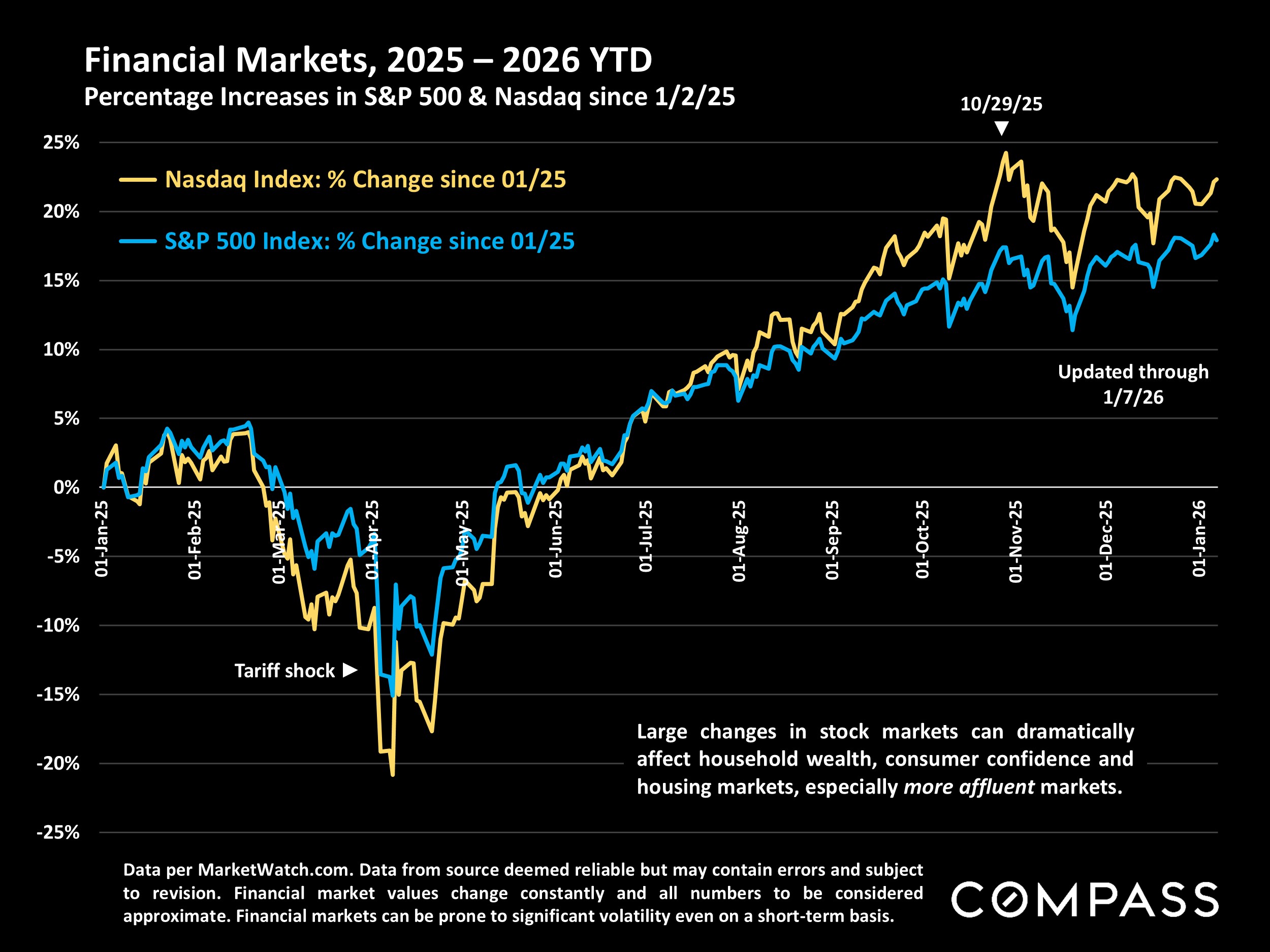

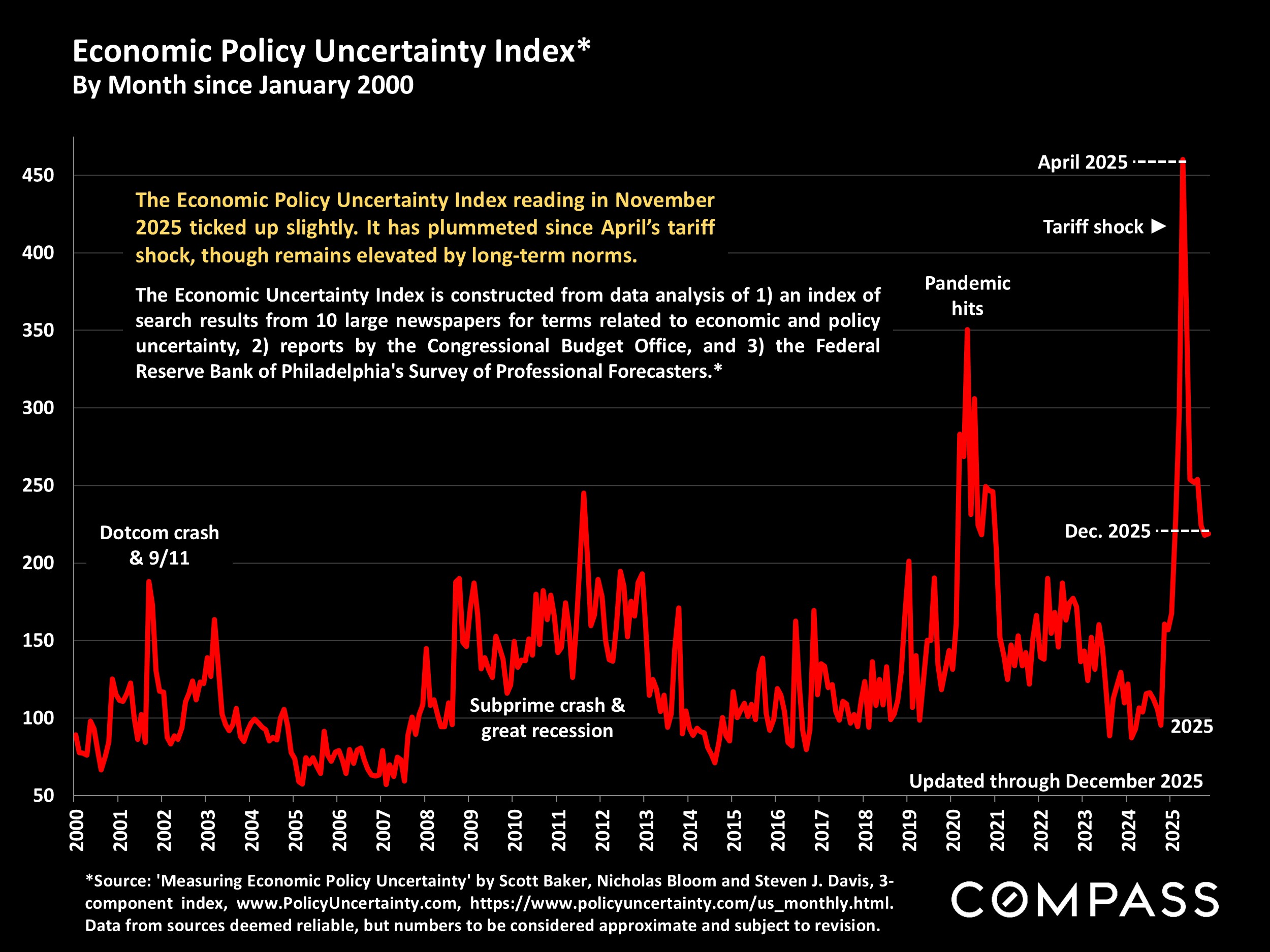

In 2025, Bay Area real estate markets started the year with strong buyer demand but had much of the wind taken out of their sails by the political/economic uncertainty that soared in early spring. Then, in mid-late summer, stock markets rebounded to hit new highs, and interest rates began a sustained decline, initiating a shift in the psychology of buyers and sellers that is still developing. Still, national consumer confidence readings showed a significant split between the outlooks of more and less affluent households, and that affected market segments in different ways.

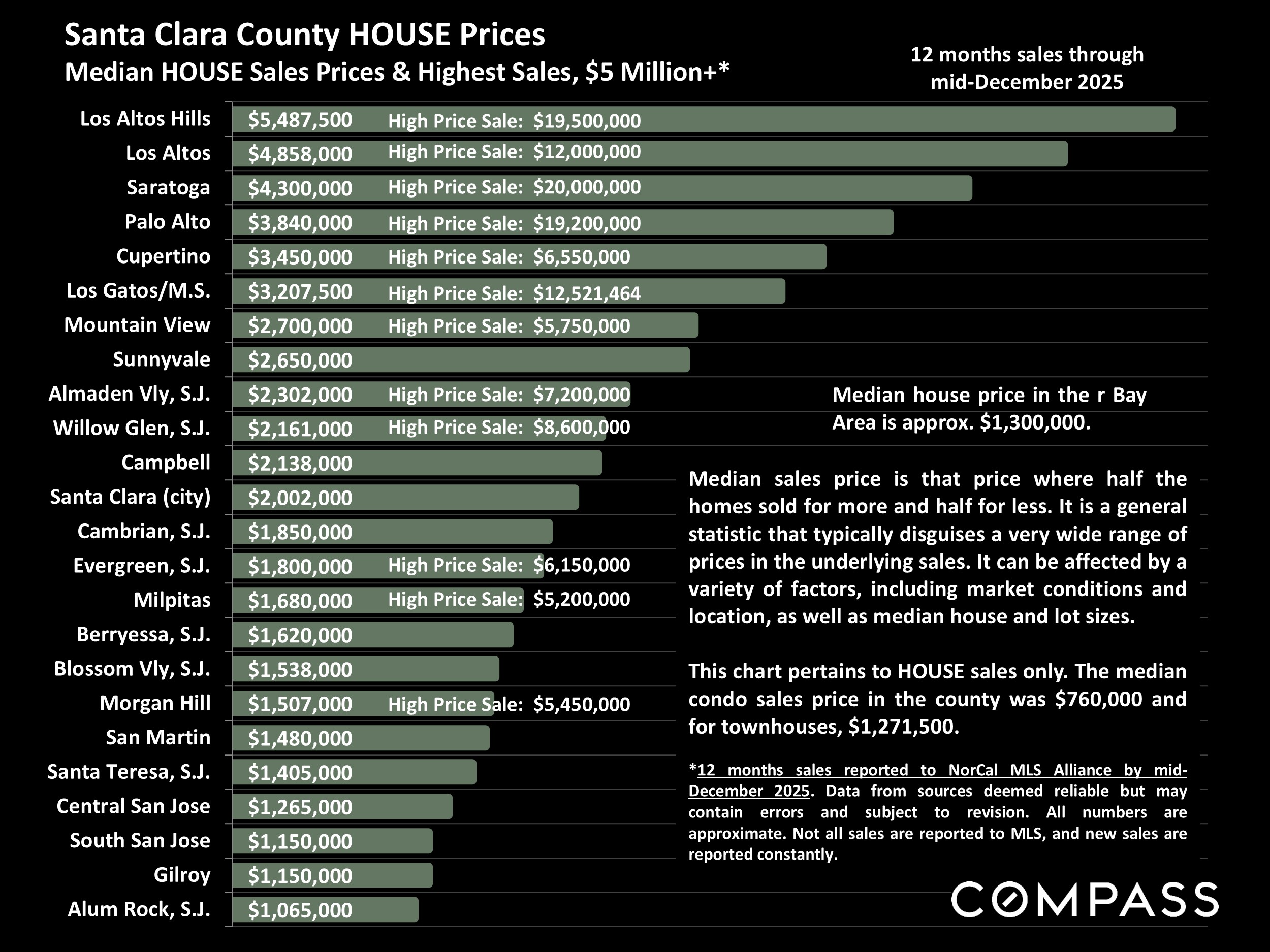

Generally speaking, more expensive markets, powered by rising demand from affluent buyers seeing substantial increases in household wealth from stock market gains, performed better than more affordable markets, which tended to be more impacted by concerns regarding inflation, affordability and employment. Of course, Santa Clara County has some of the most affluent cities in the U.S.

