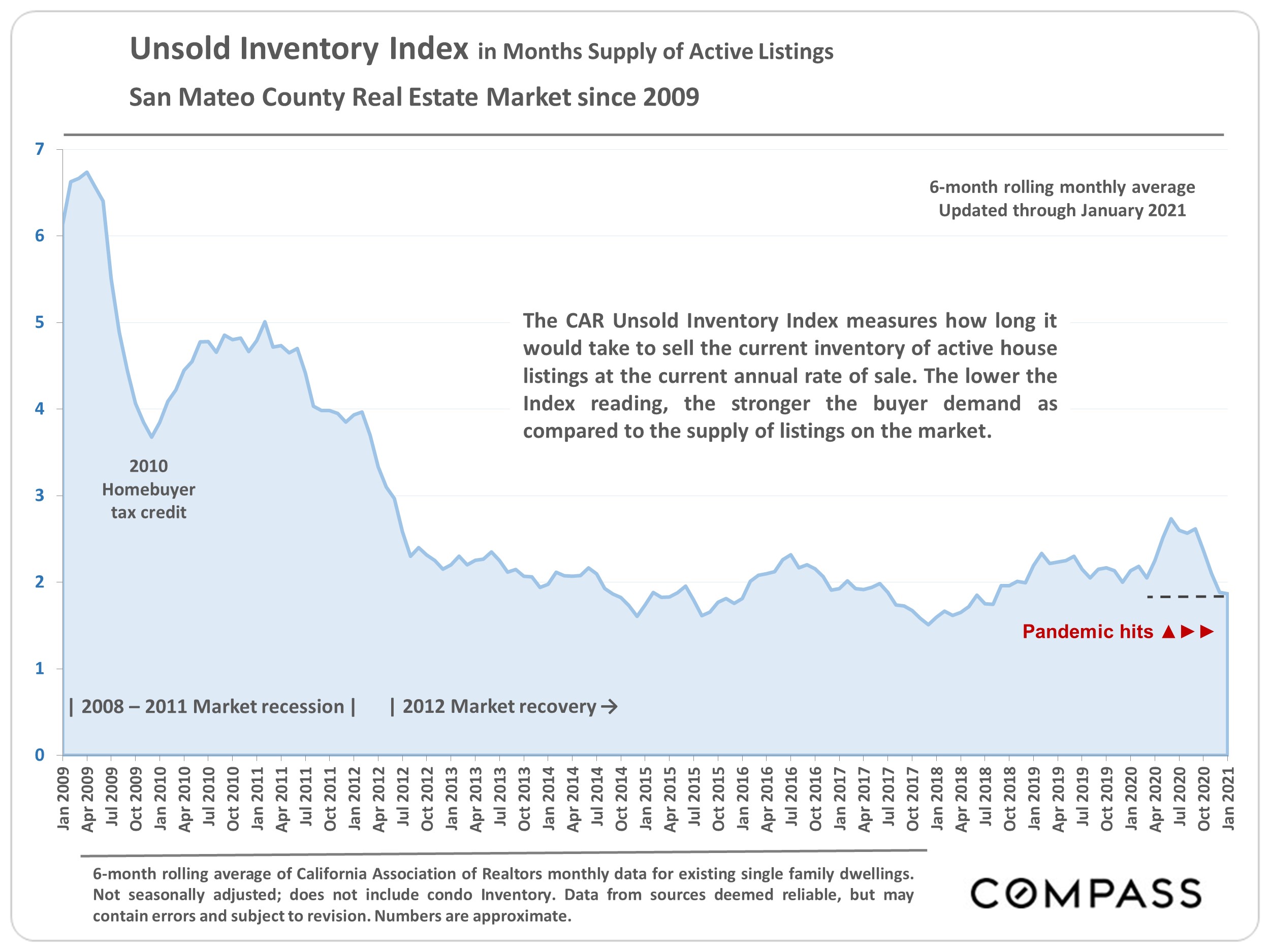

The months-supply-of-inventory level for Bay Area single family dwellings is at its lowest point in at least 15 years.

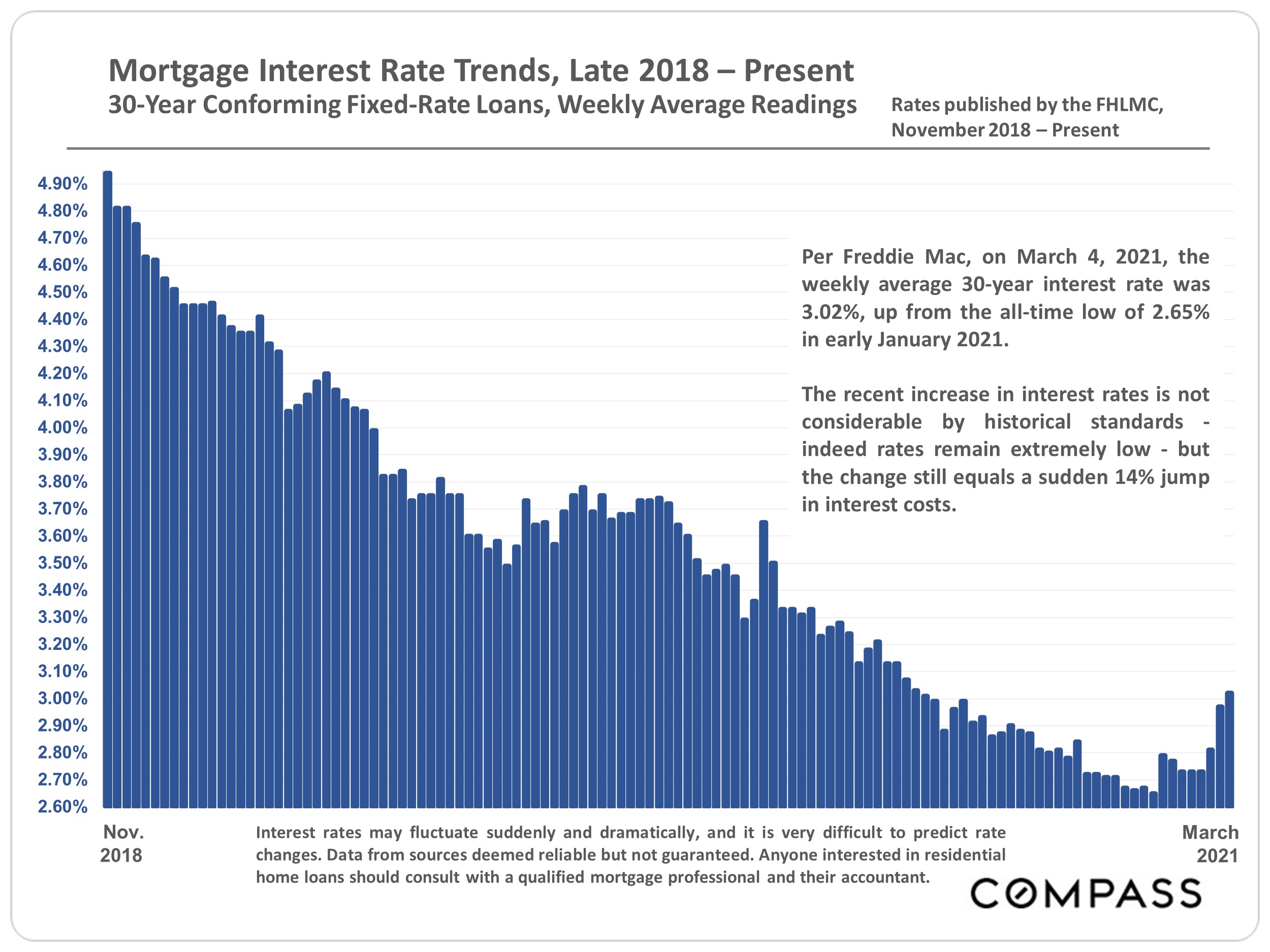

Median days-on-market for Bay Area single family dwellings are at their lowest in at least 30 years.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

