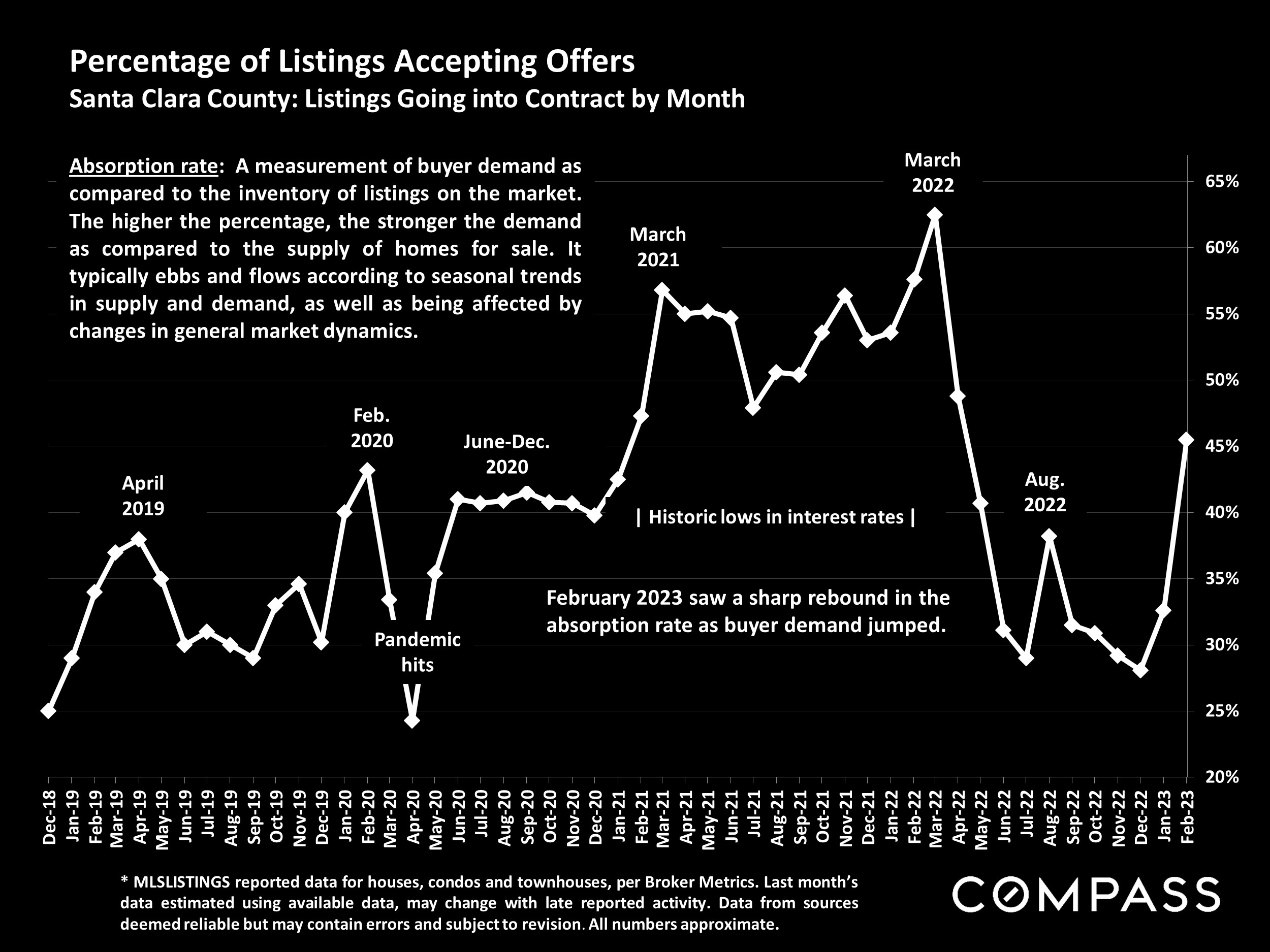

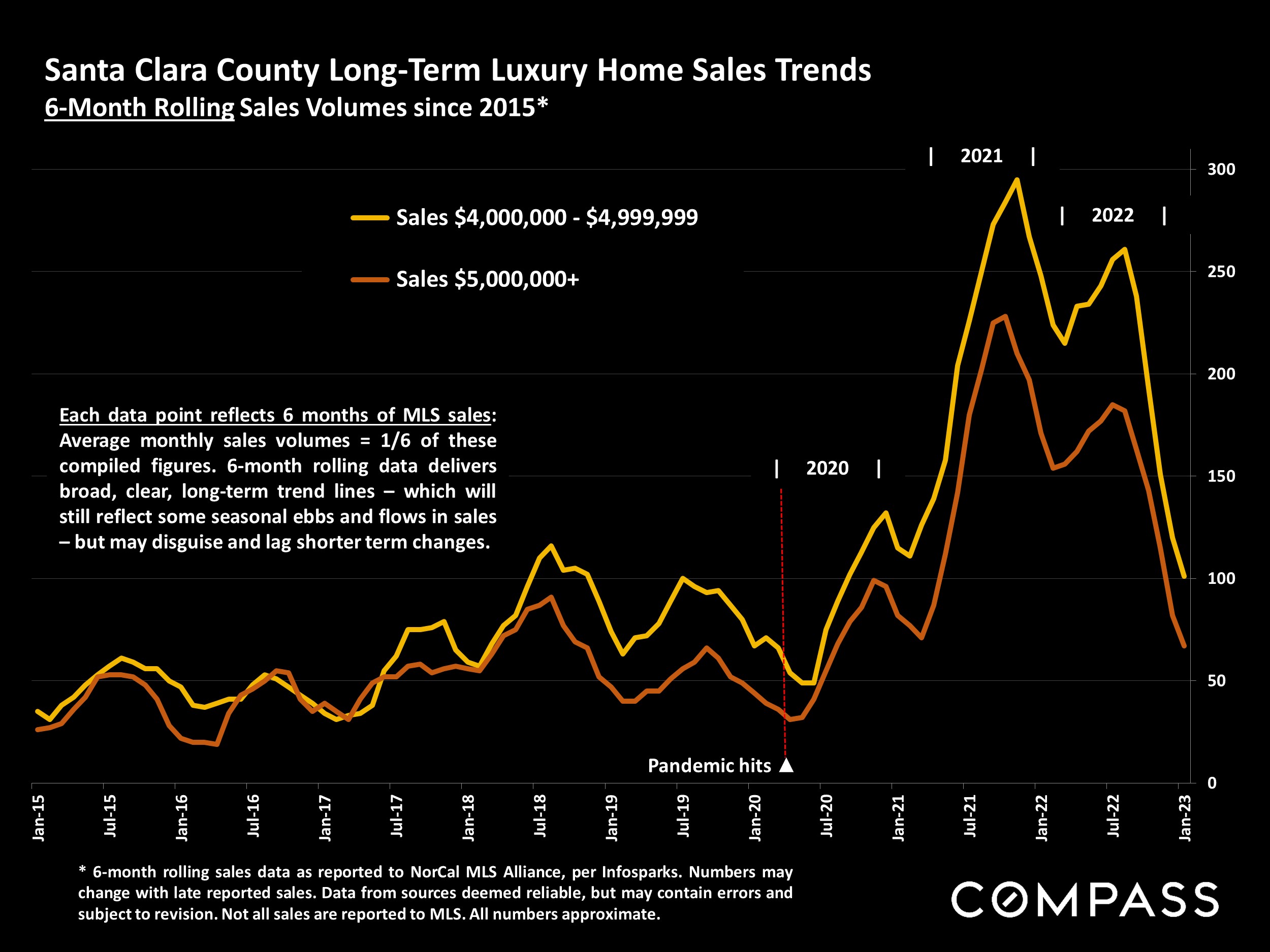