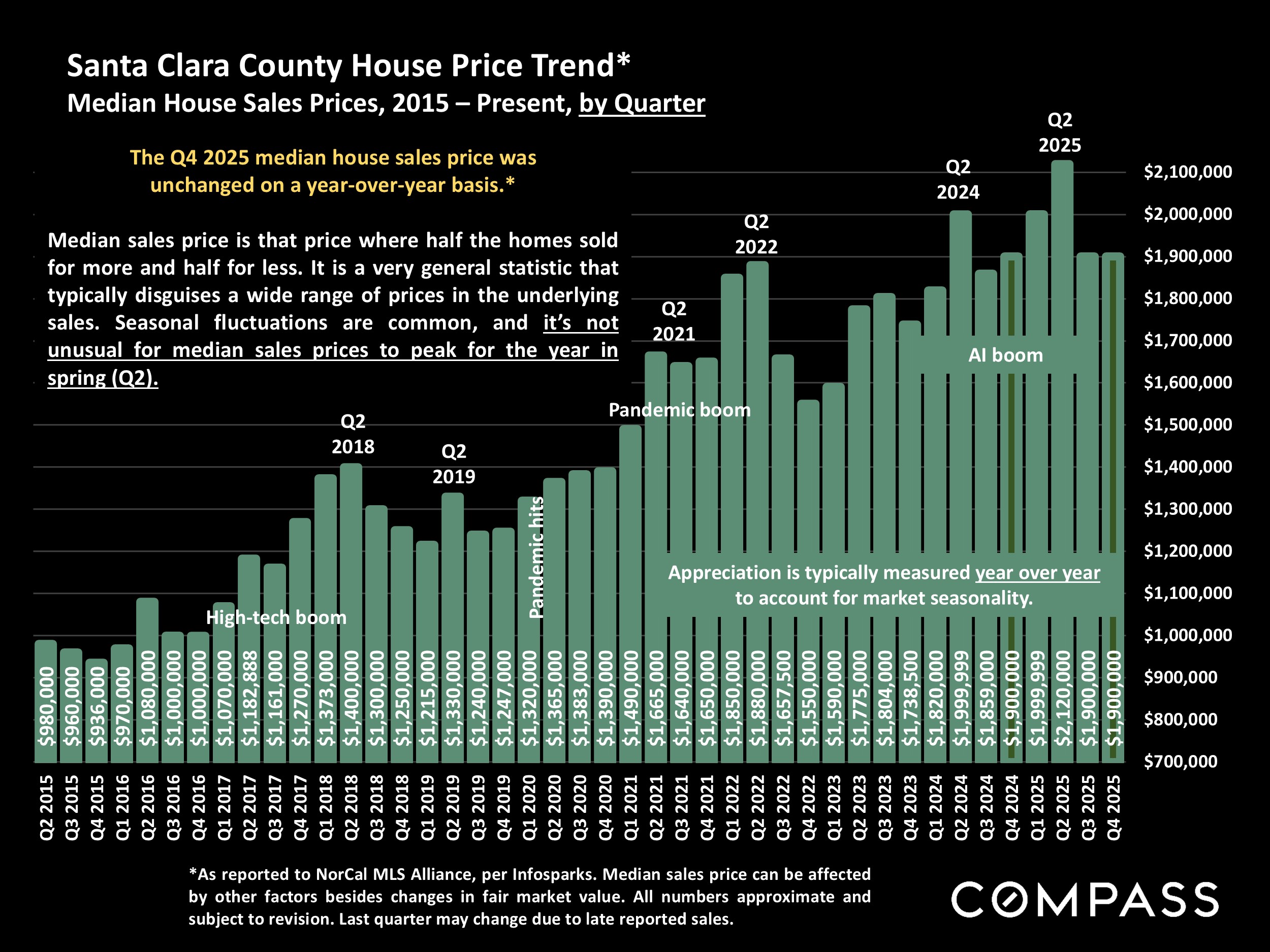

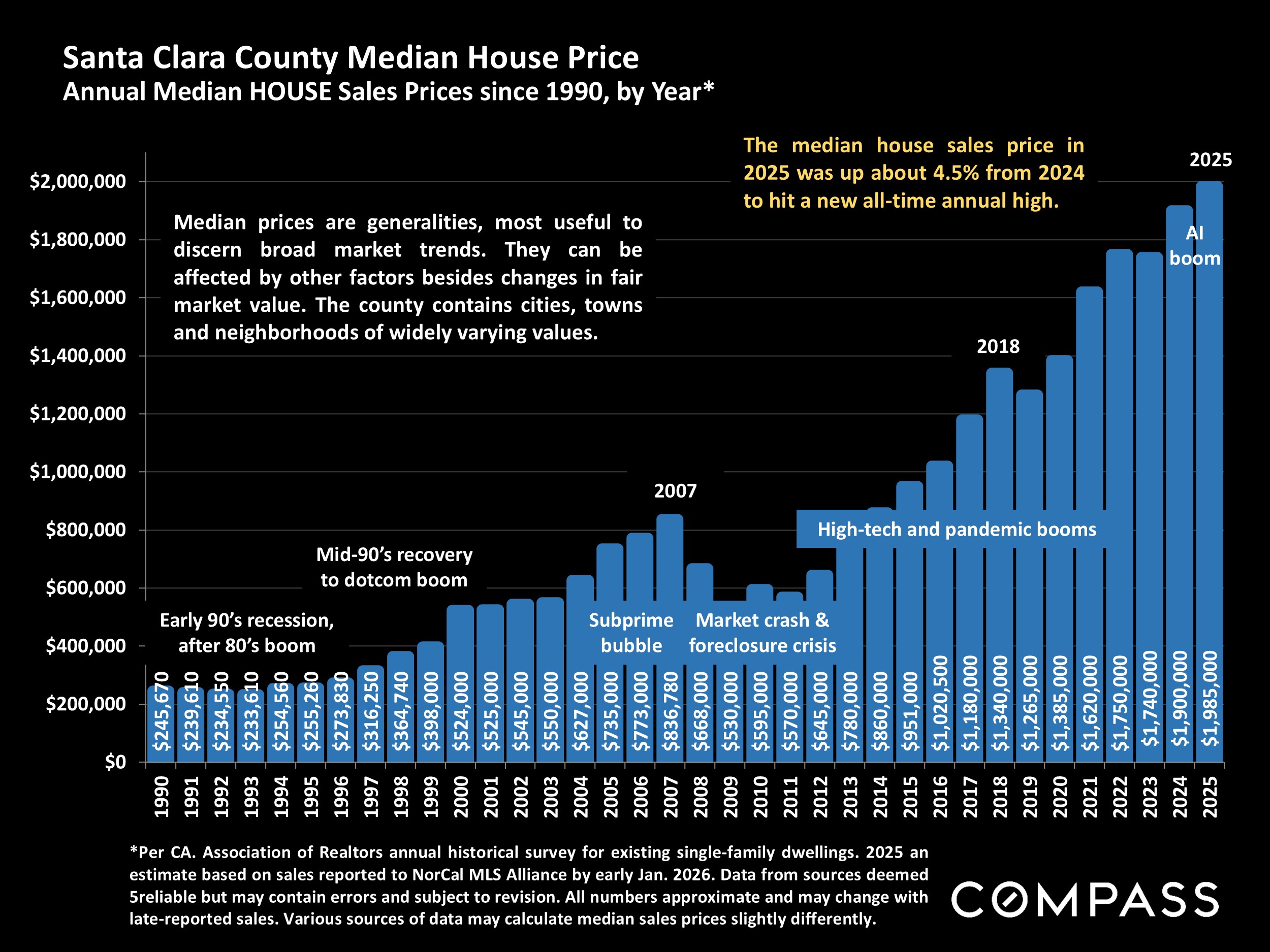

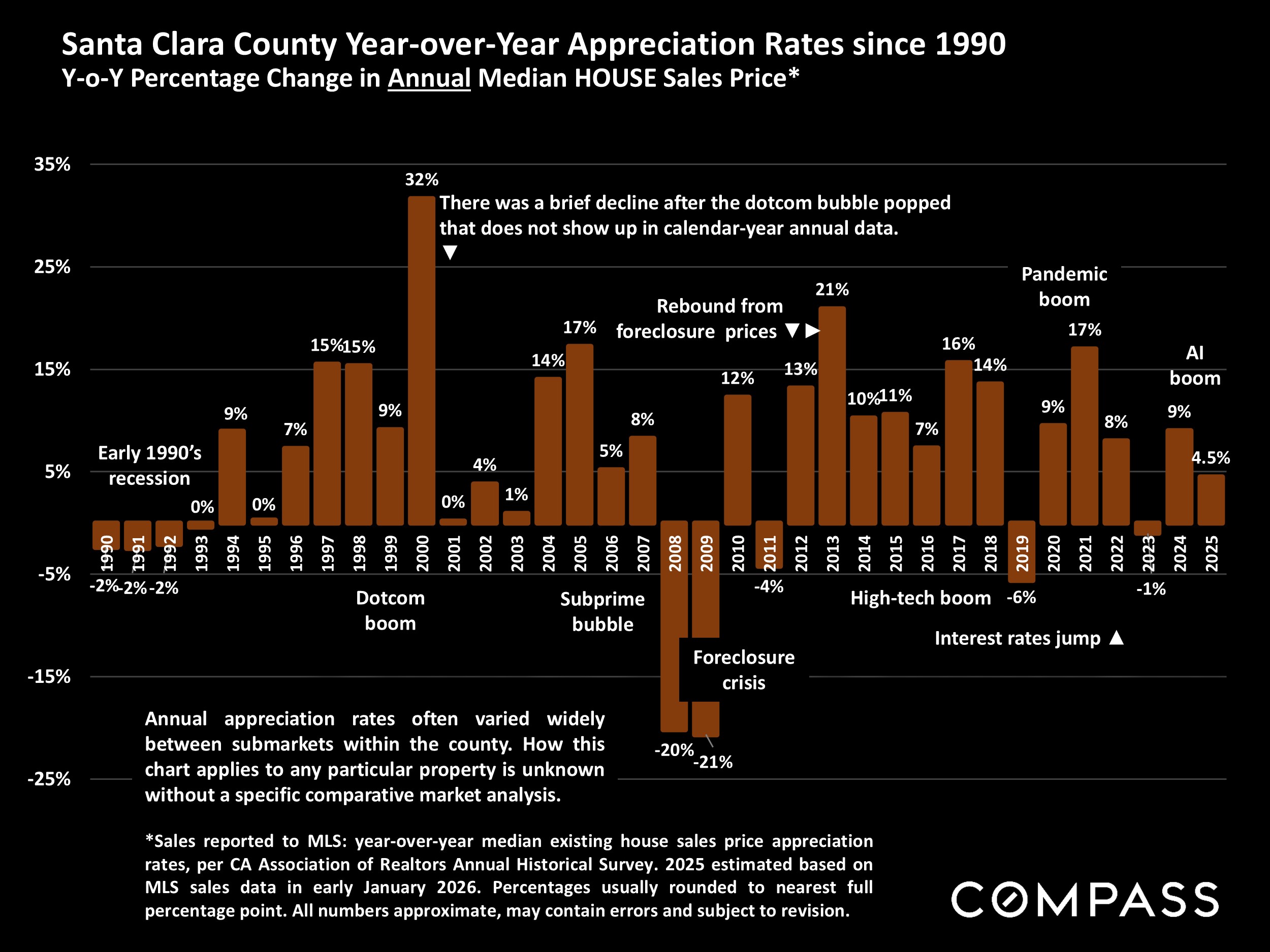

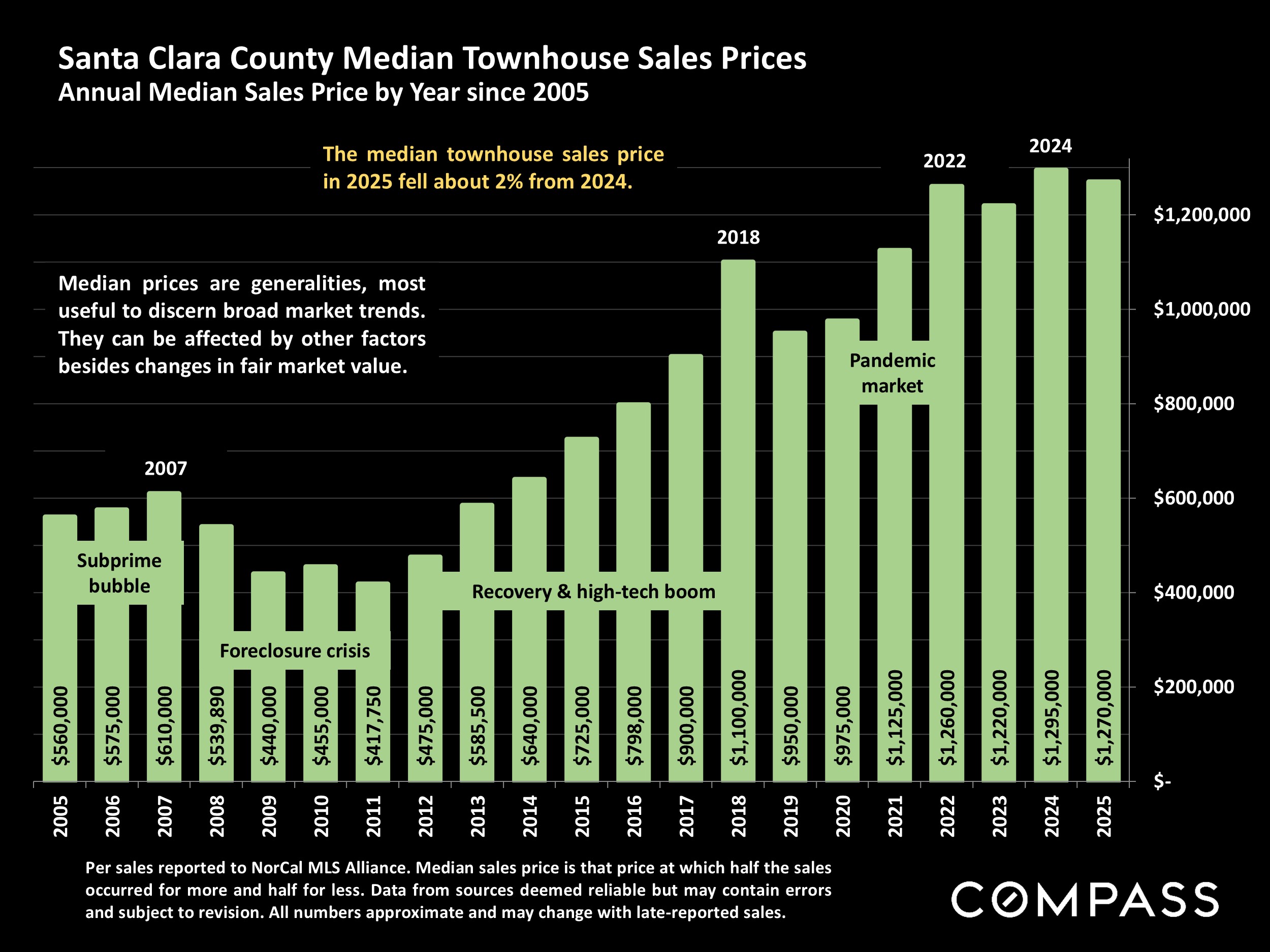

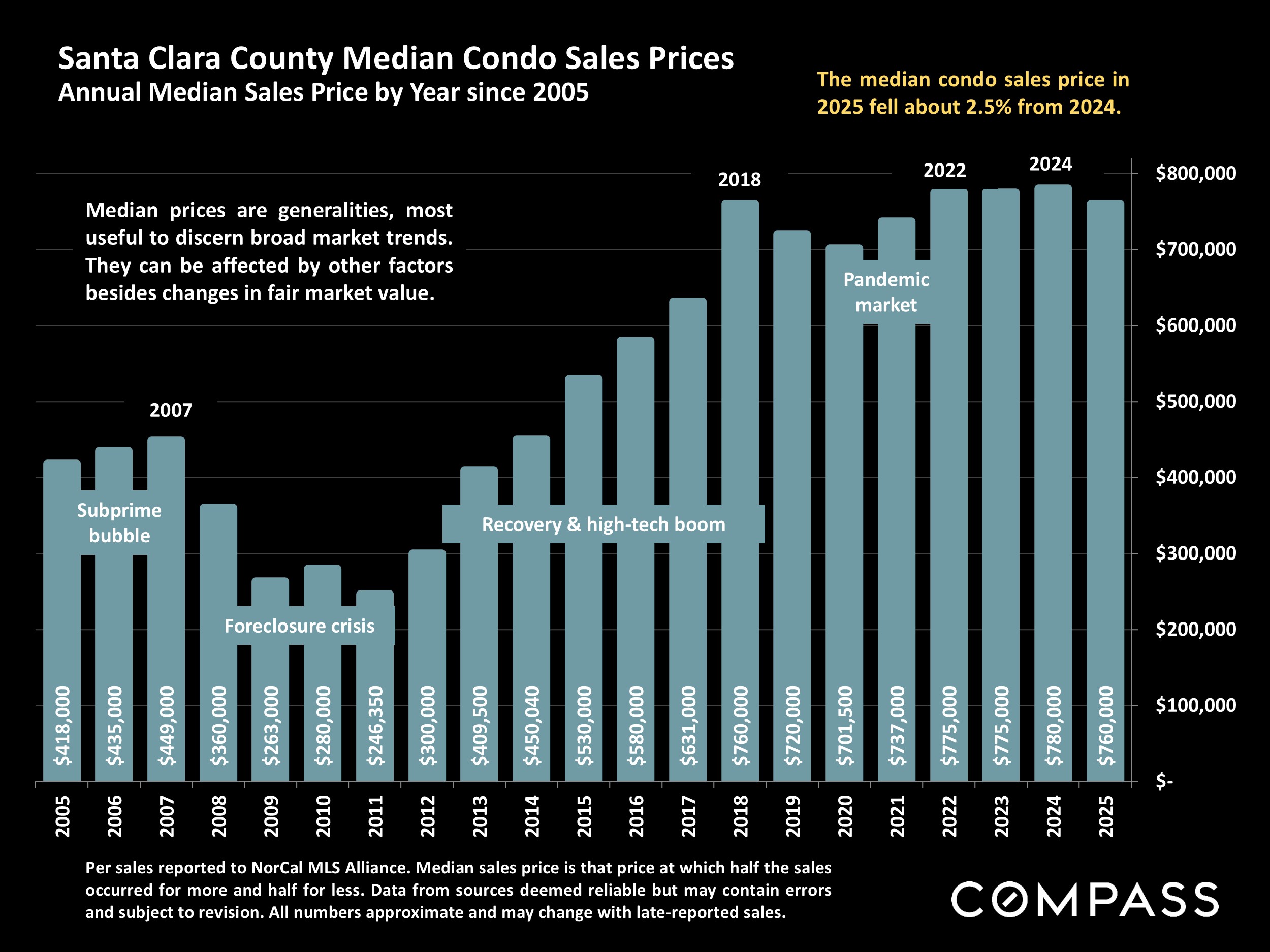

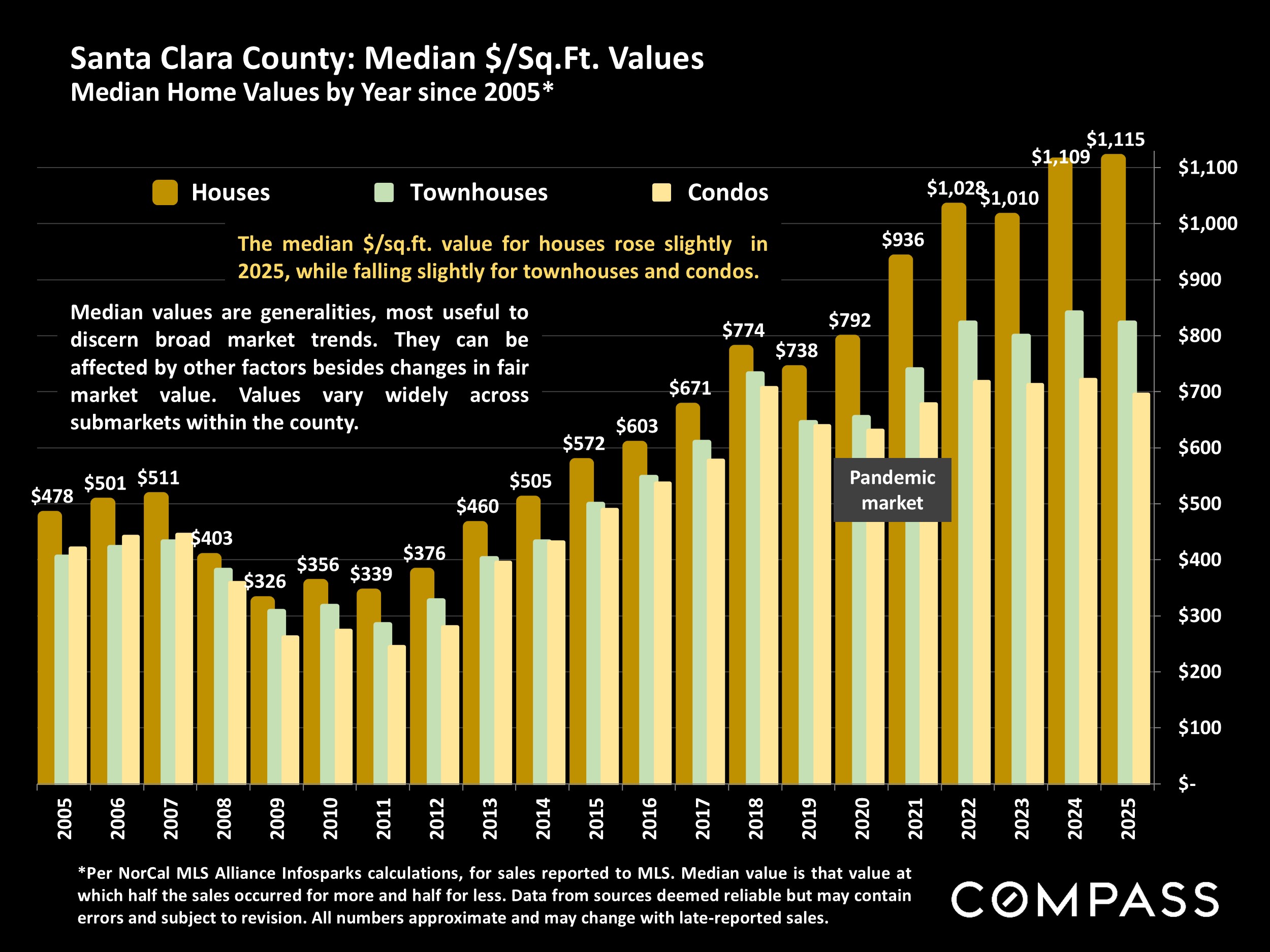

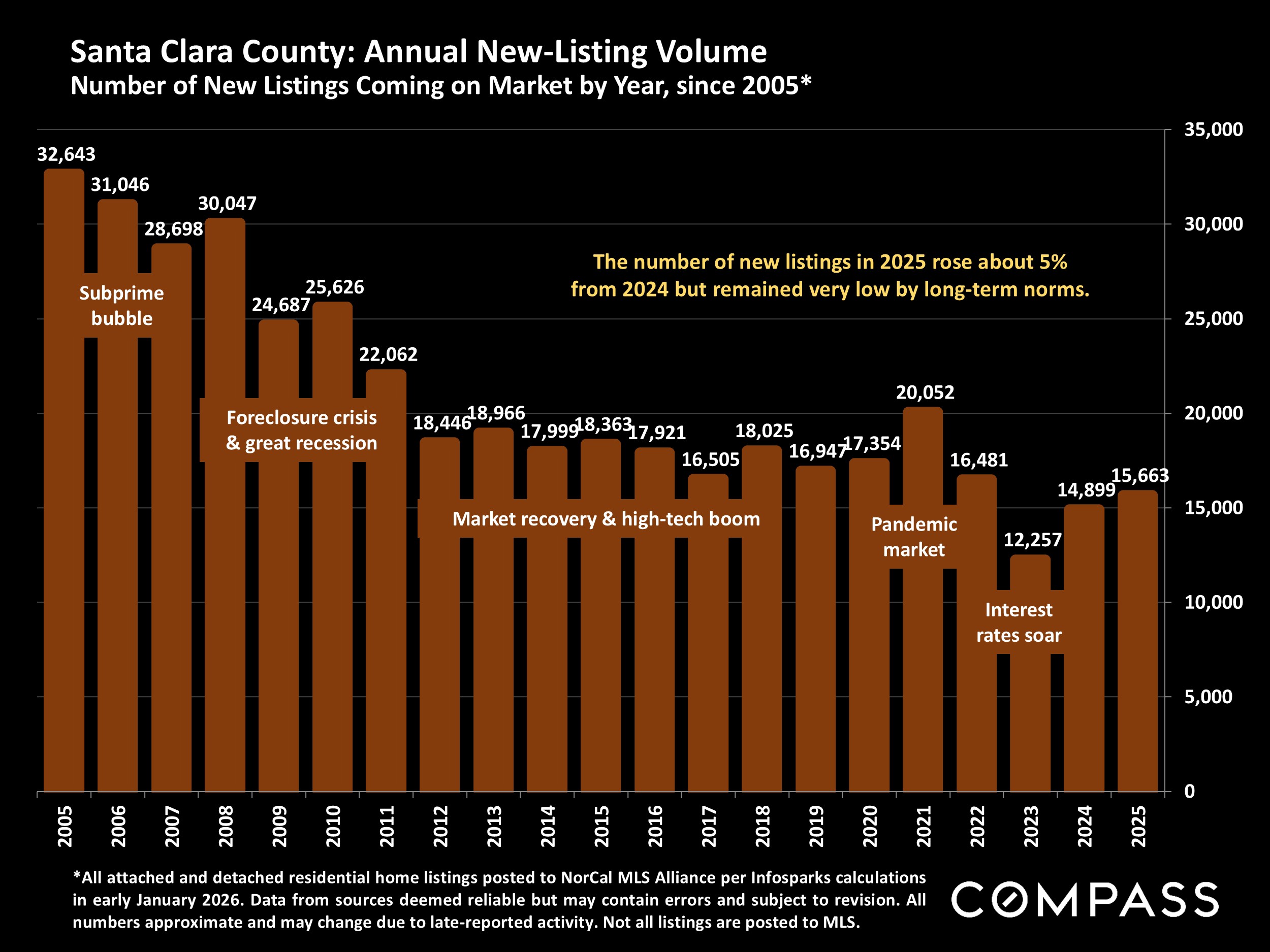