The Spring Market Began in January & Continues to Accelerate

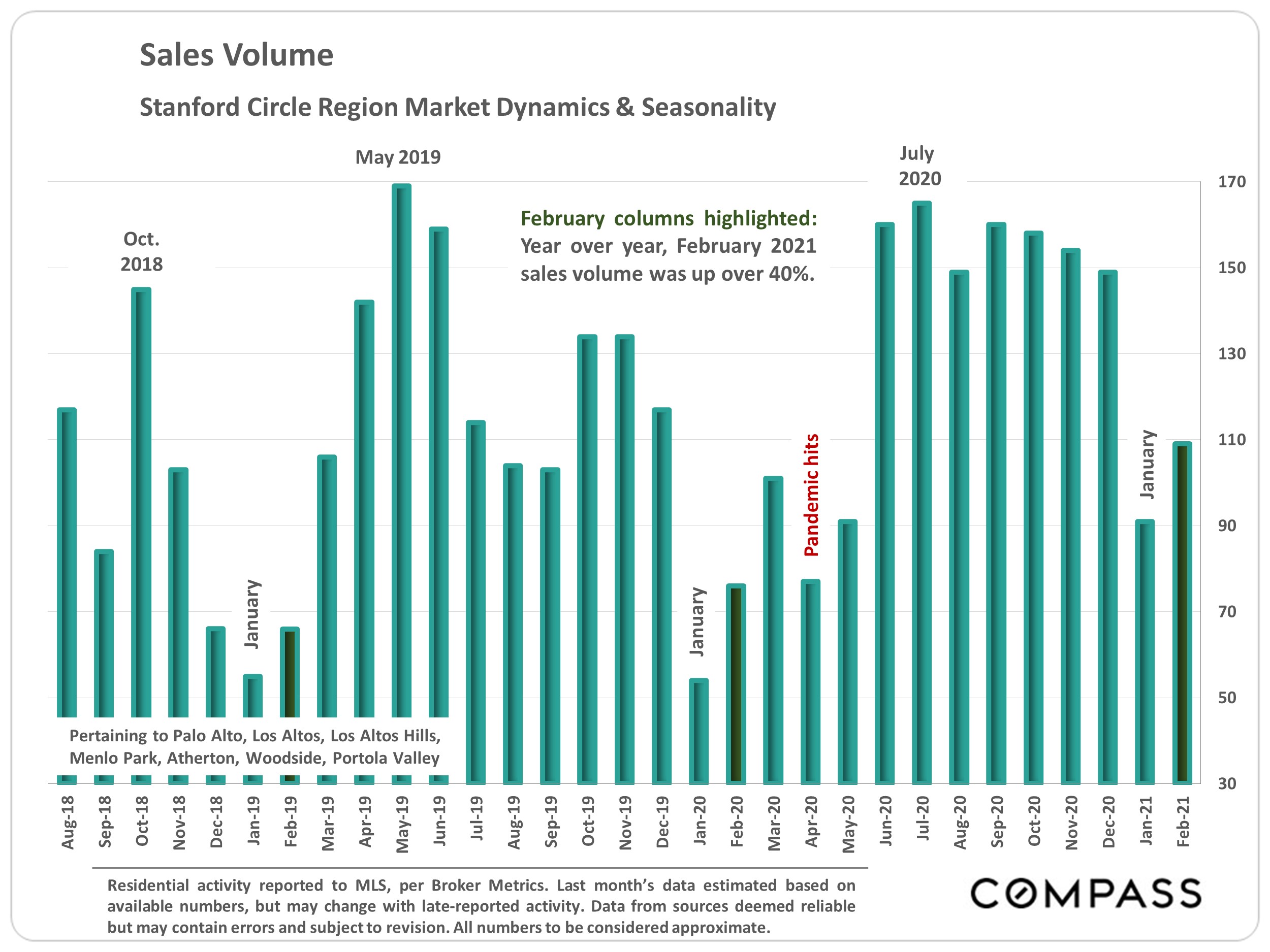

Sales Volume up 40%

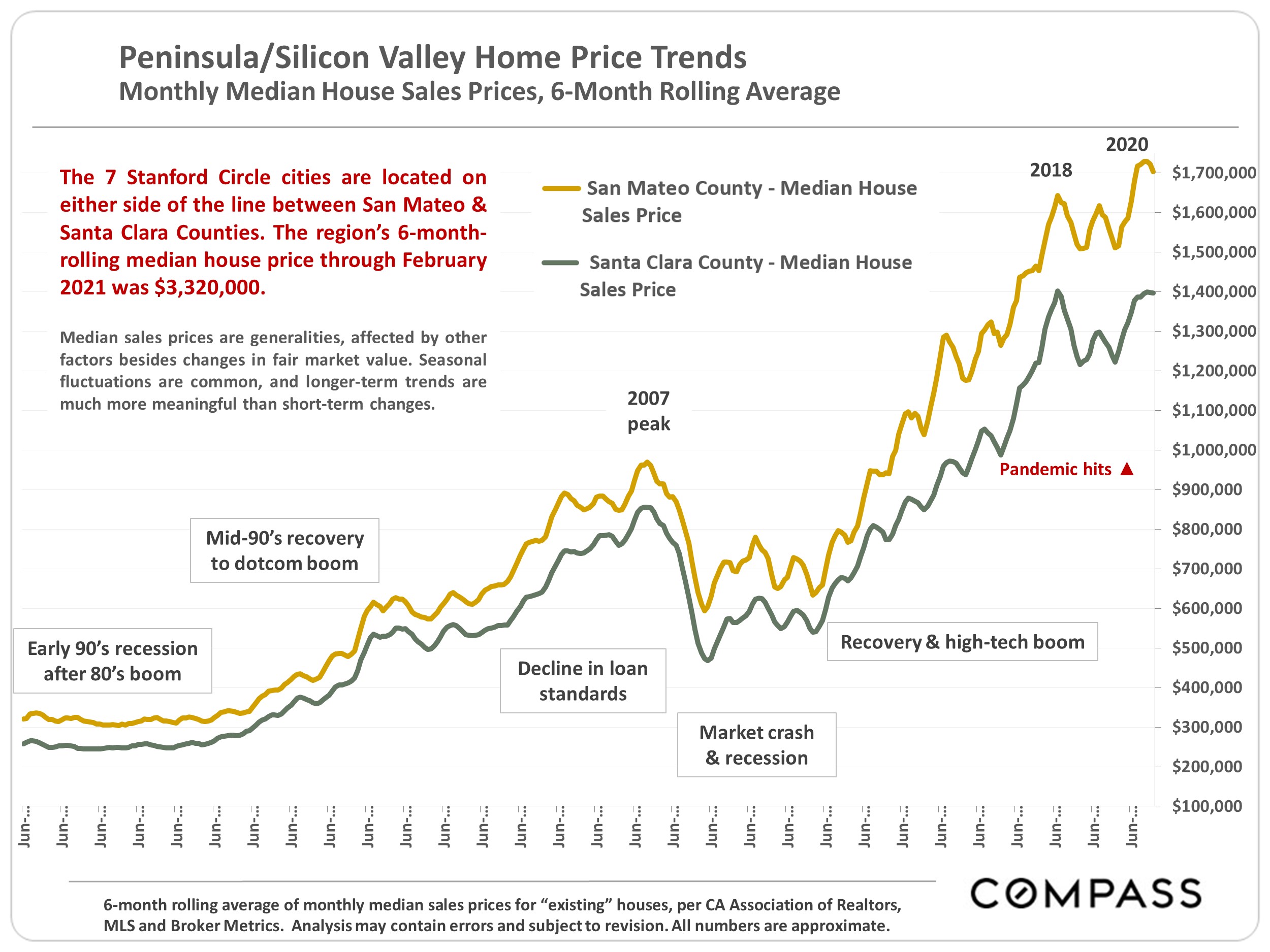

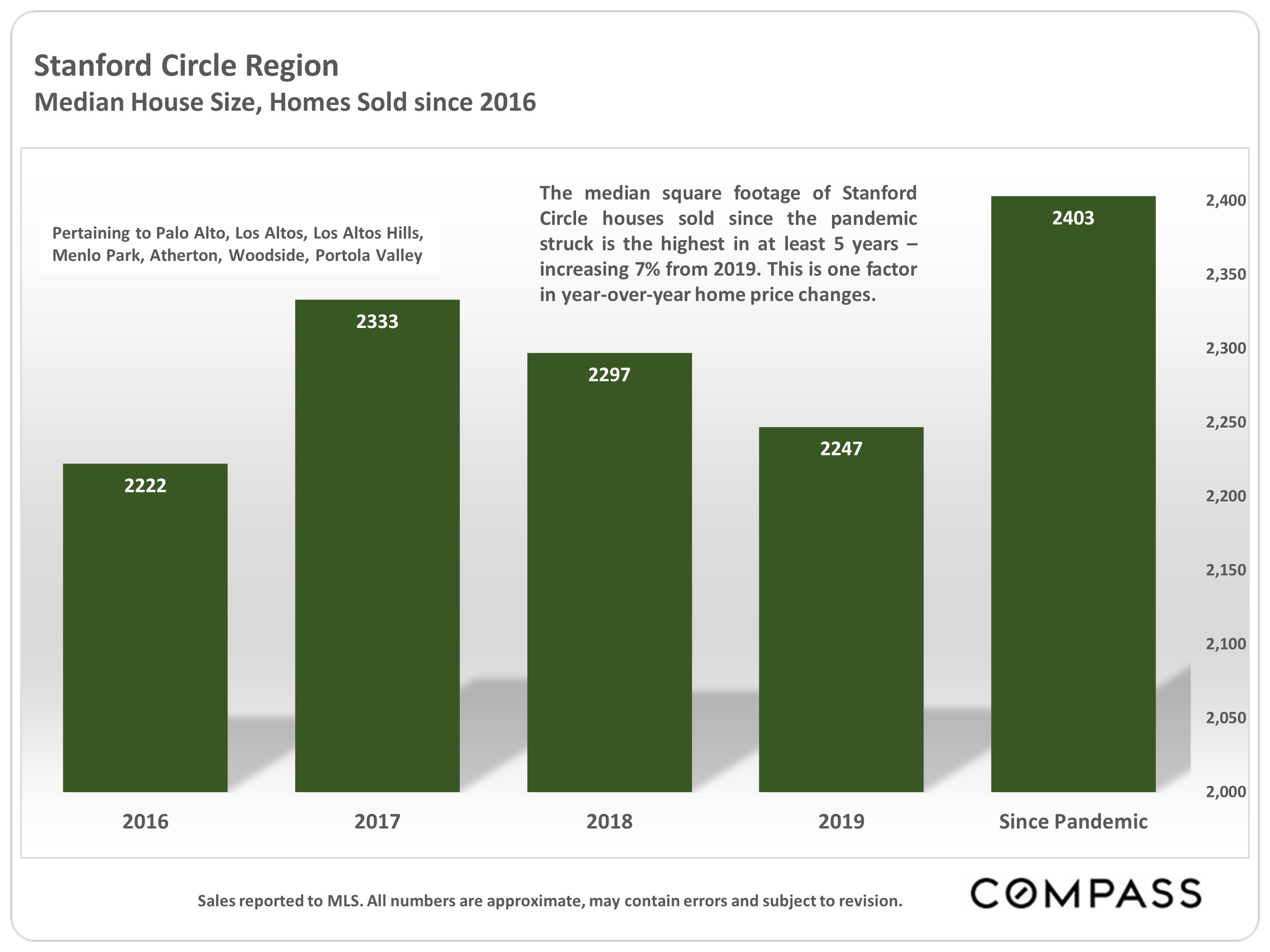

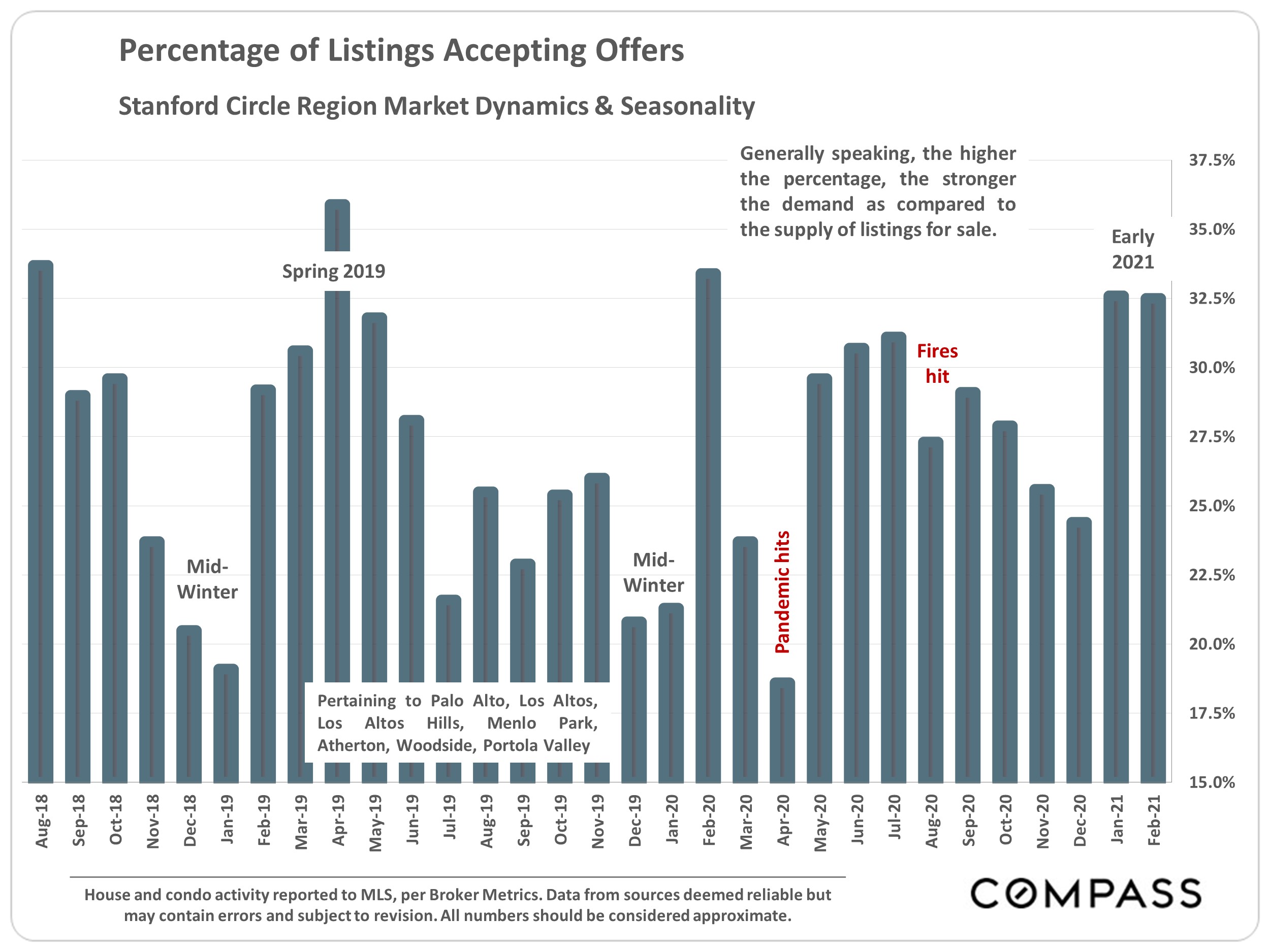

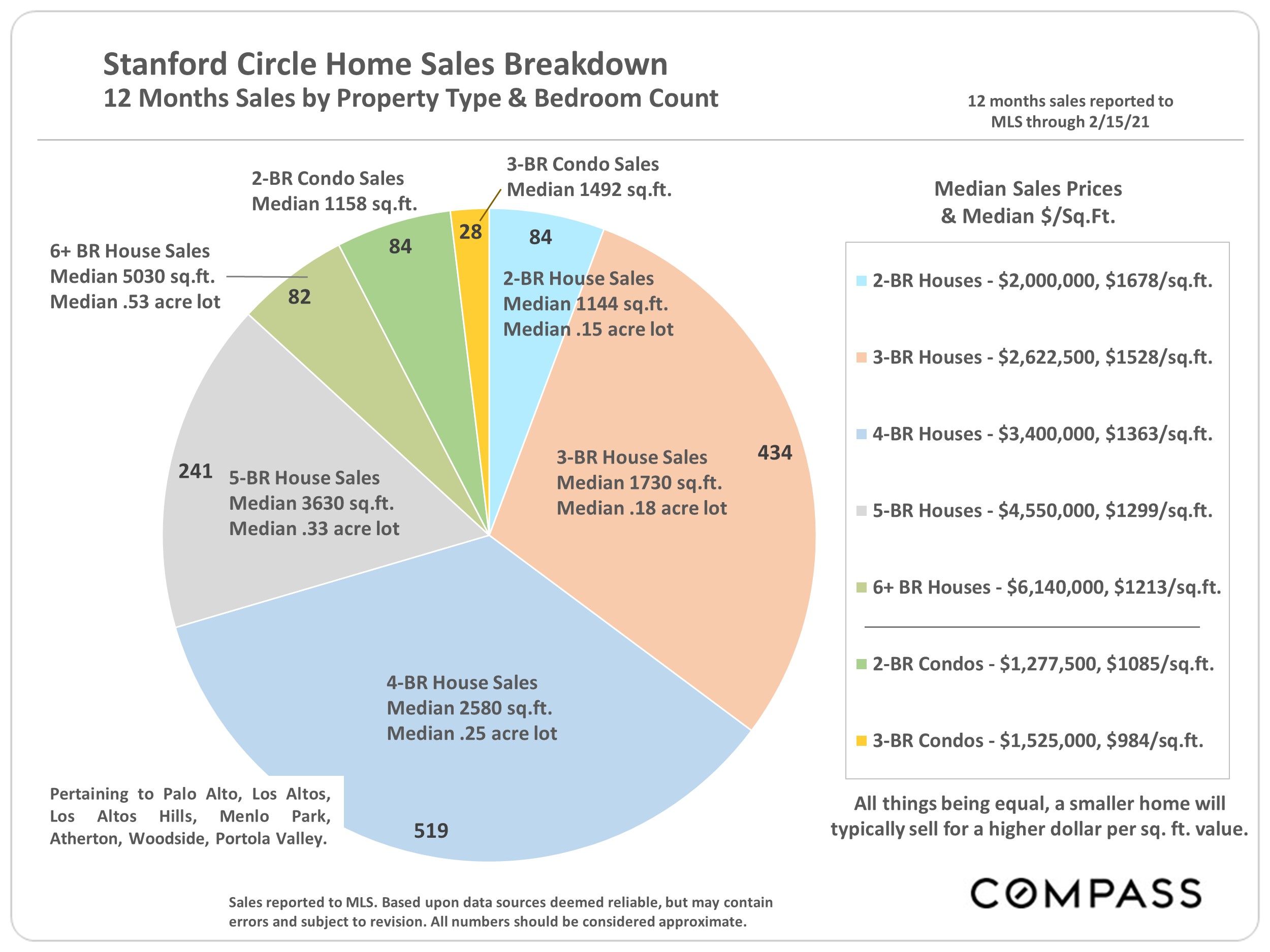

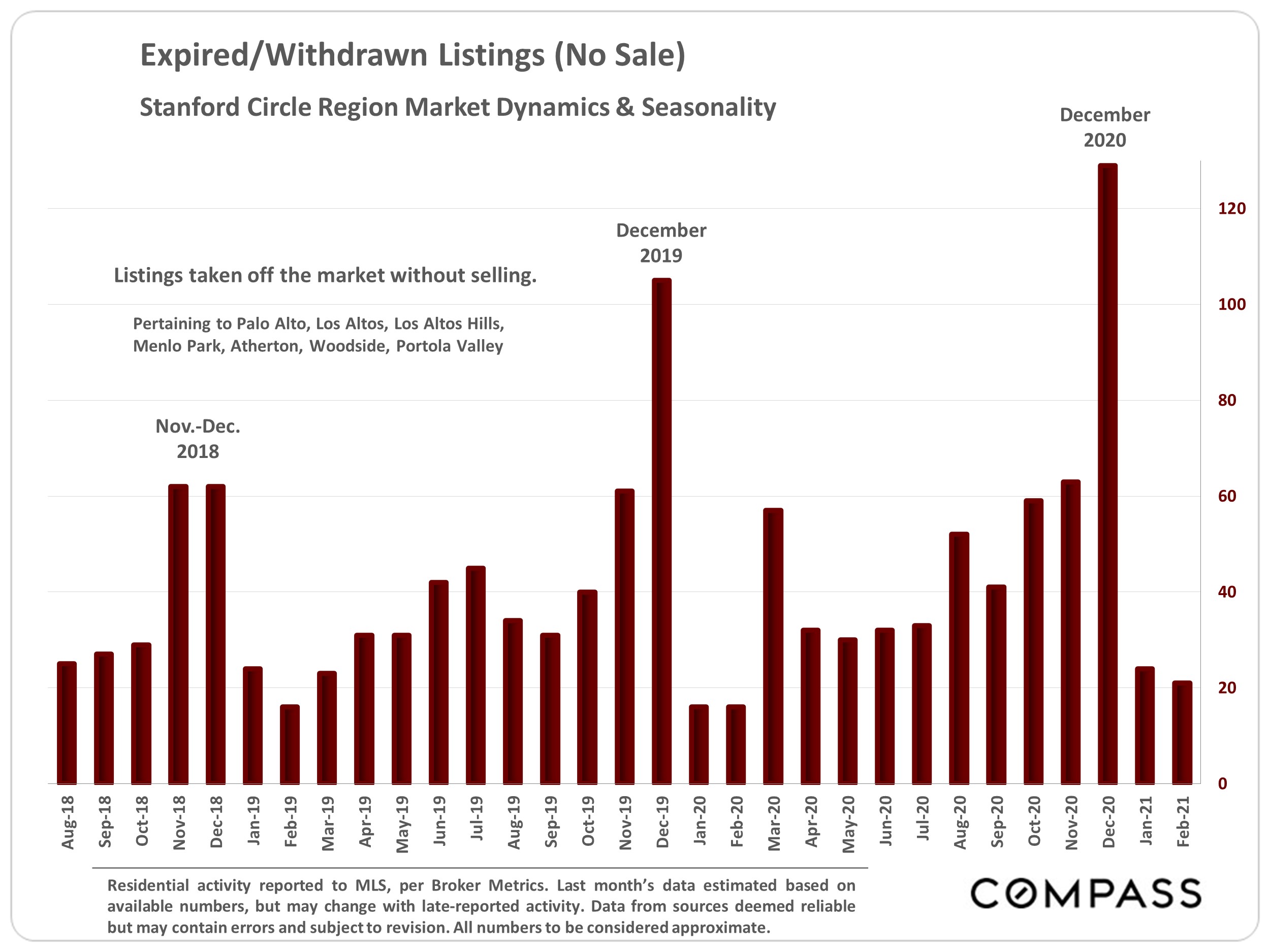

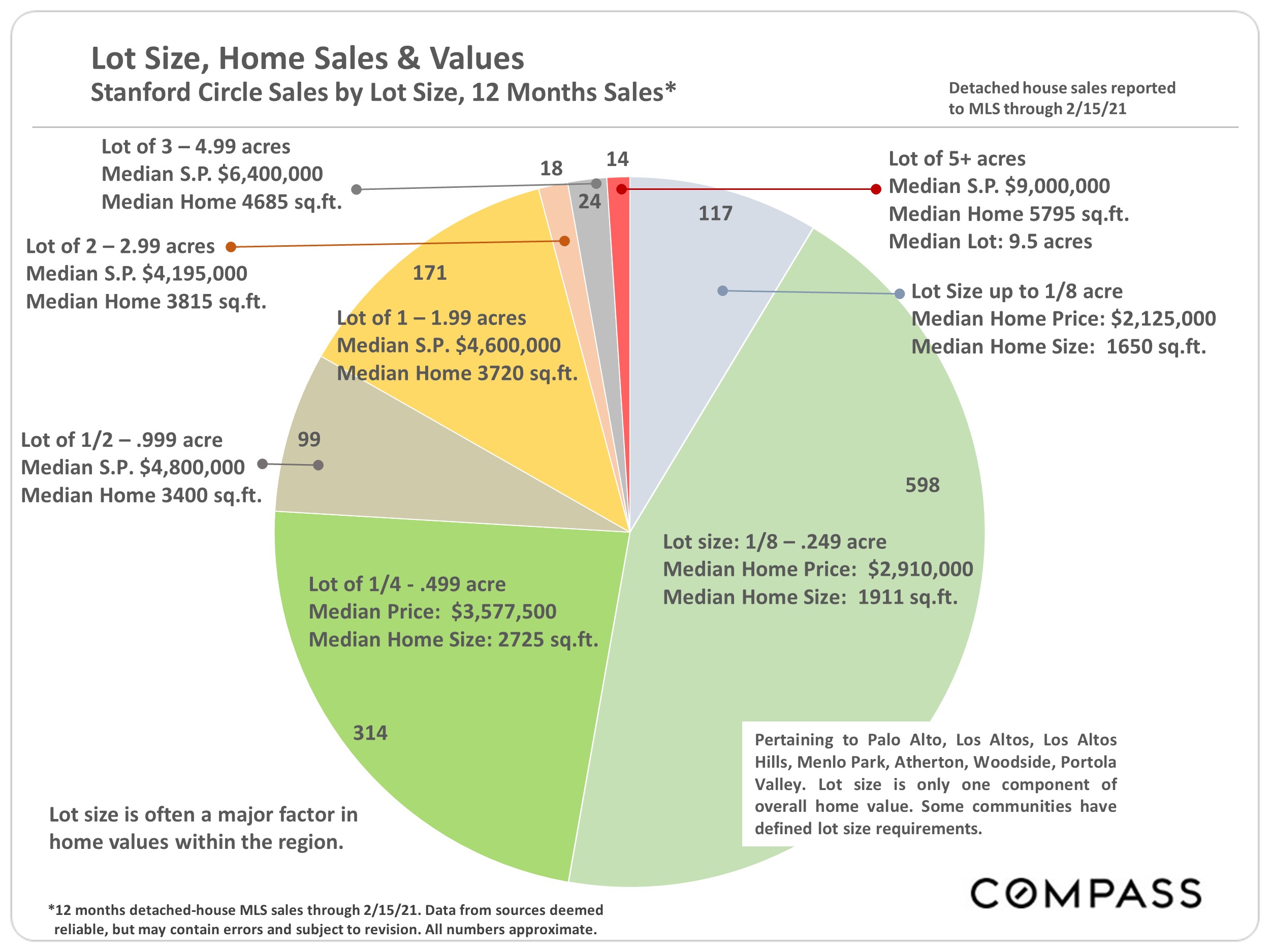

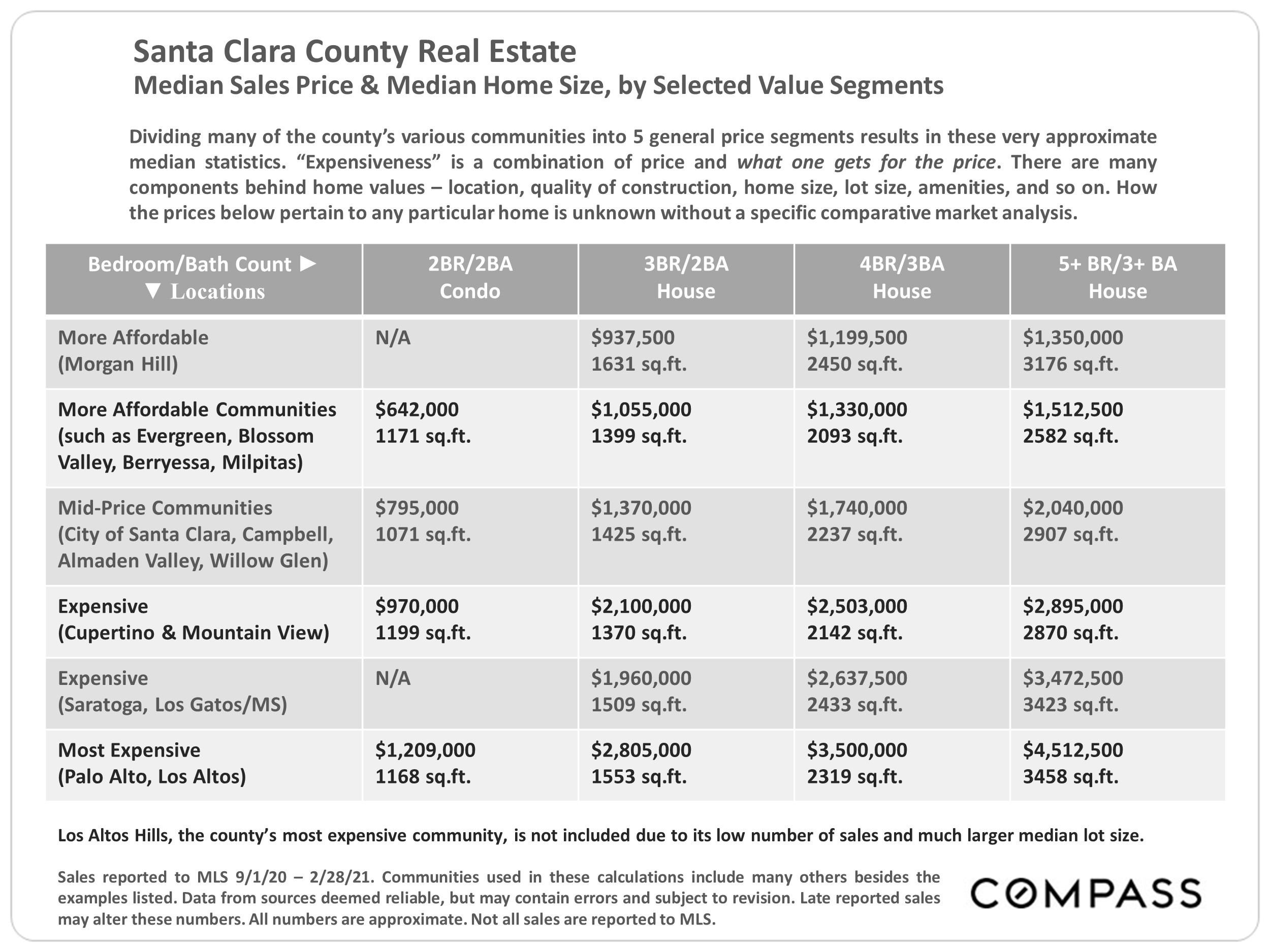

This report pertains to the communities of Palo Alto, Los Altos, Los Altos Hills, Menlo Park, Atherton, Woodside & Portola Valley – as a region, the most expensive market in the Bay Area.

At the beginning of the new year, it is unusual for buyers (demand) to jump back in much sooner than sellers (supply), a dynamic which commonly accelerates as spring get underway. When demand surges while listings lag behind, buyers must increasingly compete for appealing homes. This imbalance in supply and demand adds considerable pressure to the market.