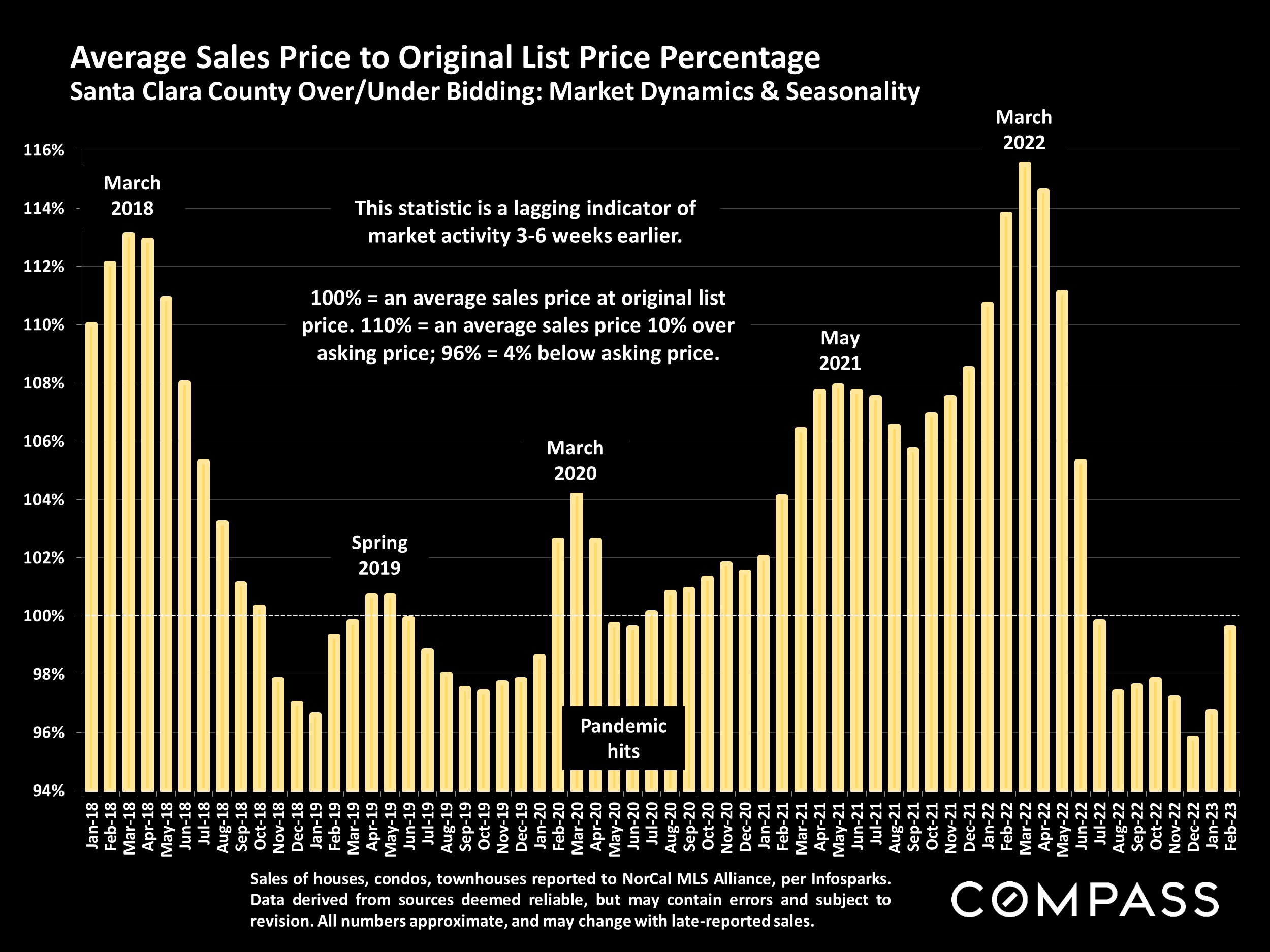

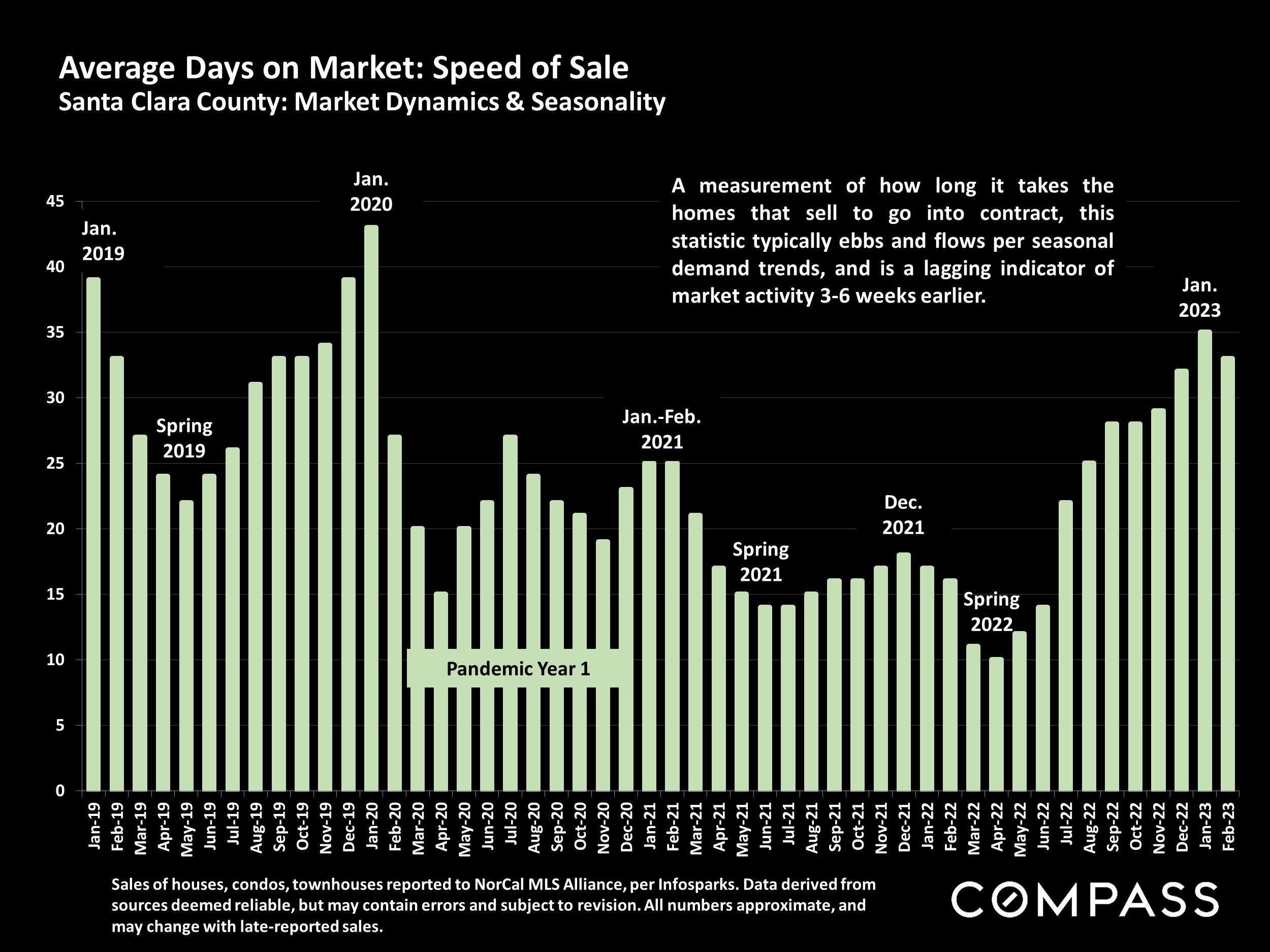

2023 Market Indicators