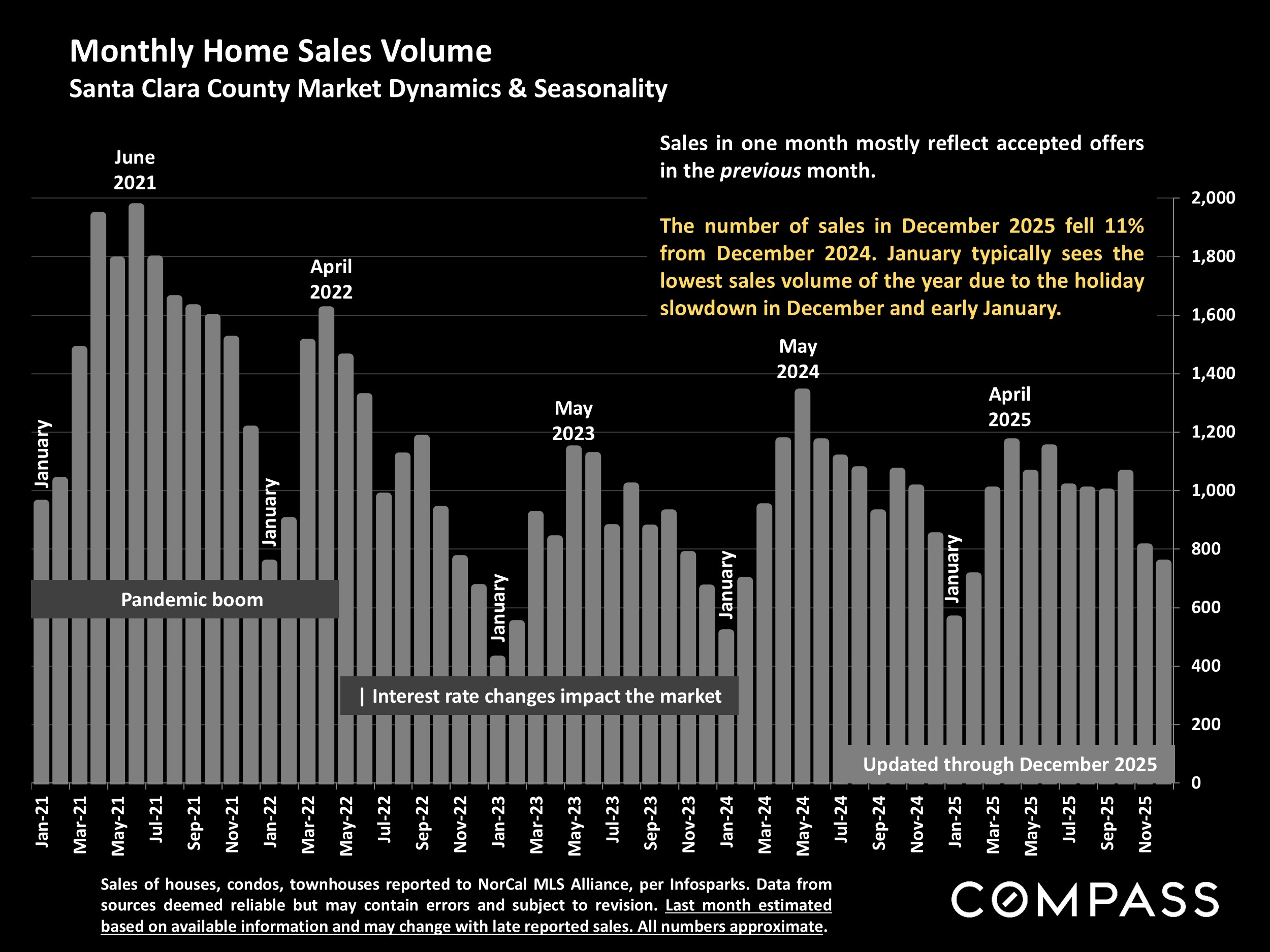

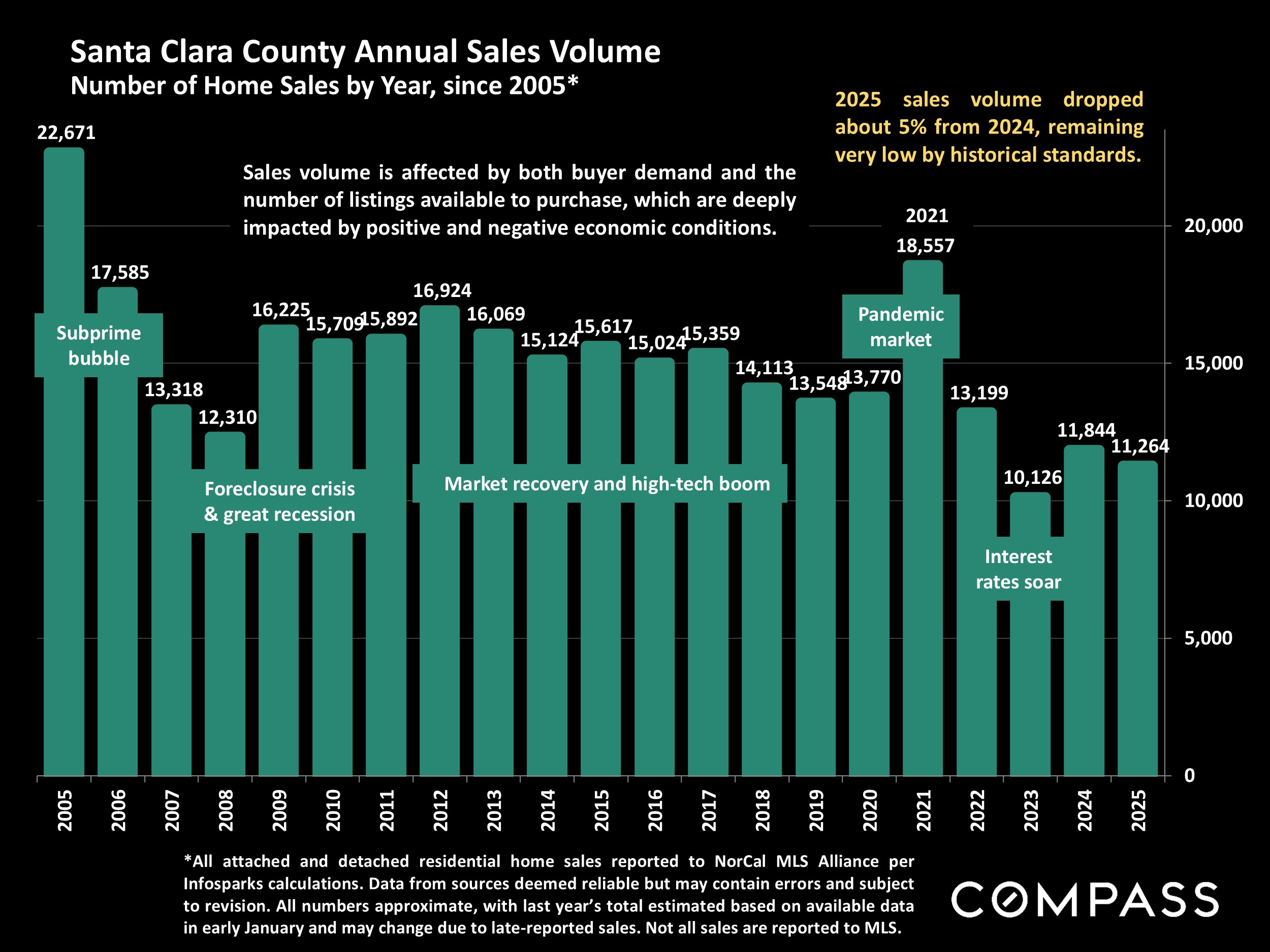

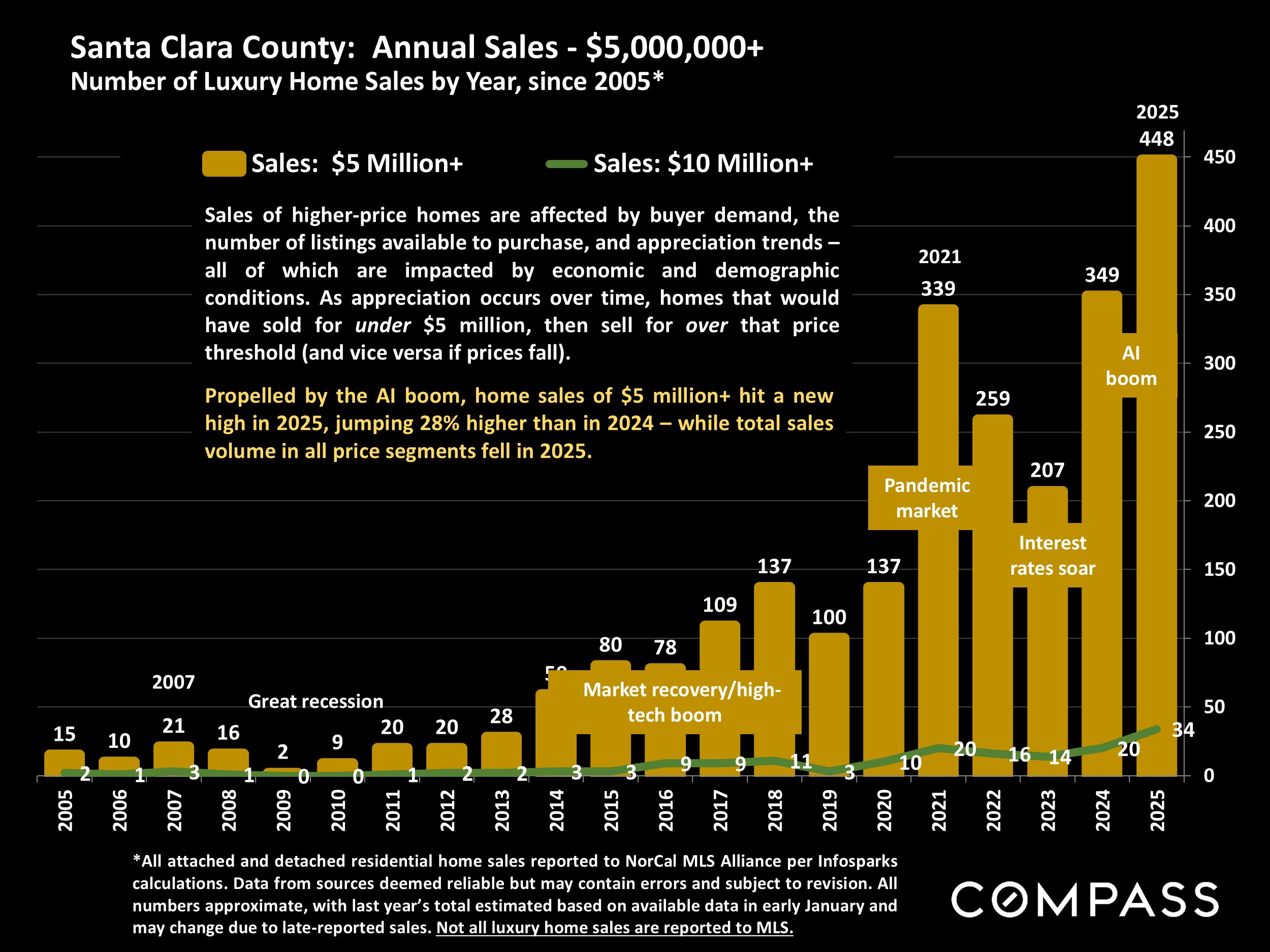

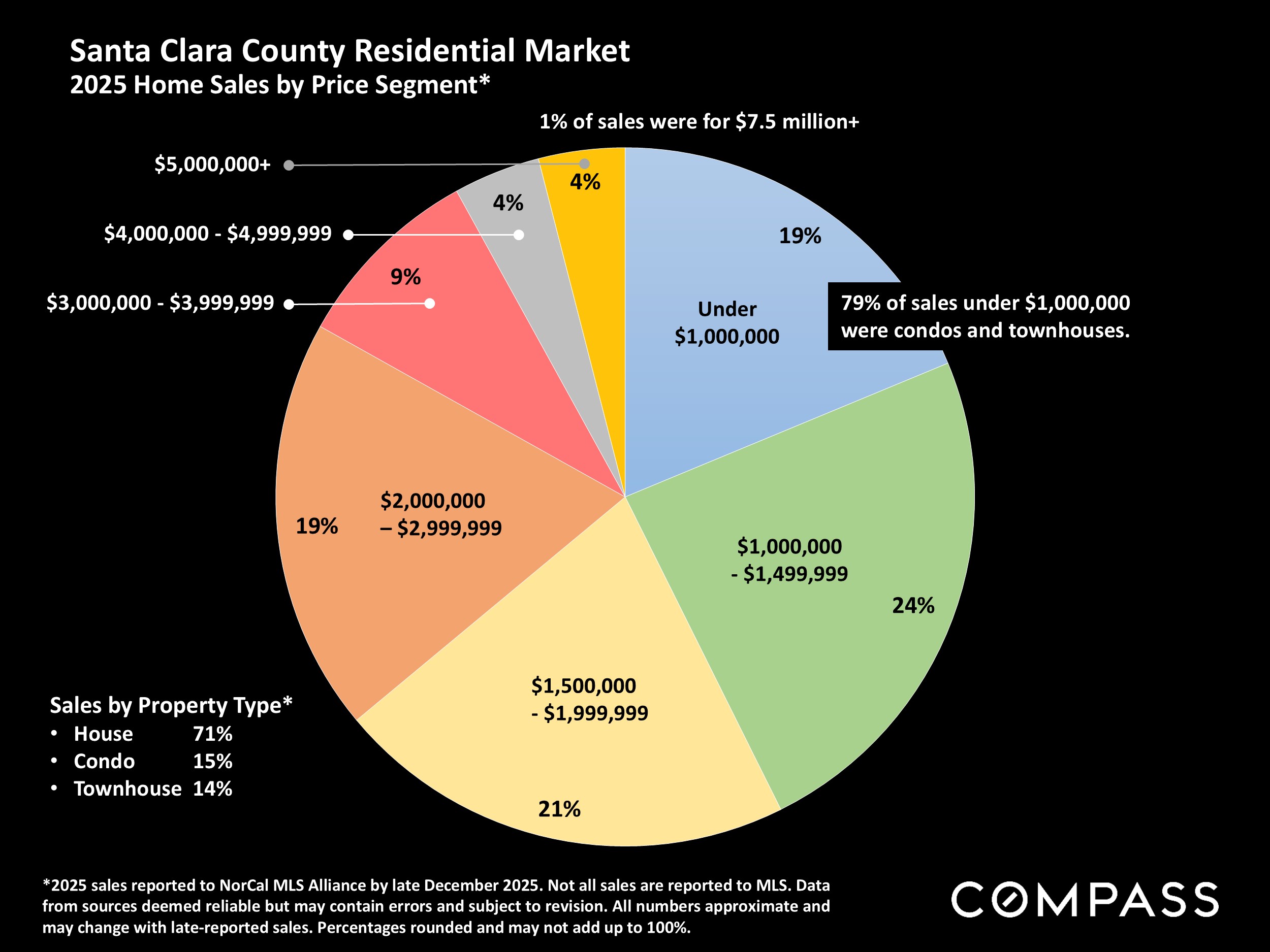

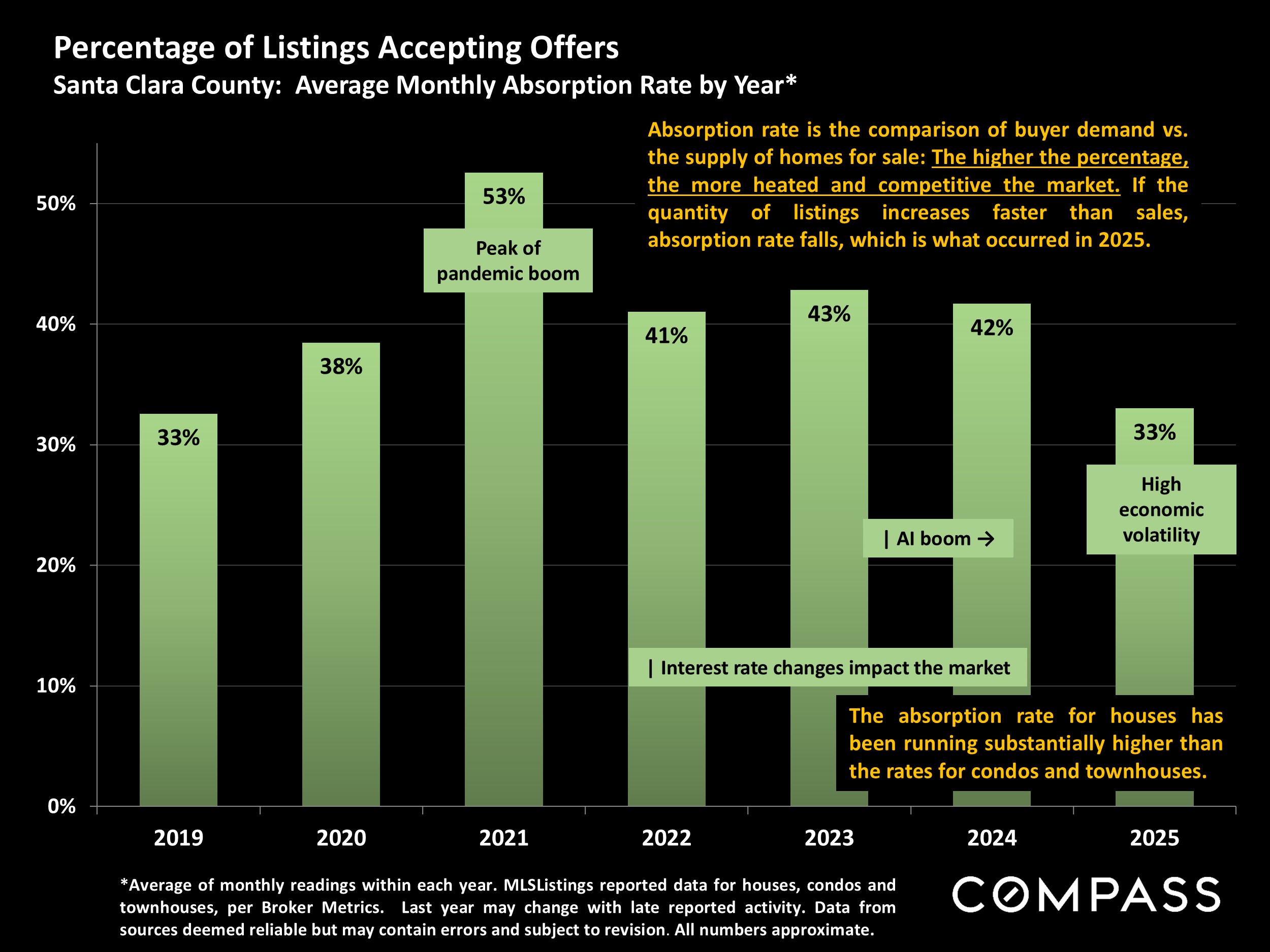

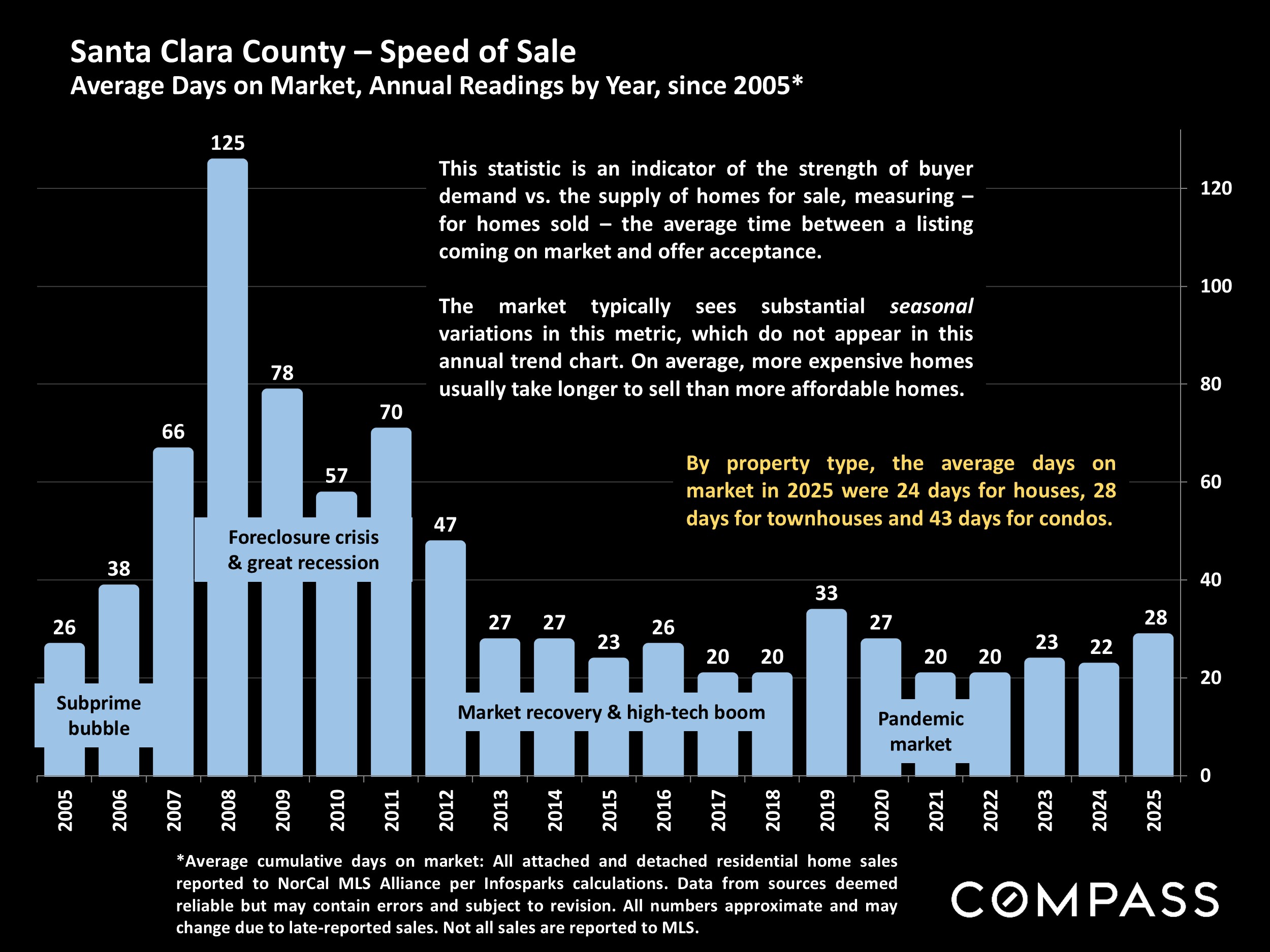

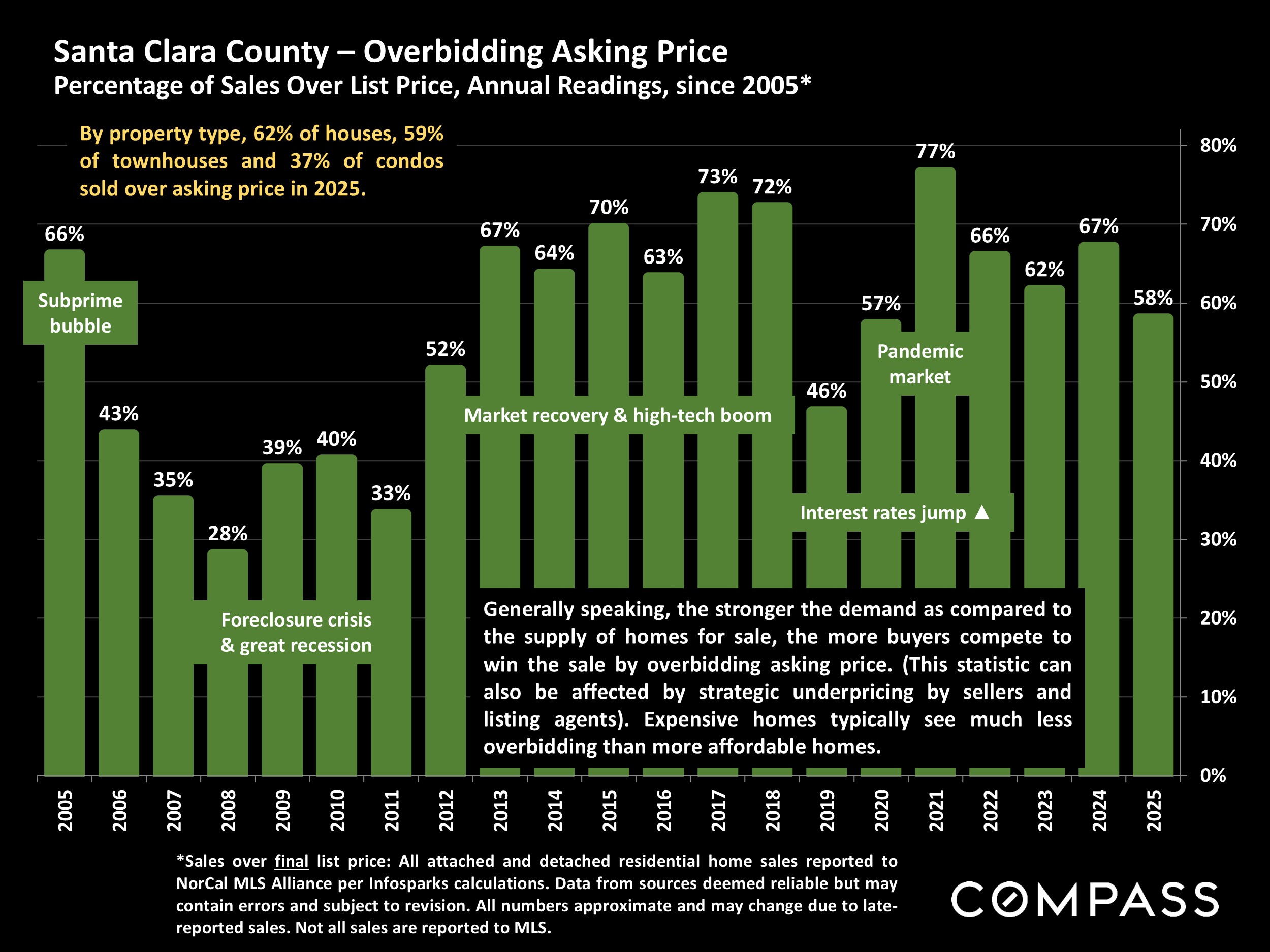