This report will look at home list and sales prices, supply and demand from a variety of angles, the increase in luxury home sales, the impact of lot size on values, and the recent jump in interest rates. The charts are meant to be self-explanatory, but your questions are always welcome.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

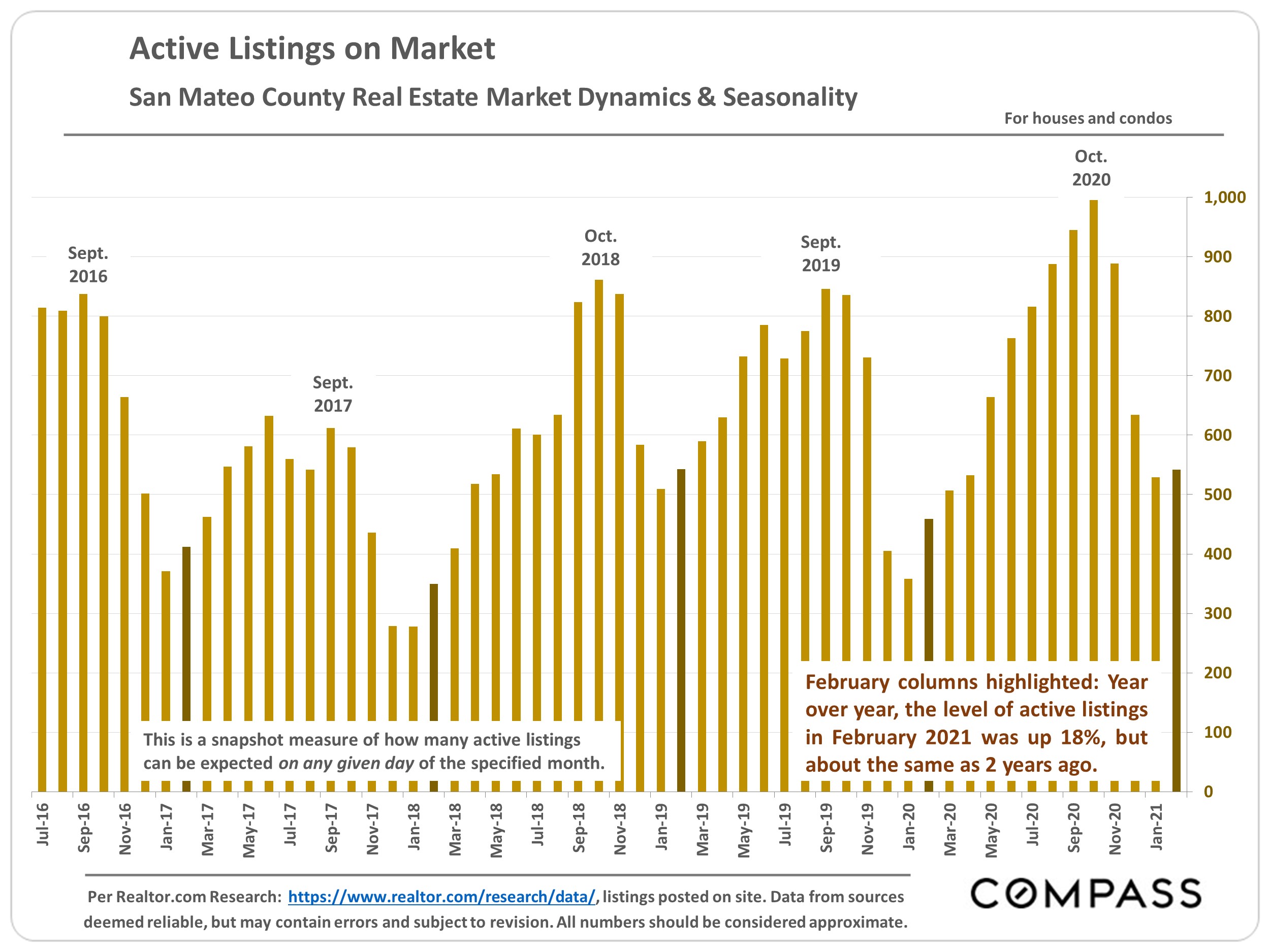

At the beginning of the new year, it is not unusual for buyers (demand) to jump back in much sooner than sellers (new listings – supply), a dynamic which commonly accelerates as spring gets underway. When demand surges while listings lag behind, buyers must increasingly compete, often heatedly, for appealing homes. This imbalance in supply and demand adds considerable pressure to the market, with overbidding and price increases becoming much more common. And this has occurred with a vengeance in early 2021, especially within the city’s house market.

This report will look at median house and condo list and sales prices, supply and demand from a variety of angles, the surge in luxury home sales, home prices along the Bay Area coast, and the recent jump in interest rates.

The charts are meant to be self-explanatory, but your questions are always welcome.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

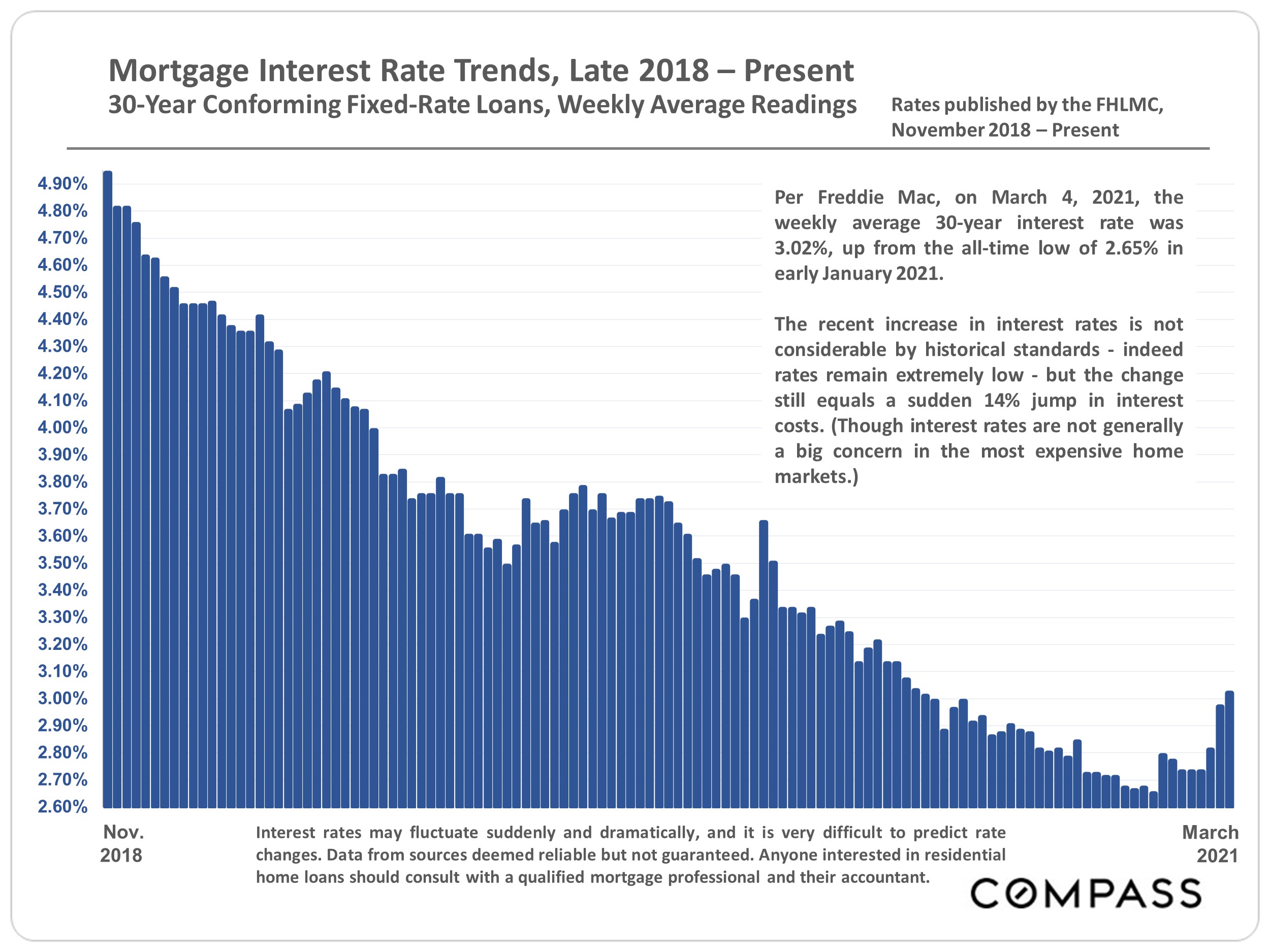

At the beginning of the new year, it is not unusual of buyers (demand) to jump back in much sooner than sellers (supply), a dynamic which commonly accelerates as spring gets underway. When demand surges while listings lag behind, buyers much increasingly compete, often heatedly, for appealing homes. This imbalance in supply and demand adds considerable pressure to the market, with overbidding and price increases becoming the norm. This has occurred with a vengeance in early 2021.

This report will look at median home list and sales prices, supply and demand from a variety of angles, the large surge in luxury home sales, home prices along the Bay Area coast, and the recent jump in interest rates.

The charts are meant to be self-explanatory, but your questions are always welcome.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

At the beginning of the new year, it is not unusual for buyers (demand) to jump back in much sooner than sellers (supply), a dynamic which commonly accelerates as spring gets underway. When demand surges while listings lag behind, buyers must increasingly compete, often heatedly, appealing homes. This imbalance in supply and demand adds considerable pressure to the market, with overbidding and price increase becoming common.

This report will look at the median home list and sales prices, supply and demand from a variety of angles, the surge in luxury home sales, home prices along the Bay Area coastline, and the recent jump in interest rates.

The charts are meant to be self-explanatory, but your questions are always welcome.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