Turn Positive (But Interest Rates Climb Again)

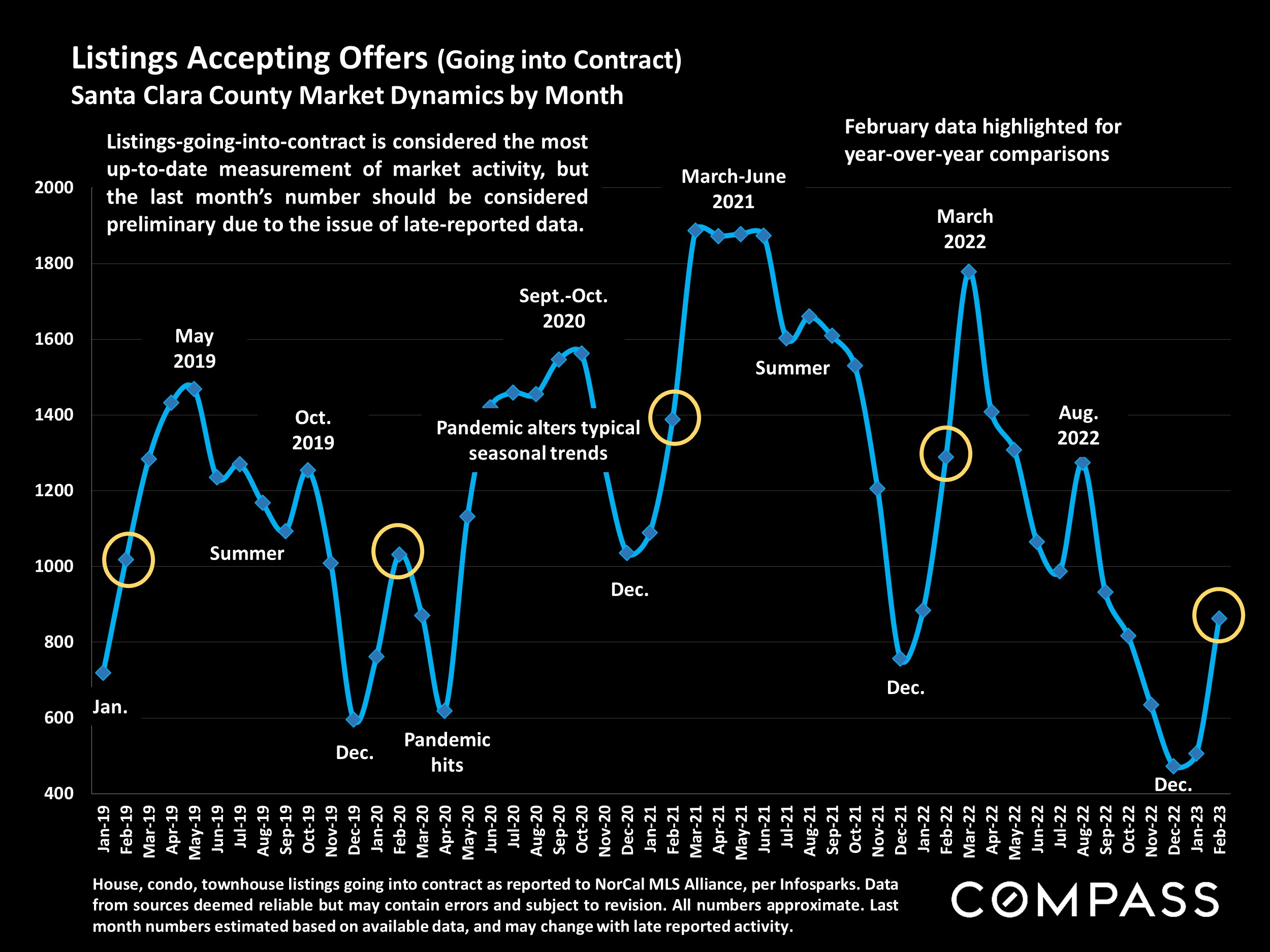