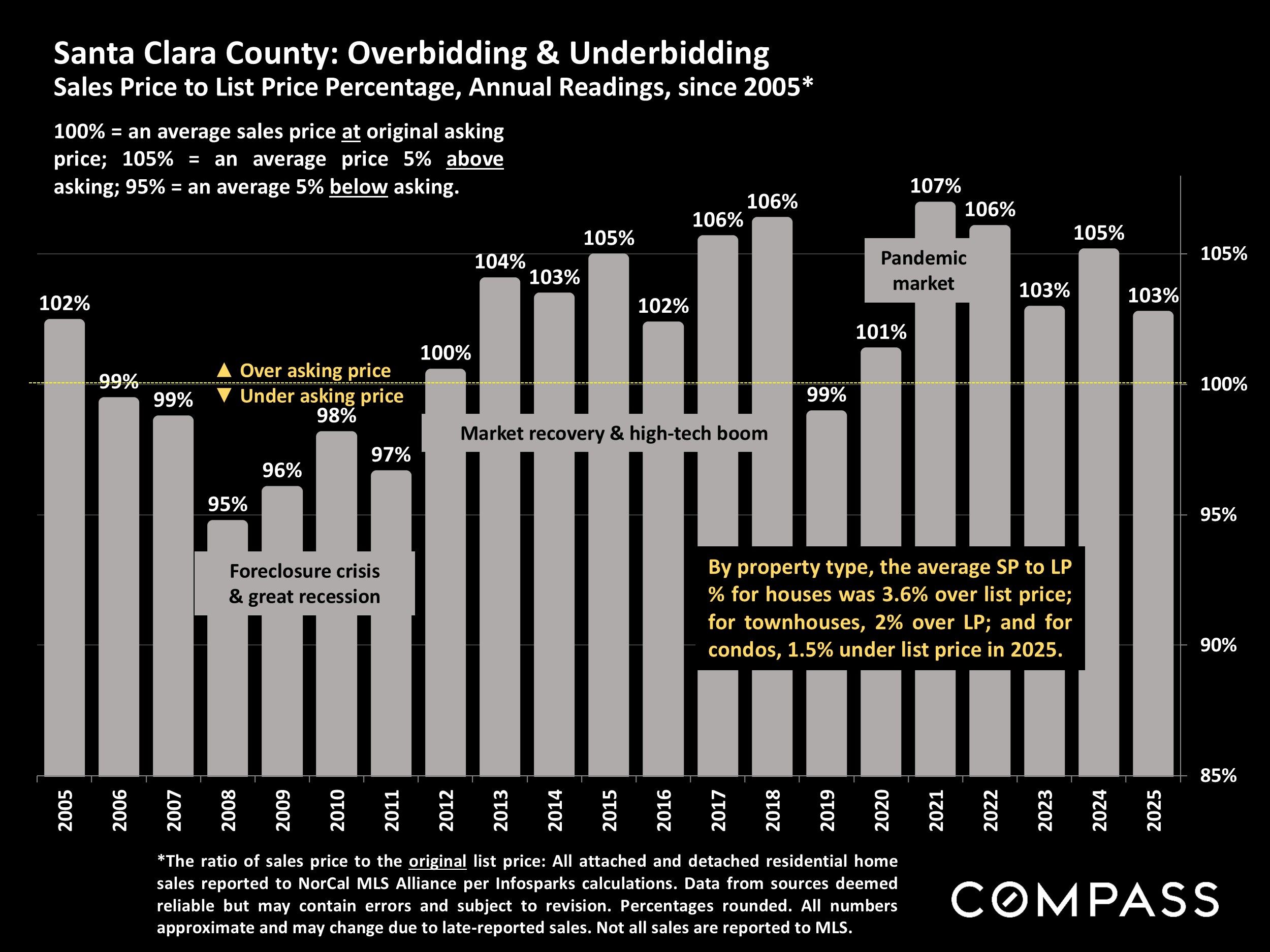

By many standard statistical measures – illustrated in this report – the county’s market cooled from 2024, but fueled by the AI boom, it remained one of the strongest markets in the country. Its median house sales price hit a