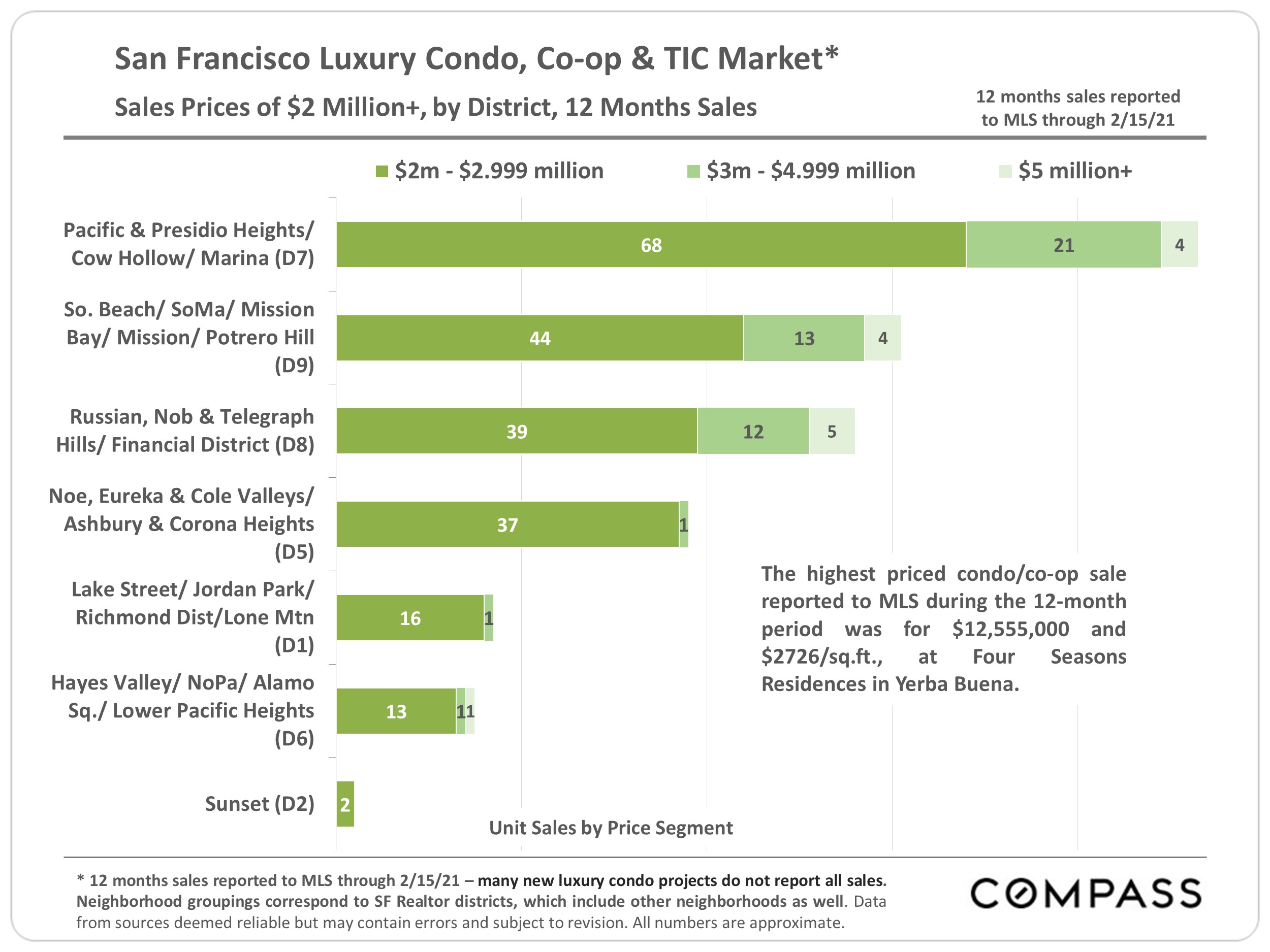

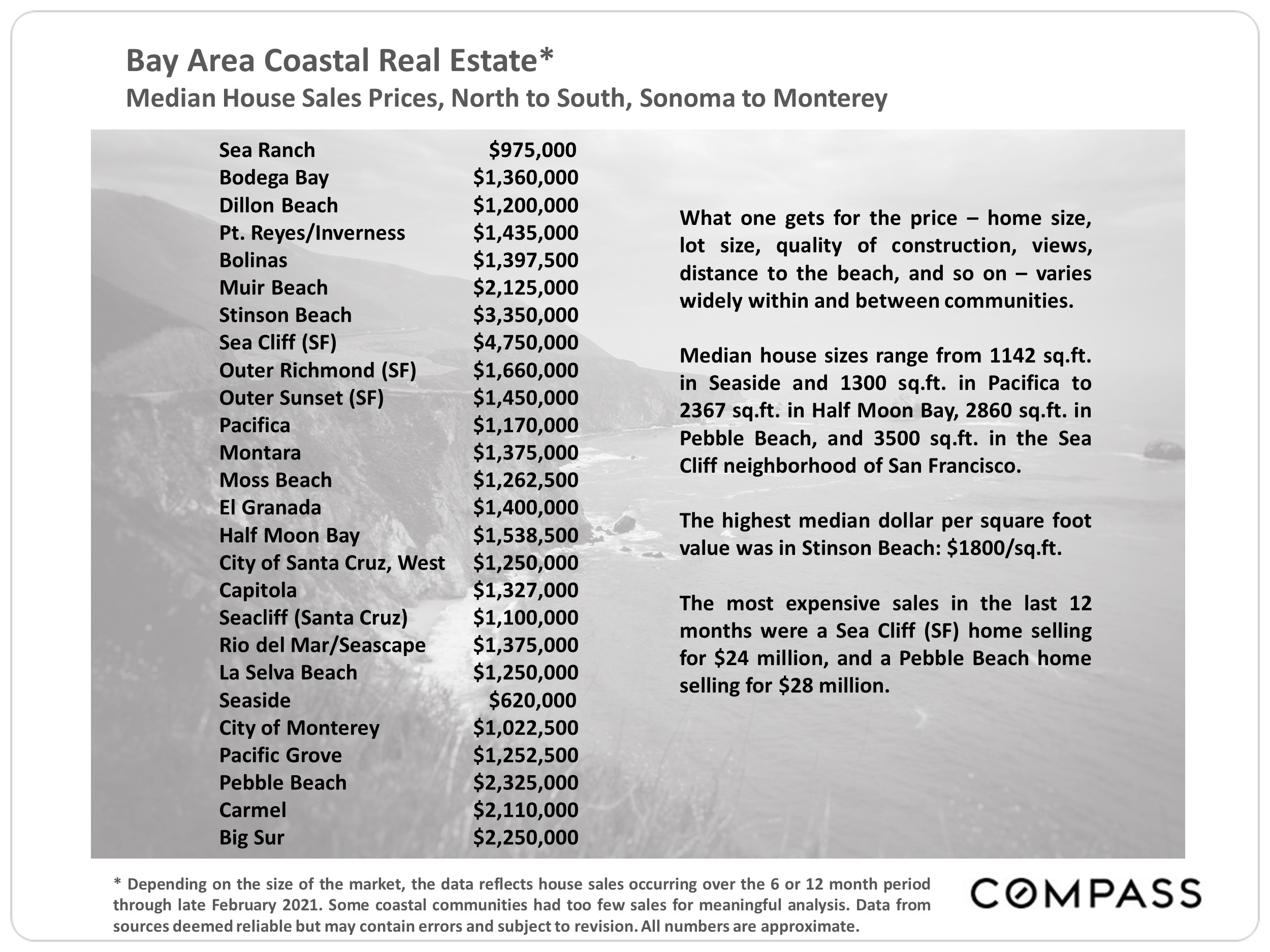

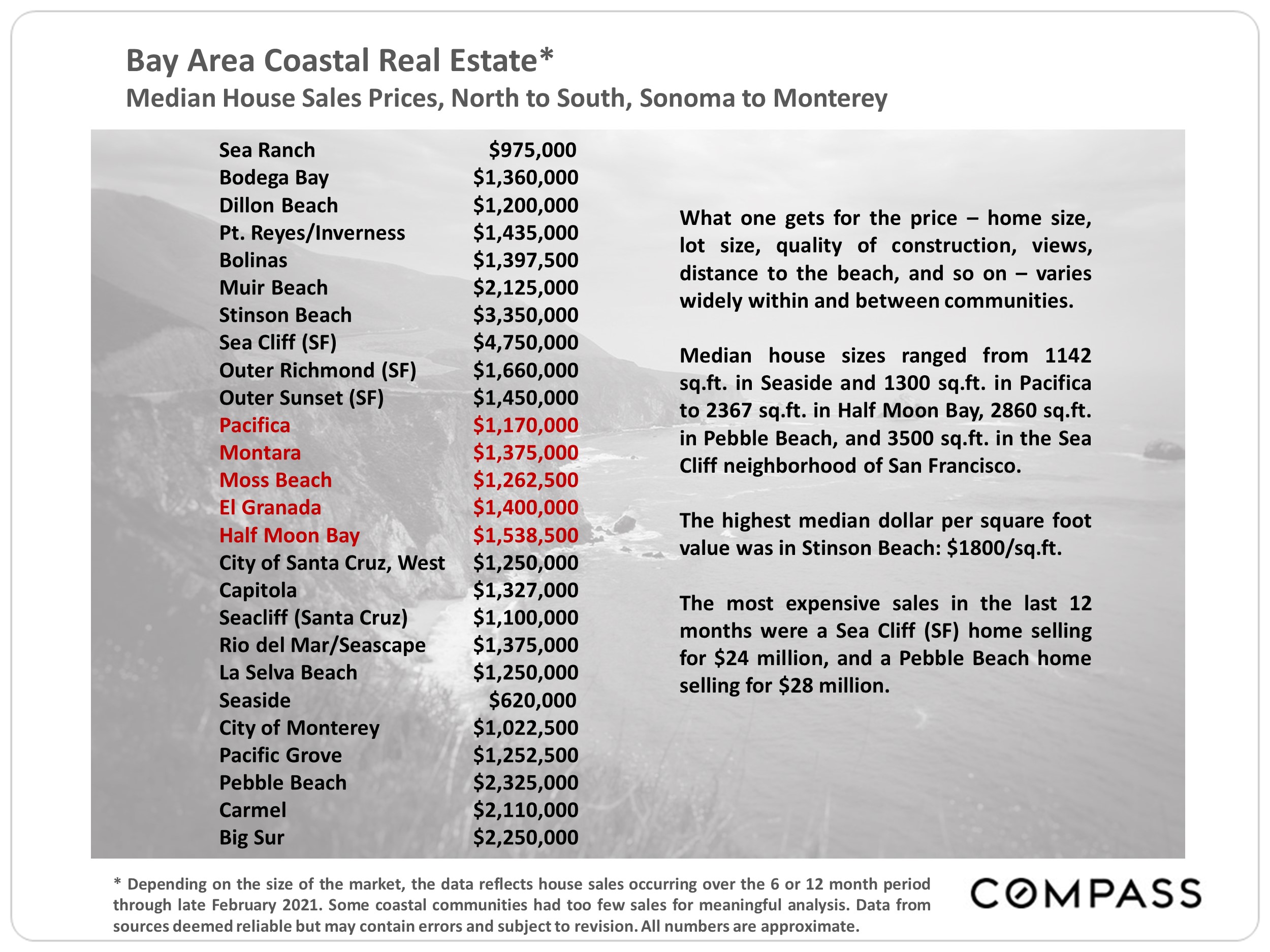

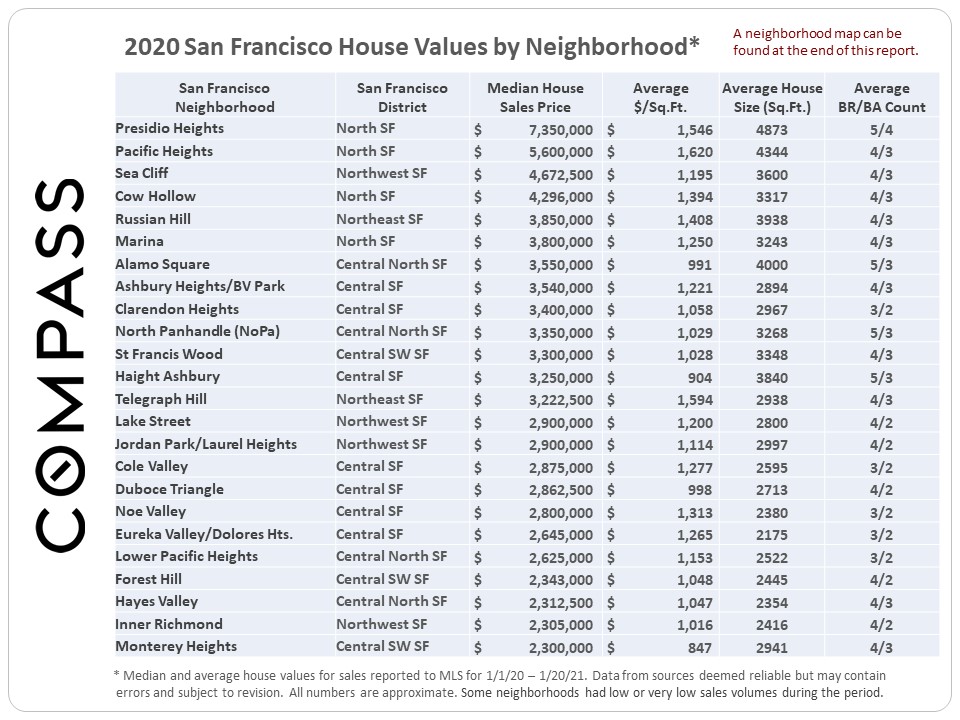

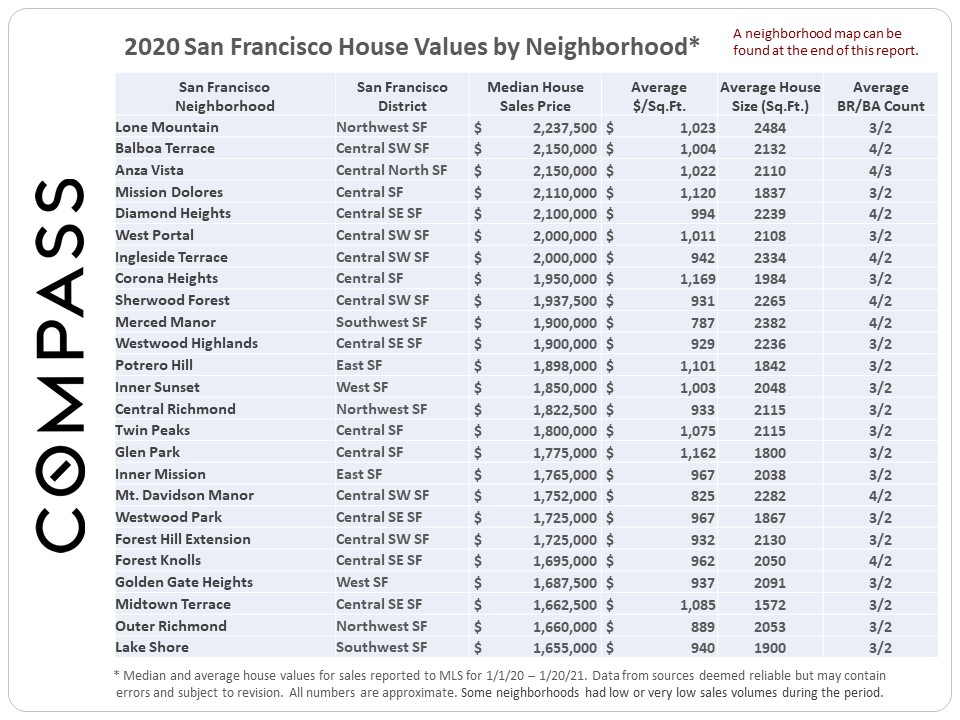

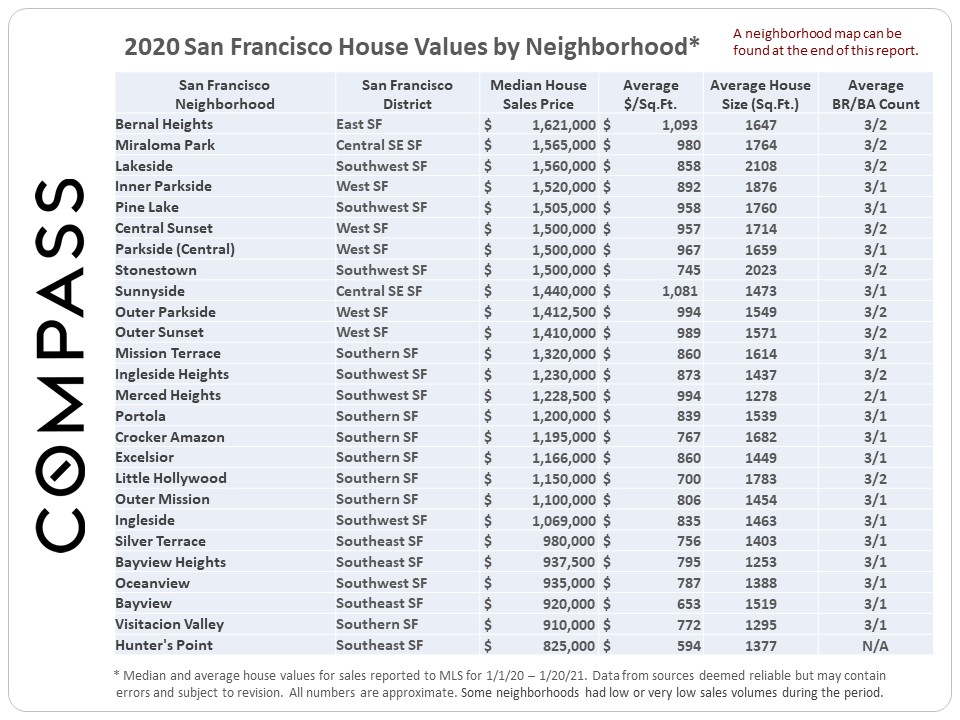

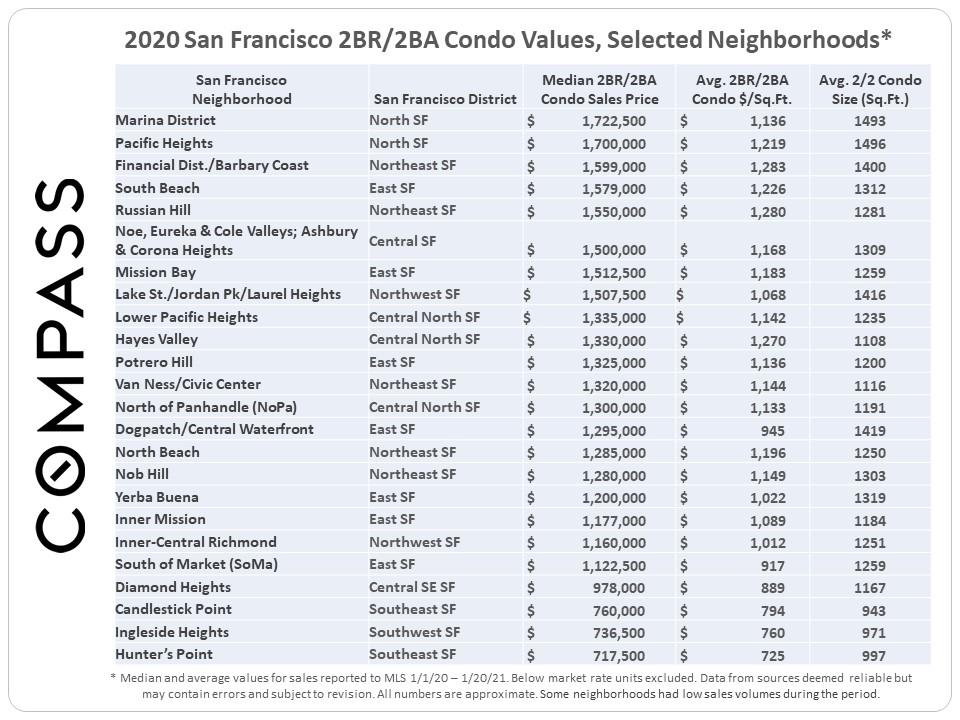

This map and the list following generally reflect 2020 median home sales prices and average dollar per square foot values in San Francisco neighborhoods. (Actually, it includes sales through 1/20/21.) Median sales prices are generalities that often fluctuate and can be affected by other factors besides changes in fair market value. They typically disguise a huge range of prices in the underlying individual sales, and all prices should be considered approximate. It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. Data per sales reported to MLS, deemed reliable, but may contain errors and subject to revision.

Median & Average Home Values*

By Neighborhood

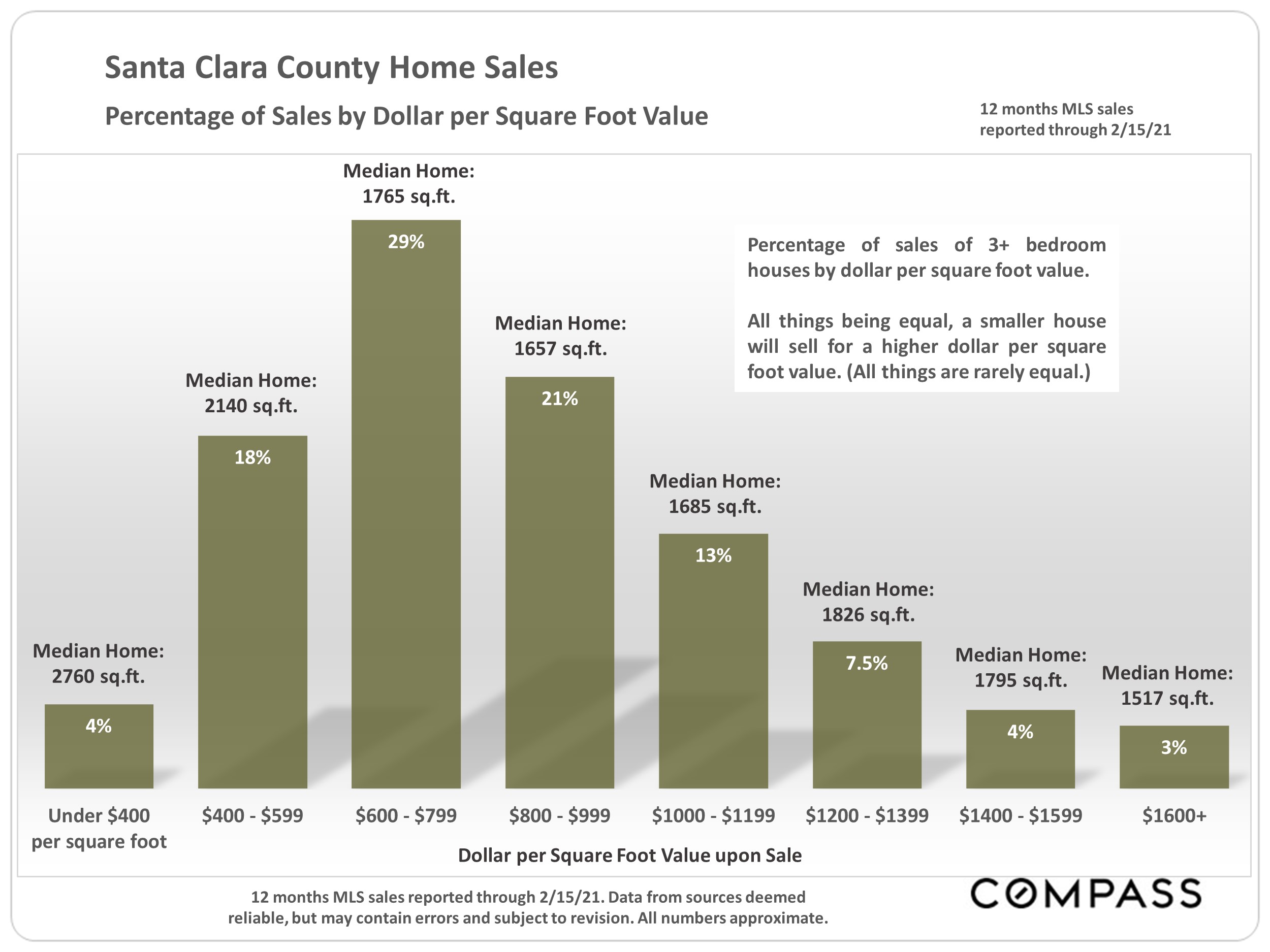

Many factors affect home values: quality of location within the market area, architectural style and curb appeal, square footage, condition, views, amenities, extra rooms, parking, decks and yards, privacy, lot size, floor and HOA services (for condos), and so on. There is often a wide or even vast variety of homes within market areas, especially larger areas. Statistics are generally broad generalities that typically “summarize” a wide variety of disparate data in the underlying individual transactions. Median and average values can be affected by a variety of factors unrelated to fair market value, and anomalous fluctuations are common, especially in smaller and/or very expensive markets over shorter time periods. Median sales prices may diverge from values calculated by average square footage and average price per square foot. Not all SF home sales report square footage.

Some of the neighborhoods delineated had low or very low sales volumes during the period, which can impact the reliability of the statistics, and make them more prone to anomalous fluctuation. How these statistics apply to any particular property is unknown without a specific comparative market analysis. Speak to your Compass agent for further insight and analysis. A San Francisco neighborhood map can be found following the tables in this report.

* Per sales reported to MLS, 1/1/20 – 1/20/21. Not all sales are reported to MLS. Neighborhoods, as defined by

the SF Association of Realtors, vary widely in the number of sales. Data from sources deemed reliable but may

contain errors and subject to revision. All numbers are approximate.