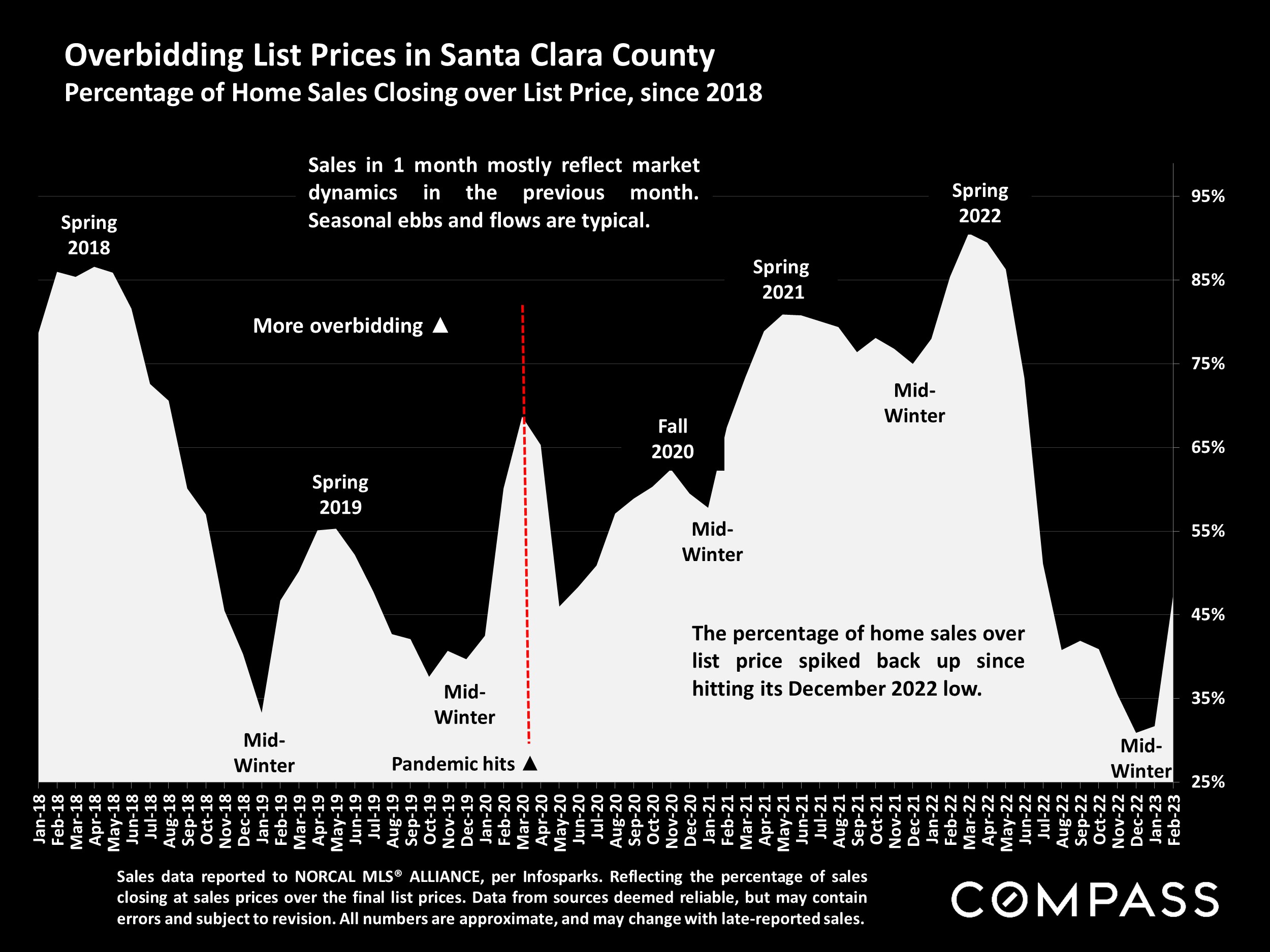

After the acute decline in market activity occurring in