new peak, though median townhouse and condo prices slightly declined. Total sales volume dropped 5% year over year, but luxury home sales soared 28% to a dramatic new high.

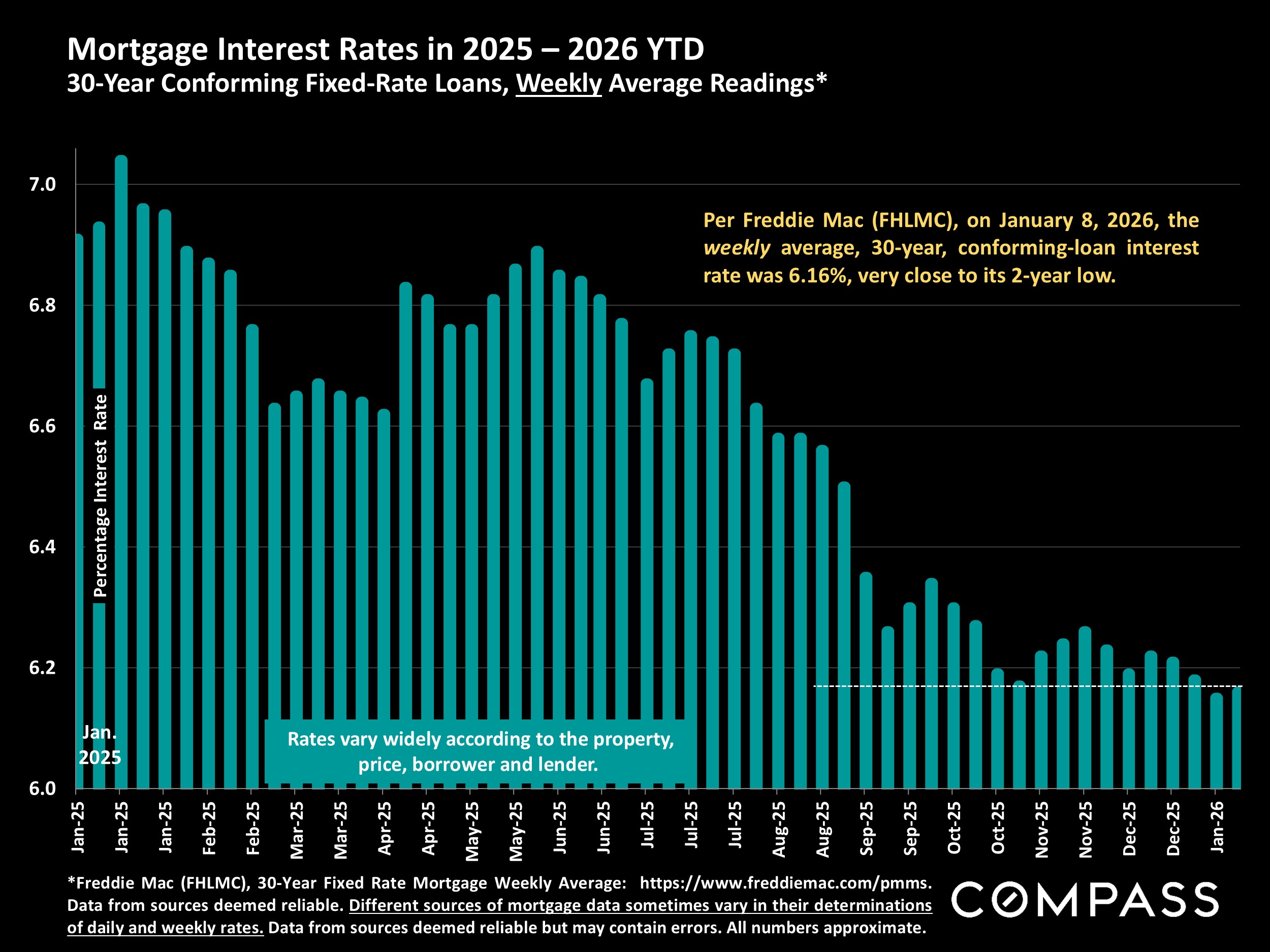

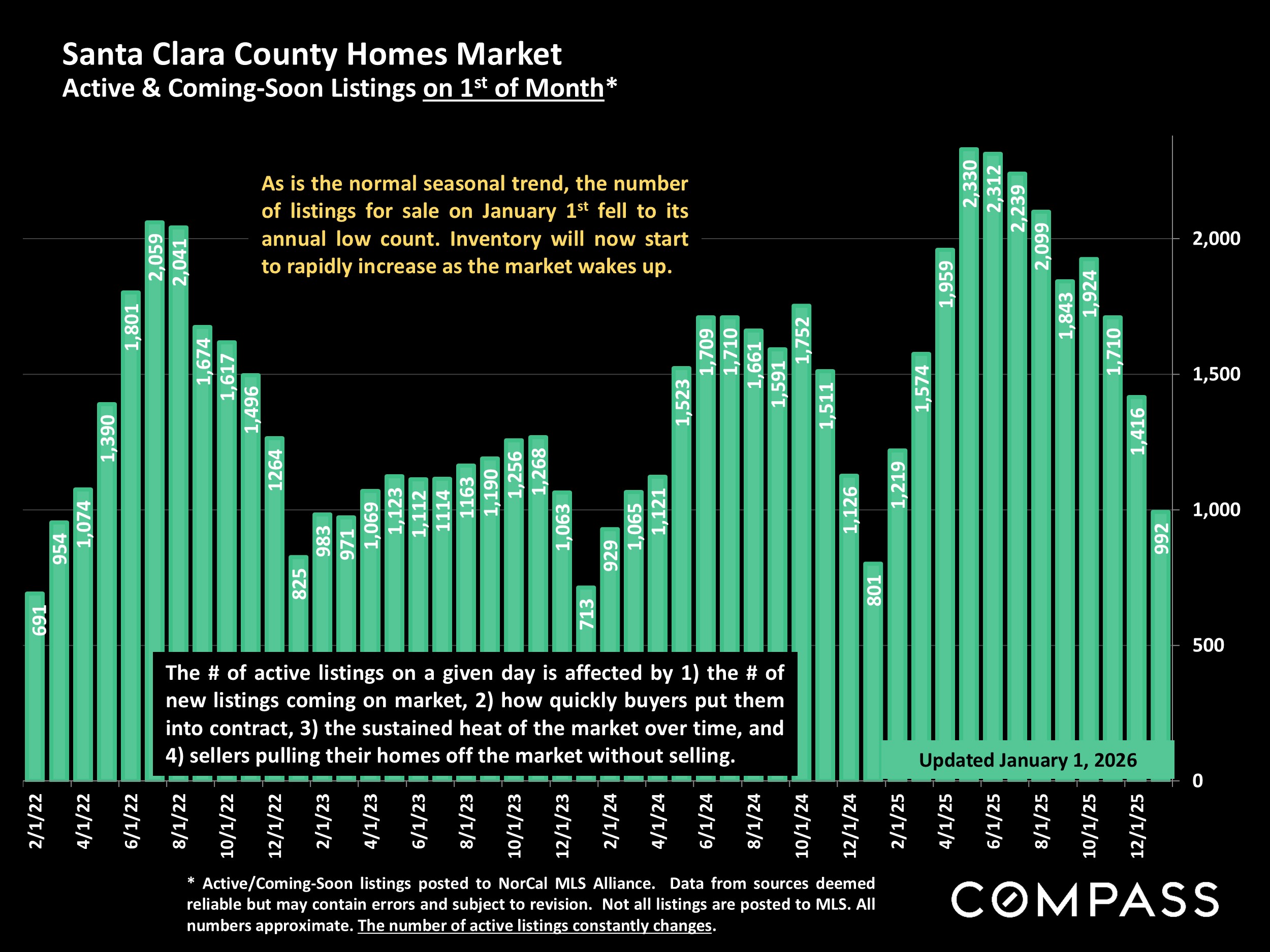

As 2026 begins, interest rates are near multi-year lows and stock markets are at or close to all-time peaks. Early in the new year, it is common for buyers, re-energized to move forward with major life decisions, to jump back into the market faster than sellers list their homes for sale. This disparity of increasing demand versus a low supply of new listings usually runs through the spring, typically making these months the most heated selling season of the year. Last year, this was weakened by the tariff shock. Barring new, unexpected economic alarms, we expect this spring to be stronger.