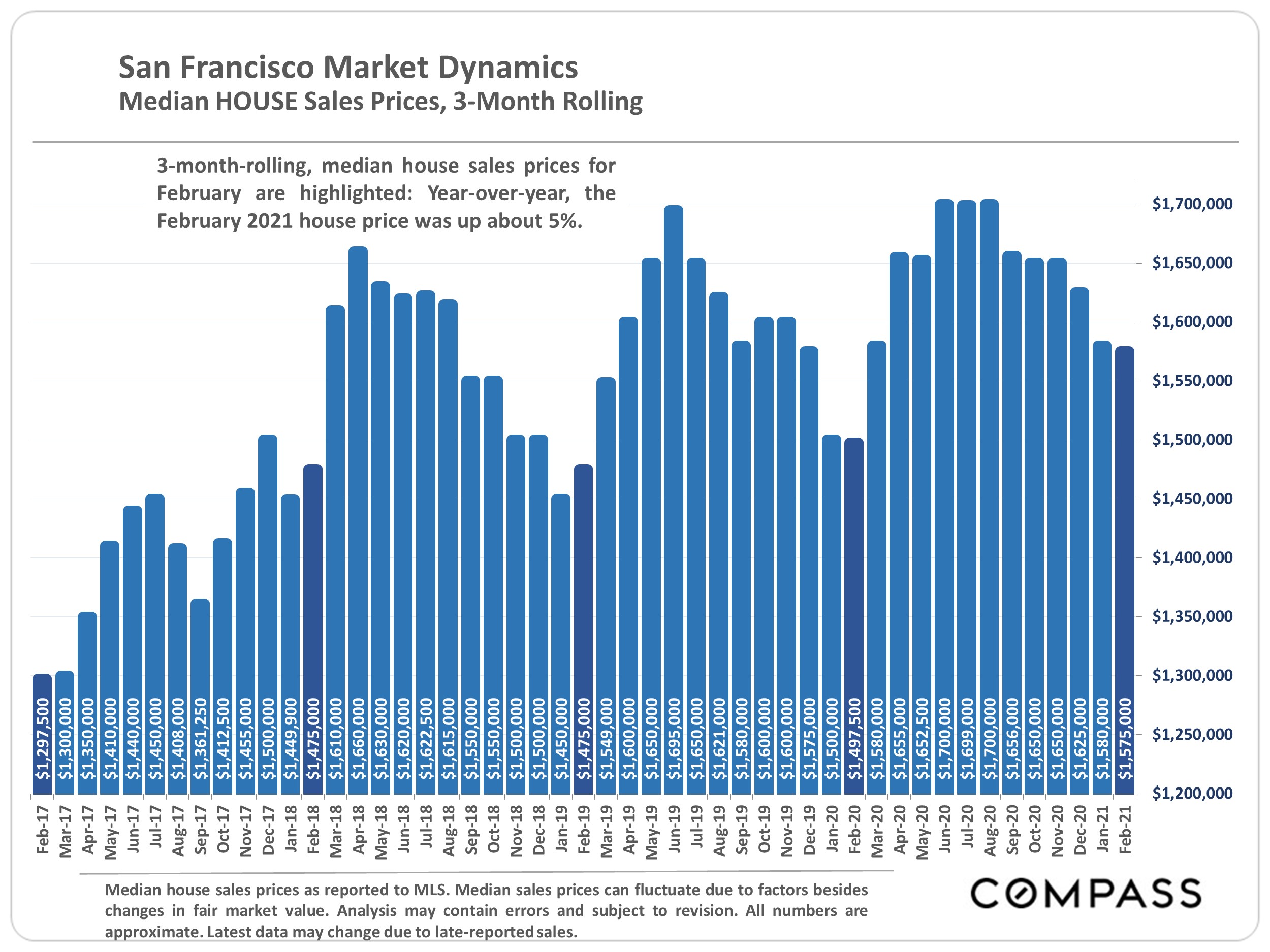

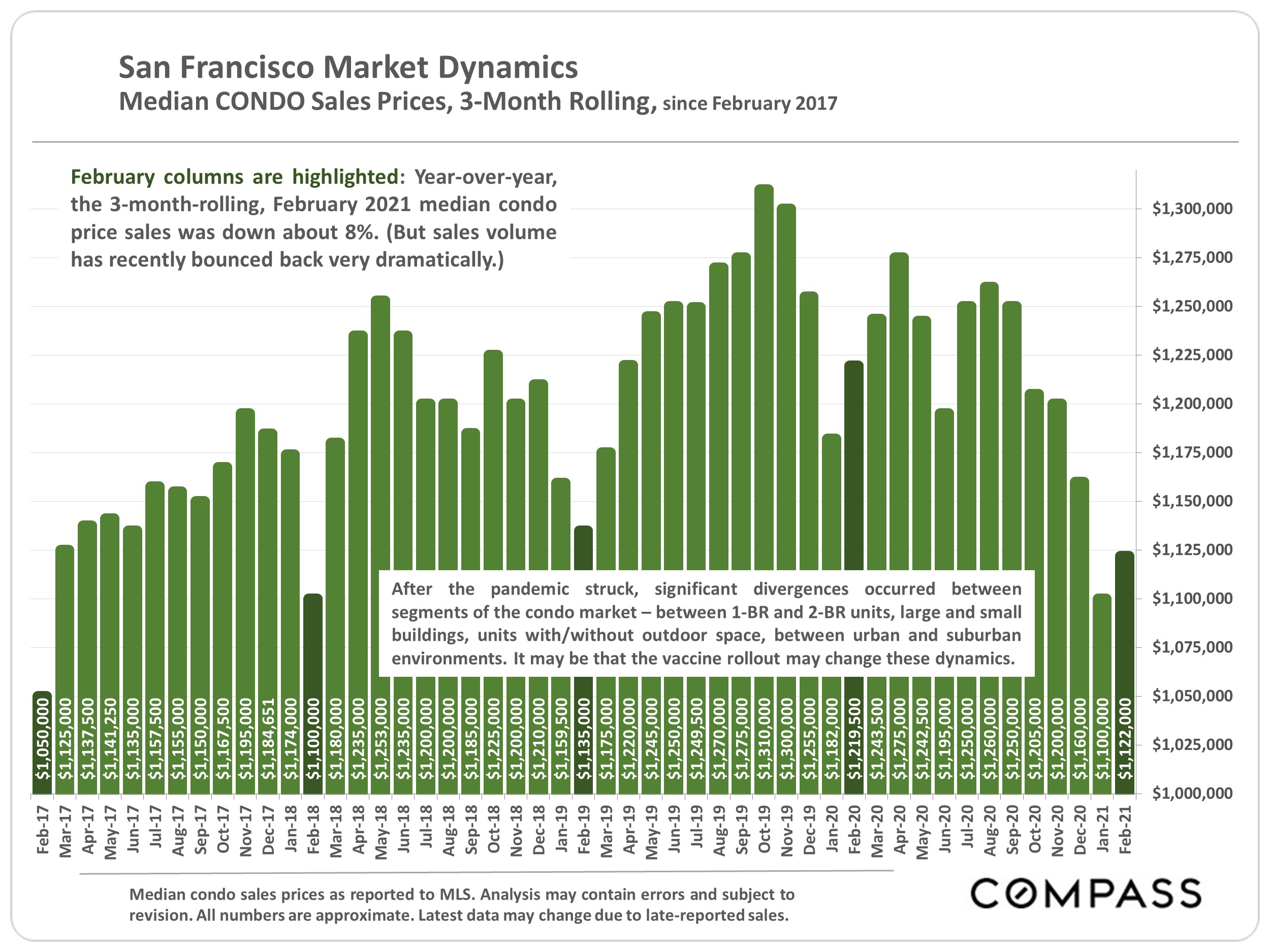

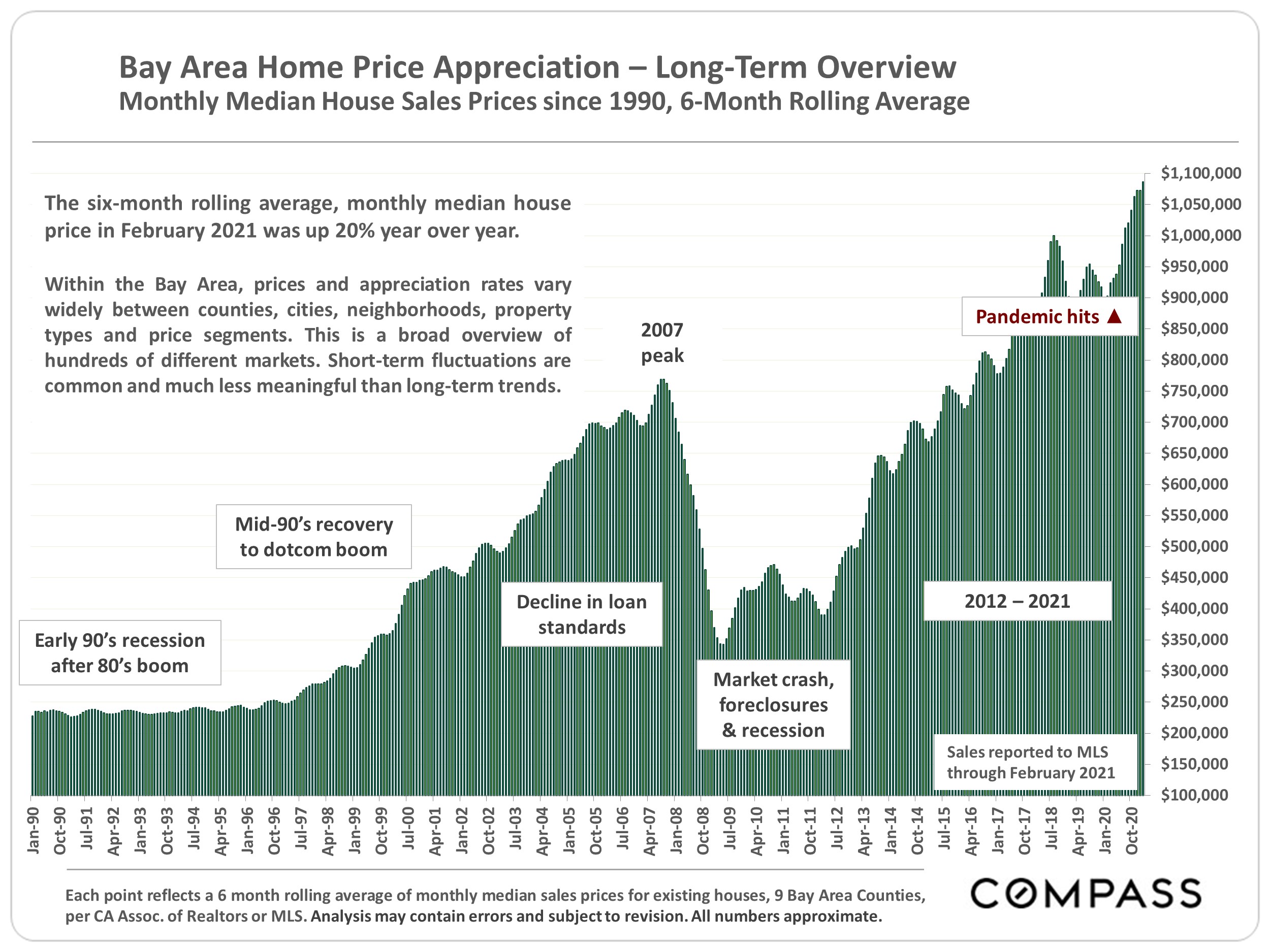

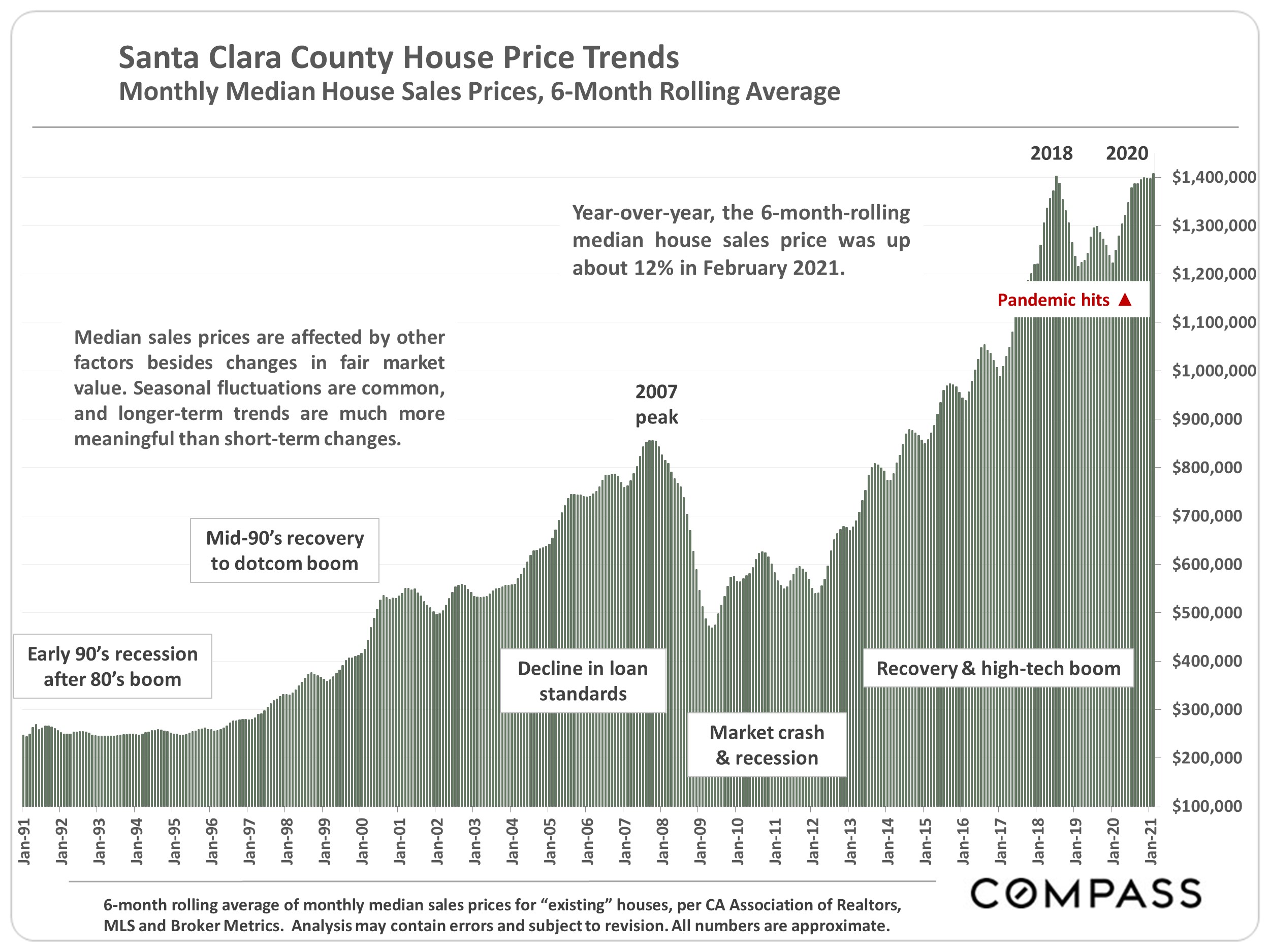

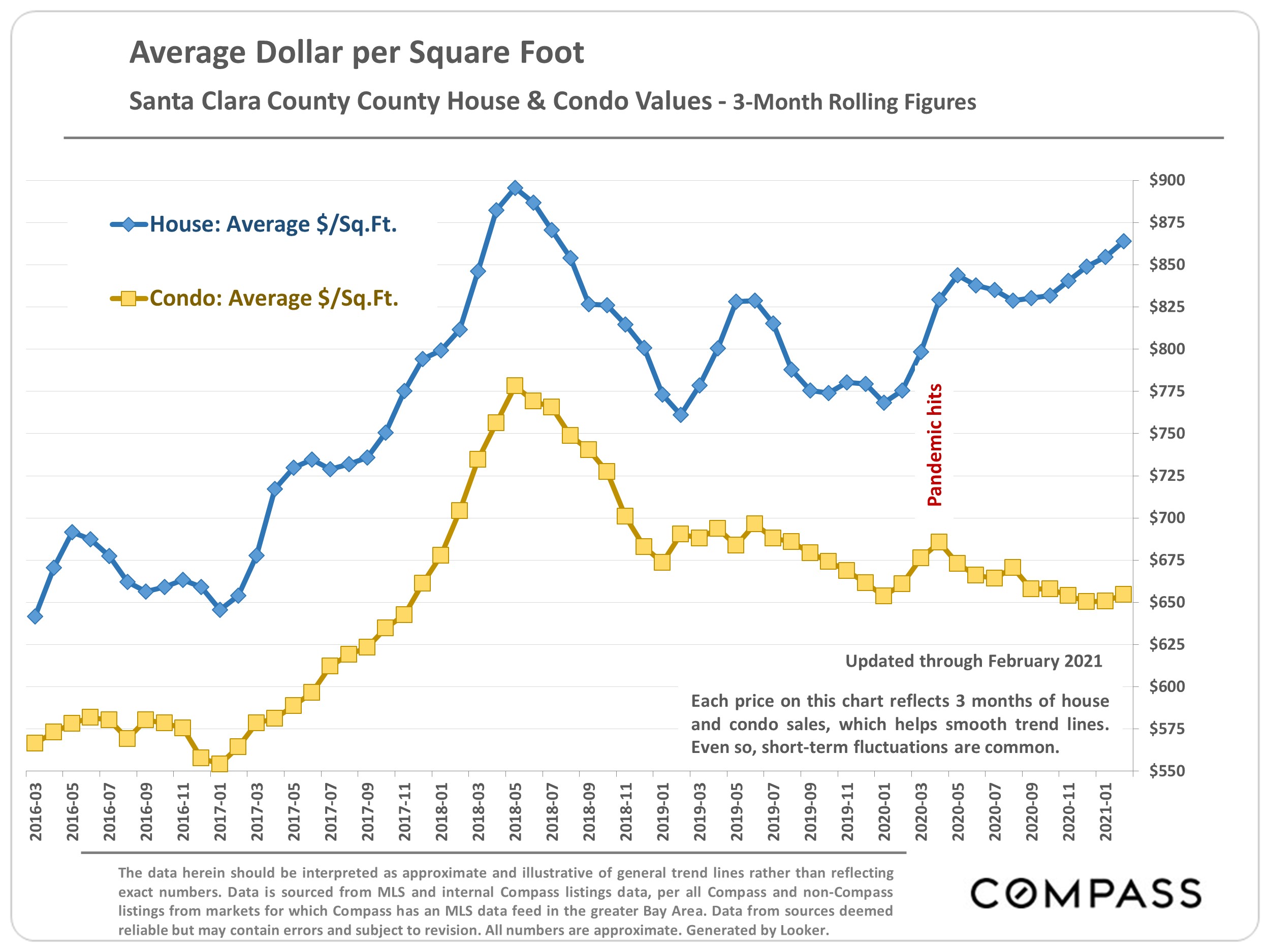

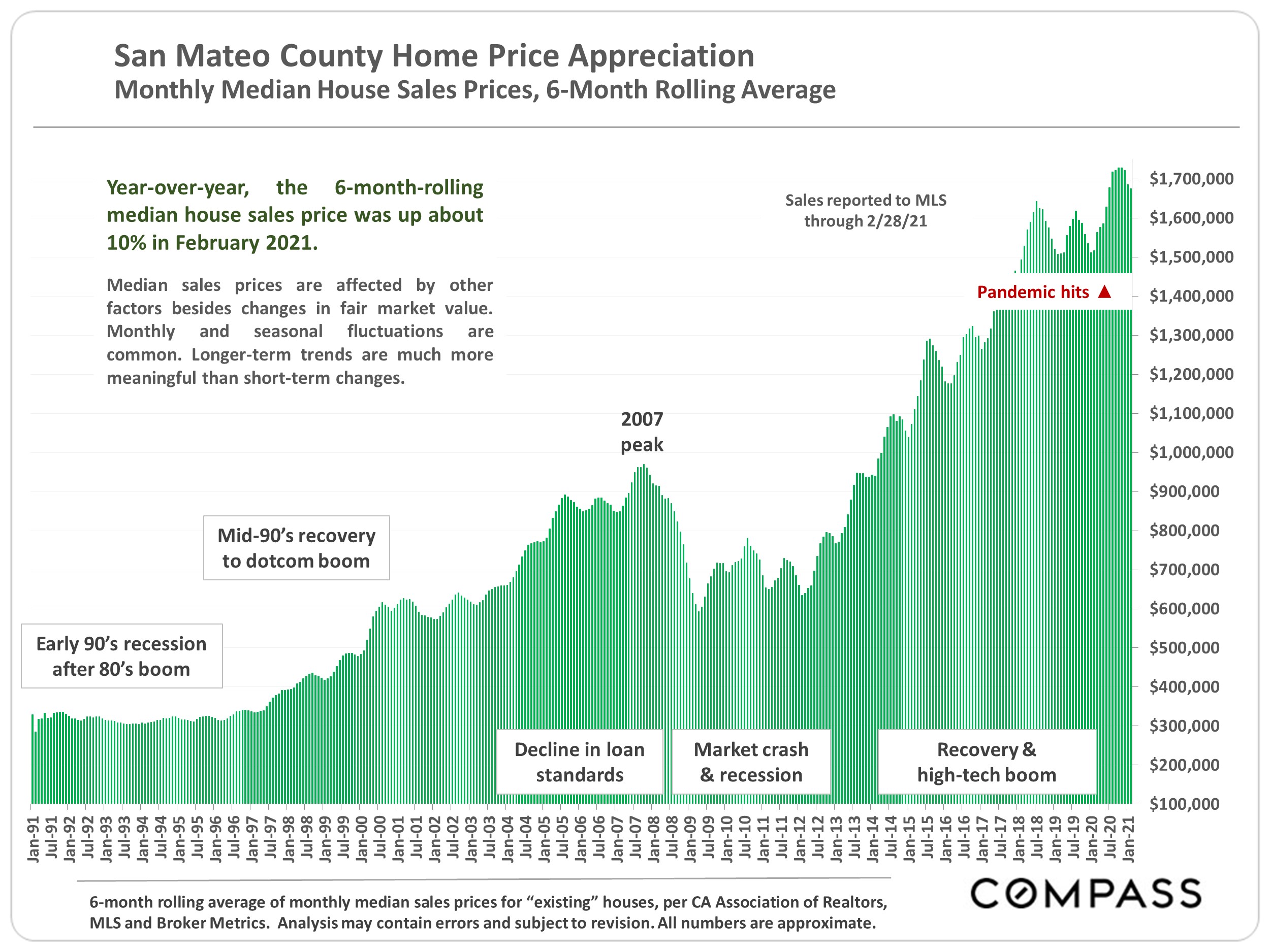

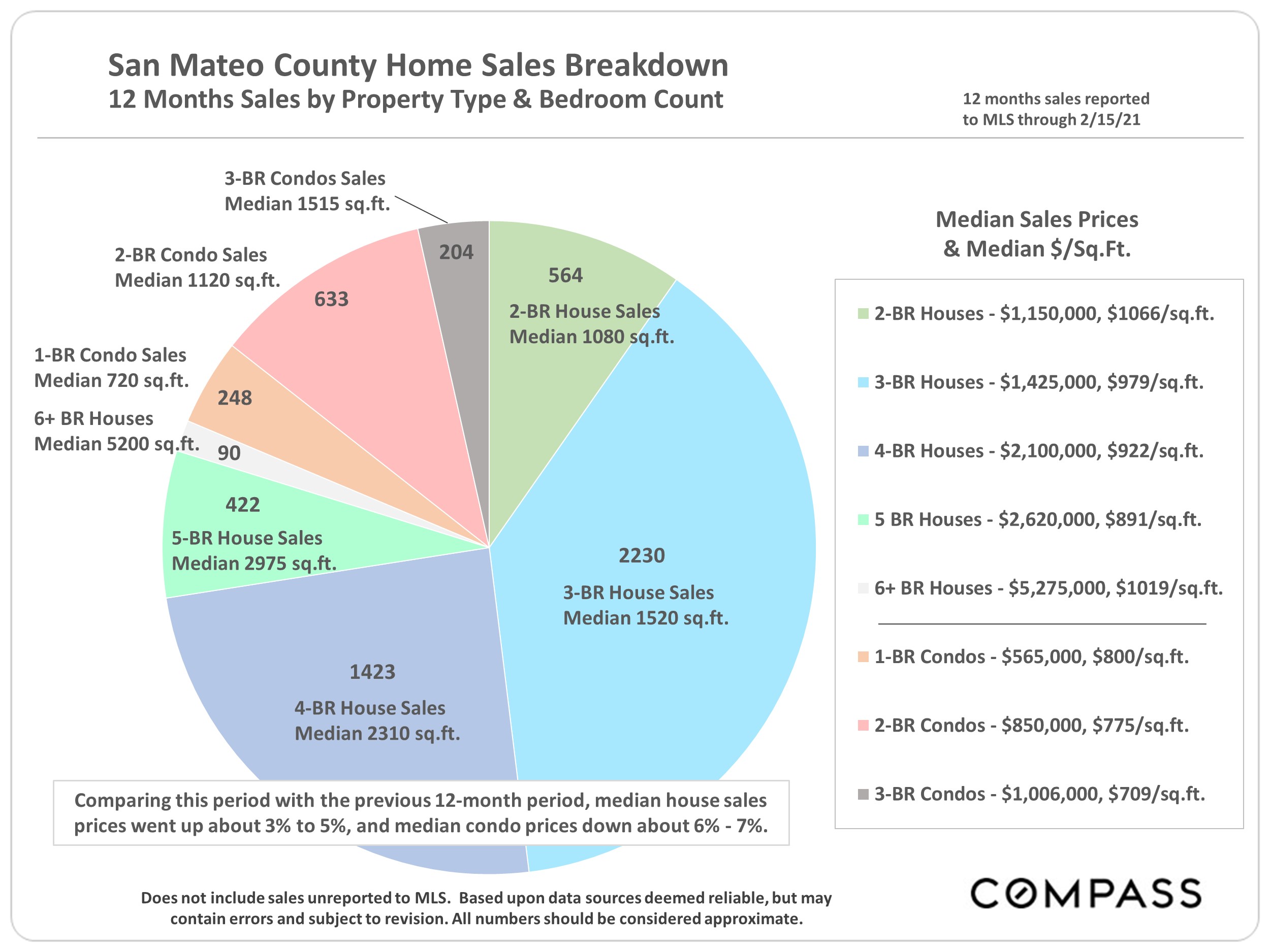

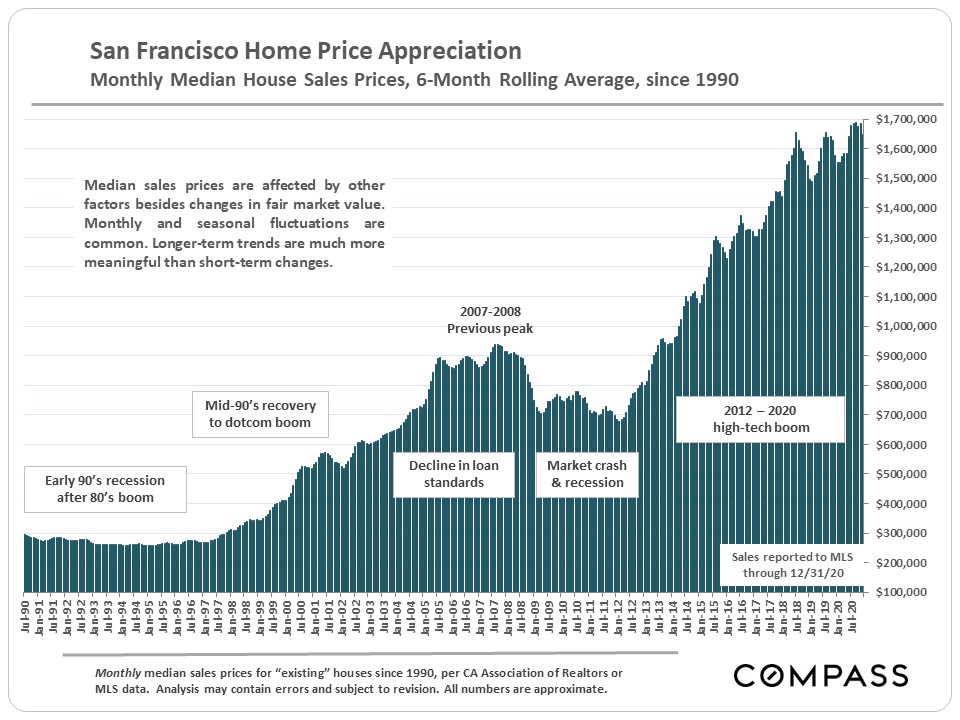

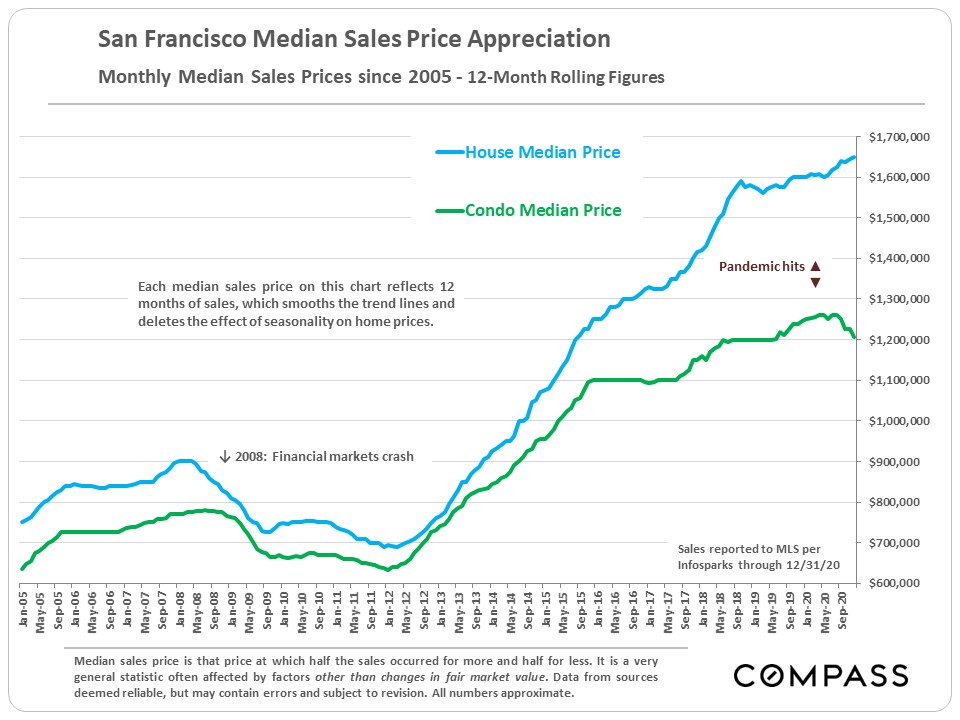

The first chart below illustrates a six-month rolling average of the monthly median house sales price, so it will reflect seasonal fluctuations (as well as other factors). The second chart illustrates 12-month rolling calculations of house and condo median sales prices, which smooth out the trend lines and eliminate the effects of seasonality.

Source: Compass

It is impossible to know how median and average value statistics apply to any particular home without a specific comparative market analysis. Below Market Rate (BMR) condos were excluded from this analysis.

These analyses were made in good faith with data from sources deemed reliable, but may contain errors and are subject to revision. It is not our intent to convince you of a particular position, but to attempt to provide straightforward data and analysis, so you can make your own informed decisions. Median and average statistics are enormous generalities: There are hundreds of different markets in San Francisco and the Bay Area, each with its own unique dynamics. Median prices and average dollar per square foot values can be and often are affected by other factors besides changes in fair market value. Longer term trends are much more meaningful than short-term.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognizing you when you return to our website, and helping our team to understand which sections of the website you find most interesting and useful. Learn more about how we use this information in our Privacy Policy.

You can adjust all of your cookie settings by navigating the tabs on the left hand side.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.