the 2nd half of 2022, buyer demand rebounded dramatically and most market indicators turned positive in early 2023: Open house traffic, number of offers, and overbidding and absorption rates all saw improvement.*

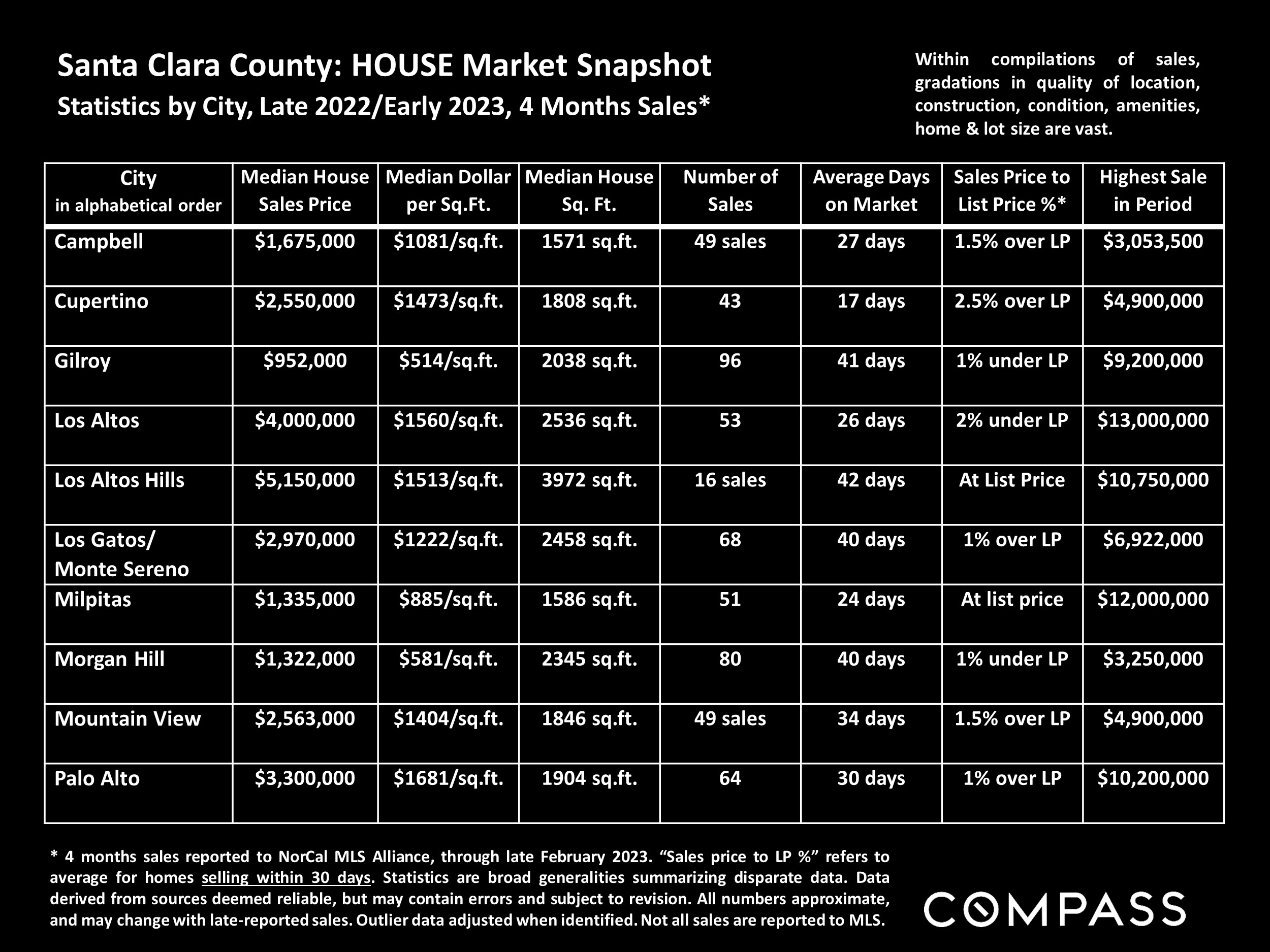

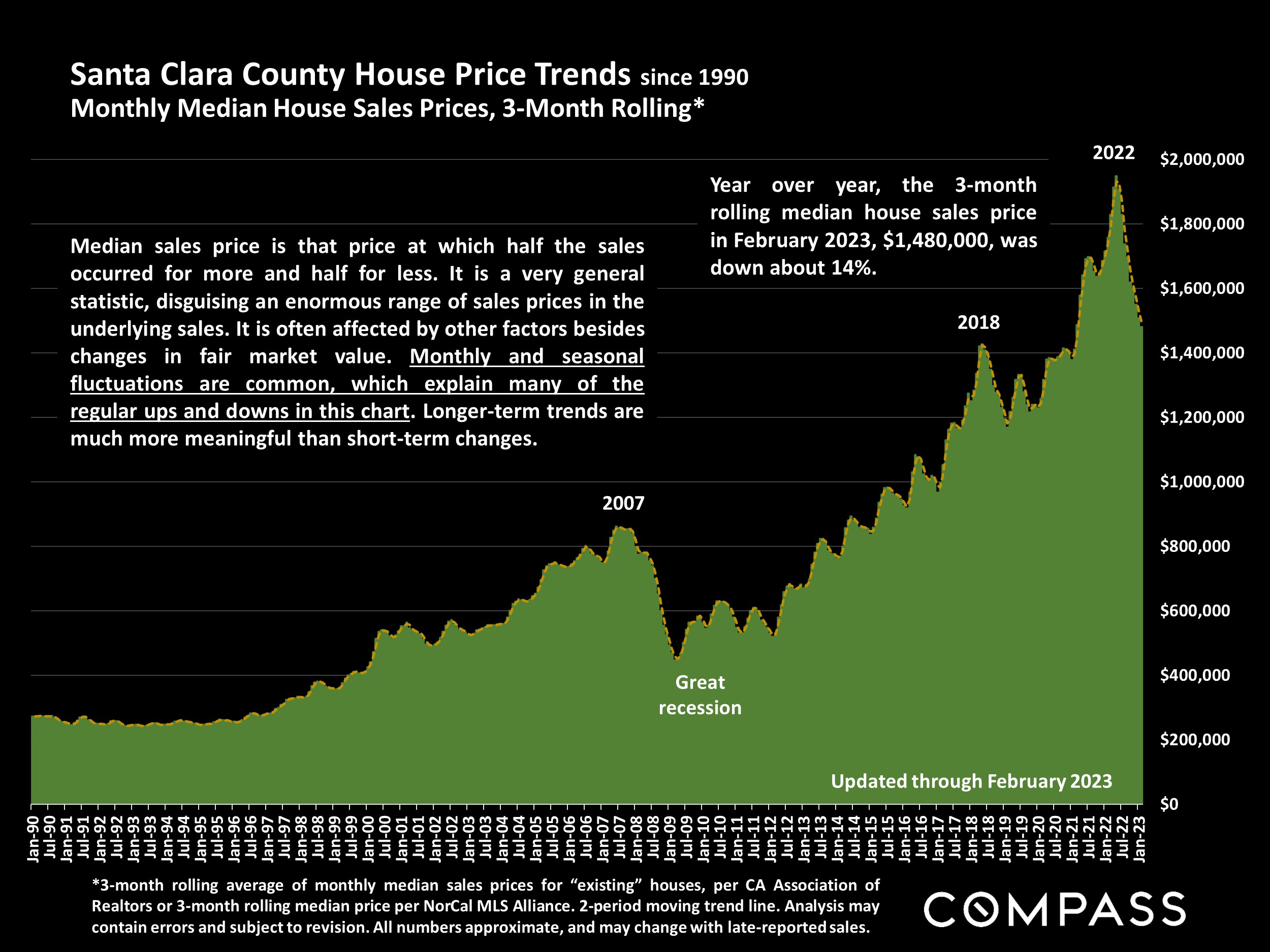