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics – such as “active listings,” “days on market,” and “months supply of inventory” – differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won’t be reflected in the data. “Homes” signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, unless otherwise delineated. Multi-county metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

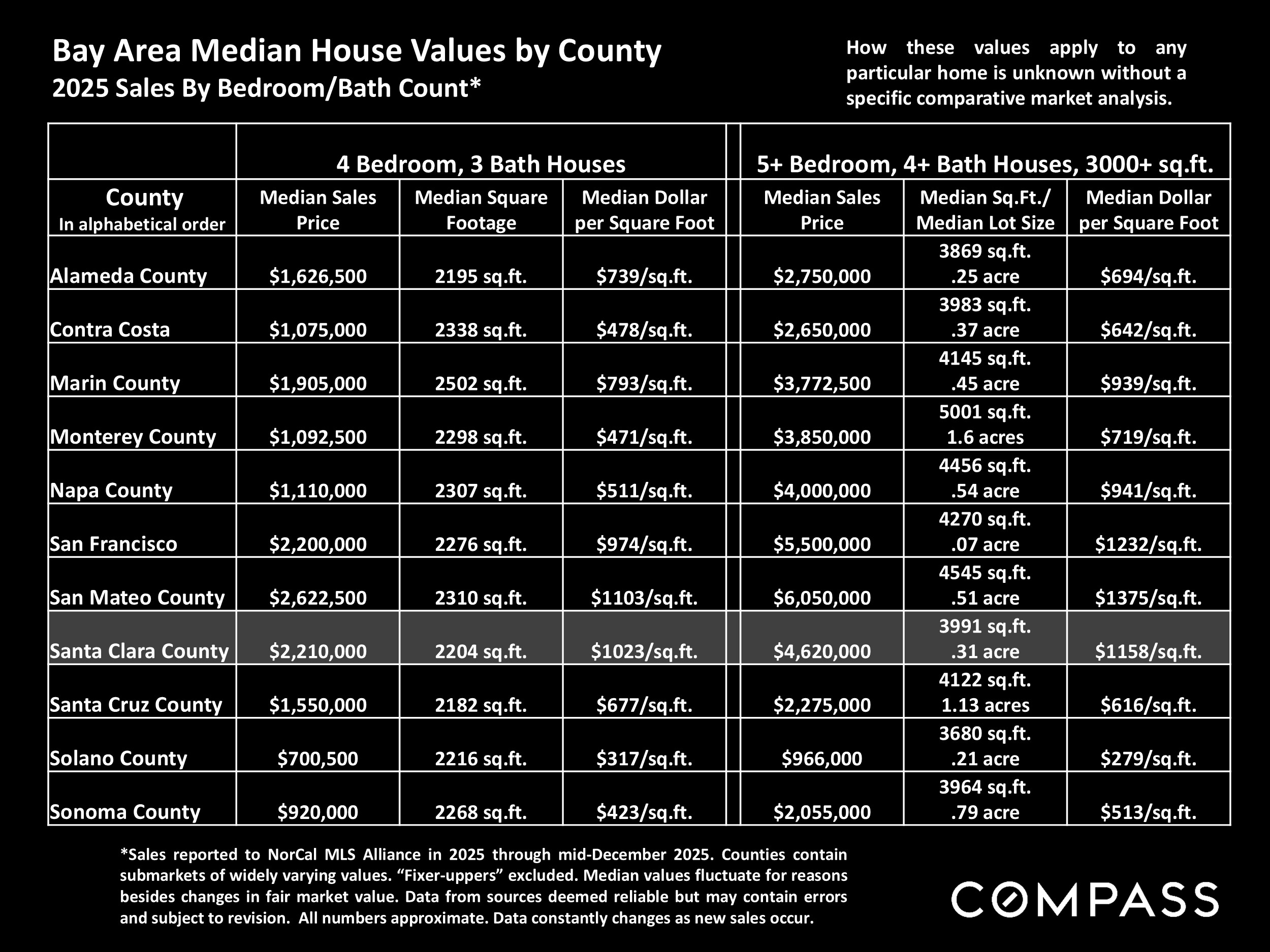

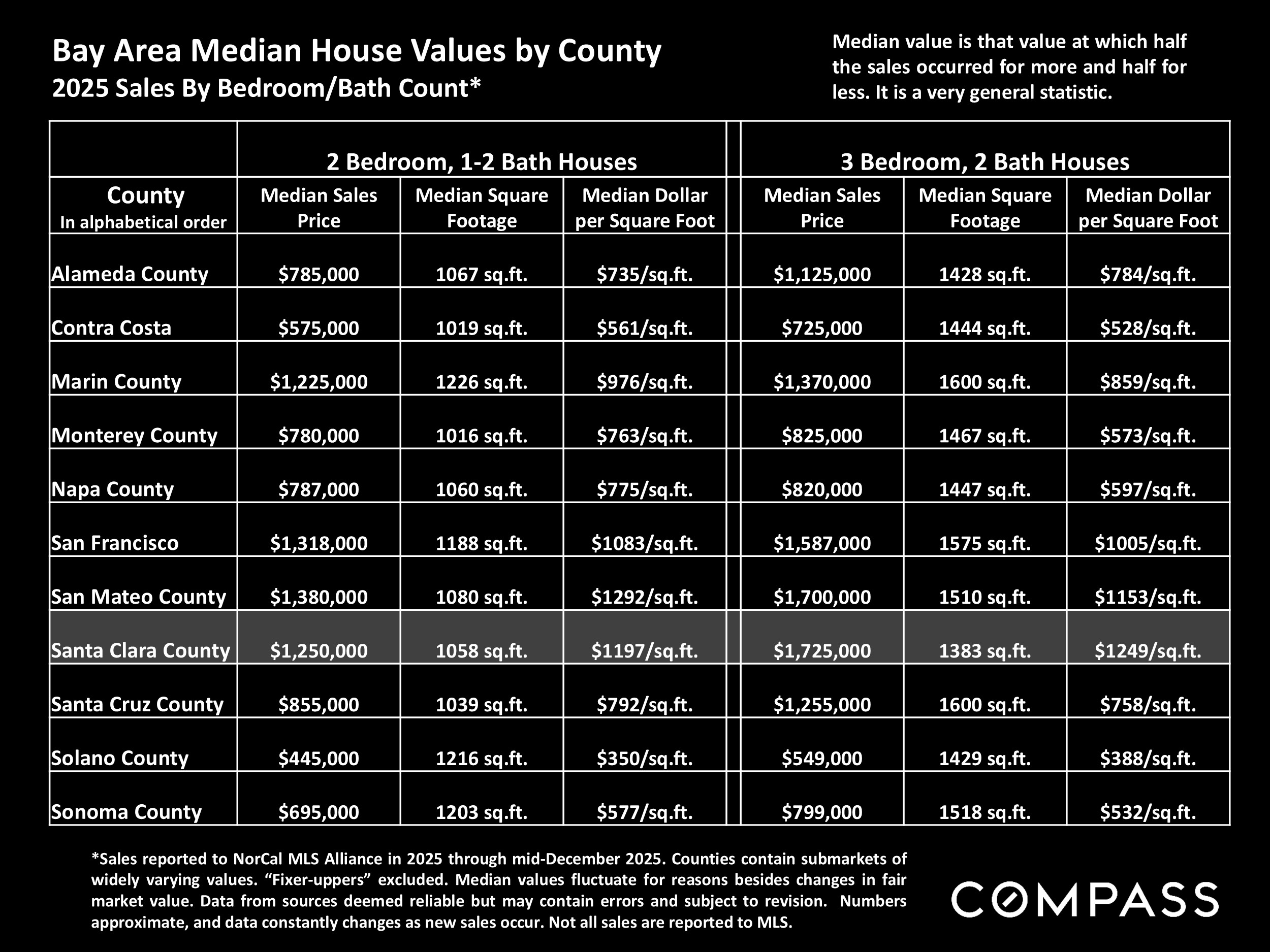

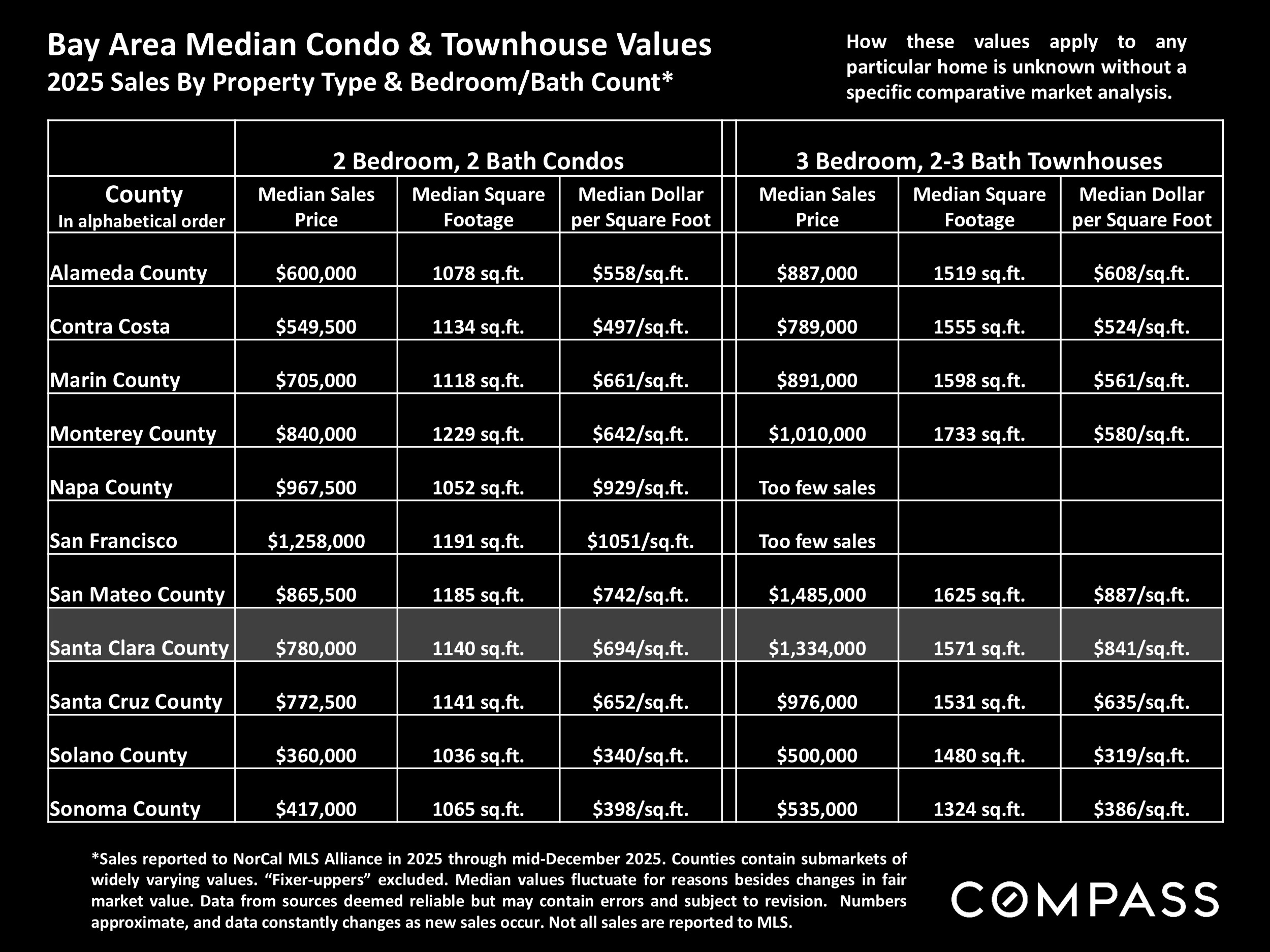

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, “bonus” rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis.

Median Sales Price is that price at which half the properties sold for more and half for less. It may be affected by seasonality, “unusual” events, or changes in inventory and buying trends, as well as by changes in fair market value. The median sales price for an area will often conceal an enormous variety of sales prices in the underlying individual sales.

Dollar per Square Foot is based upon the home’s interior living space and does not include garages, unfinished attics and basements, rooms built without permit, patios, decks or yards (though all those can add value to a home). These figures are usually derived from appraisals or tax records, but are sometimes unreliable (especially for older homes) or unreported altogether. The calculation can only be made on those home sales that reported square footage.