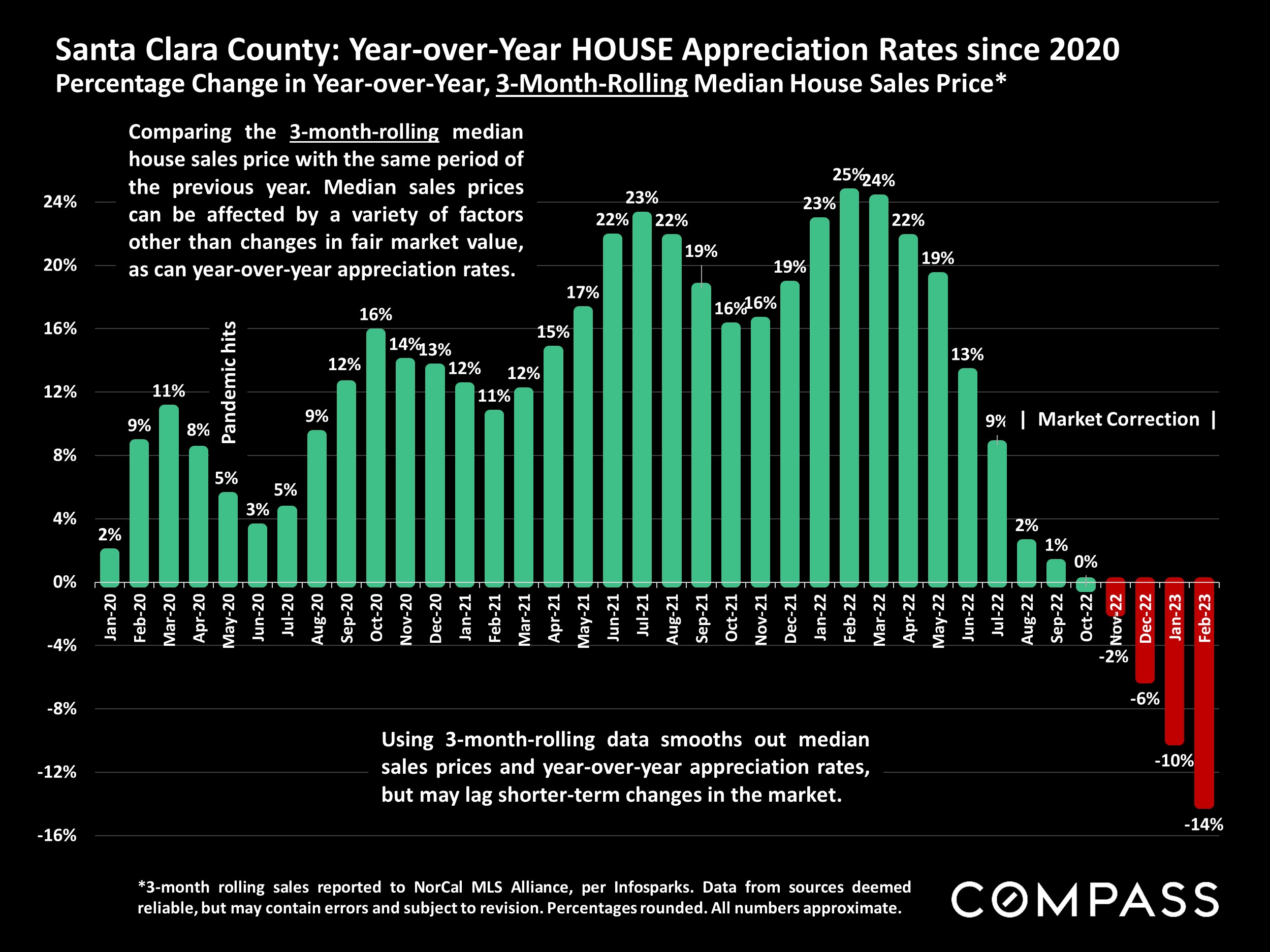

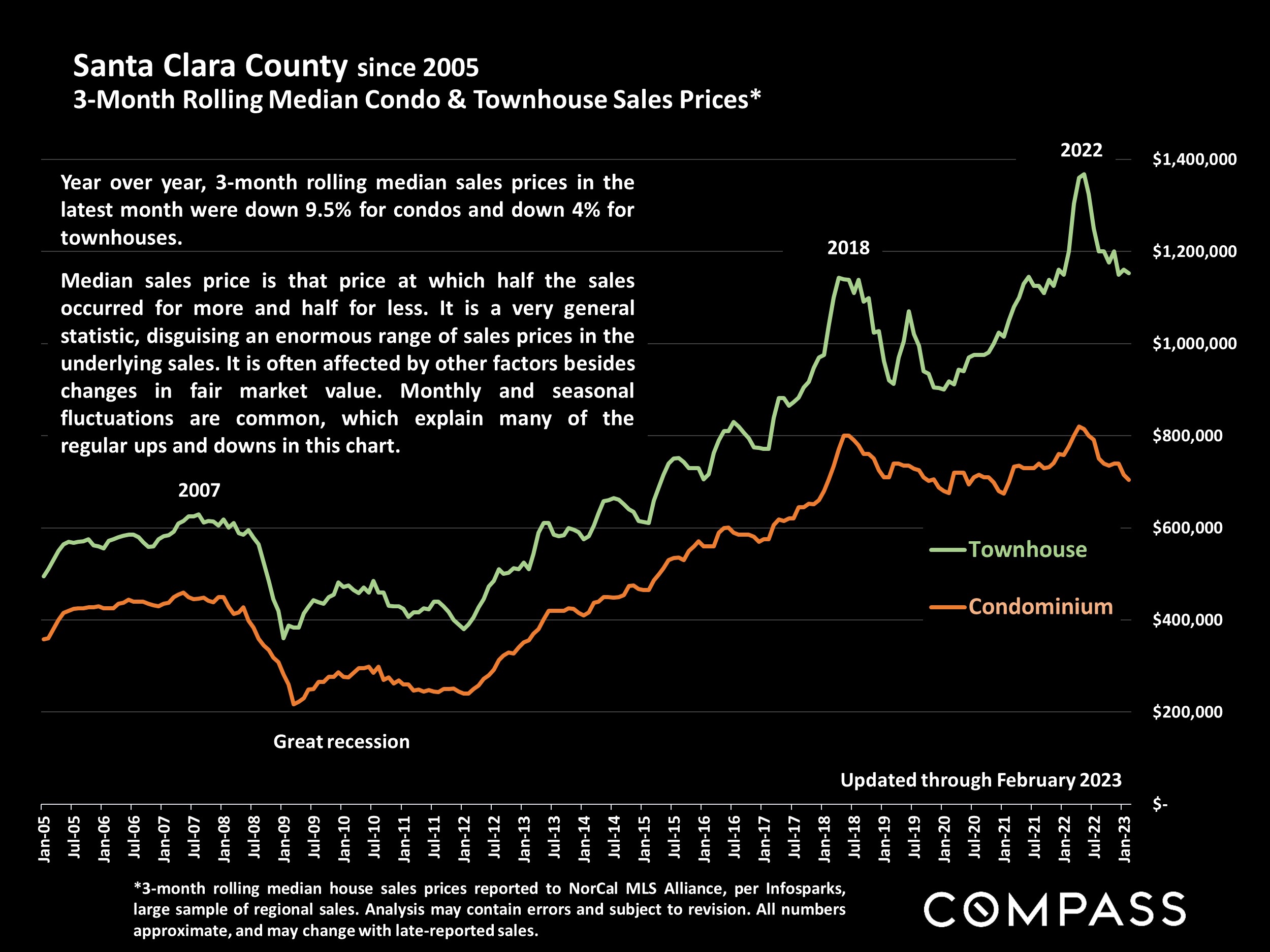

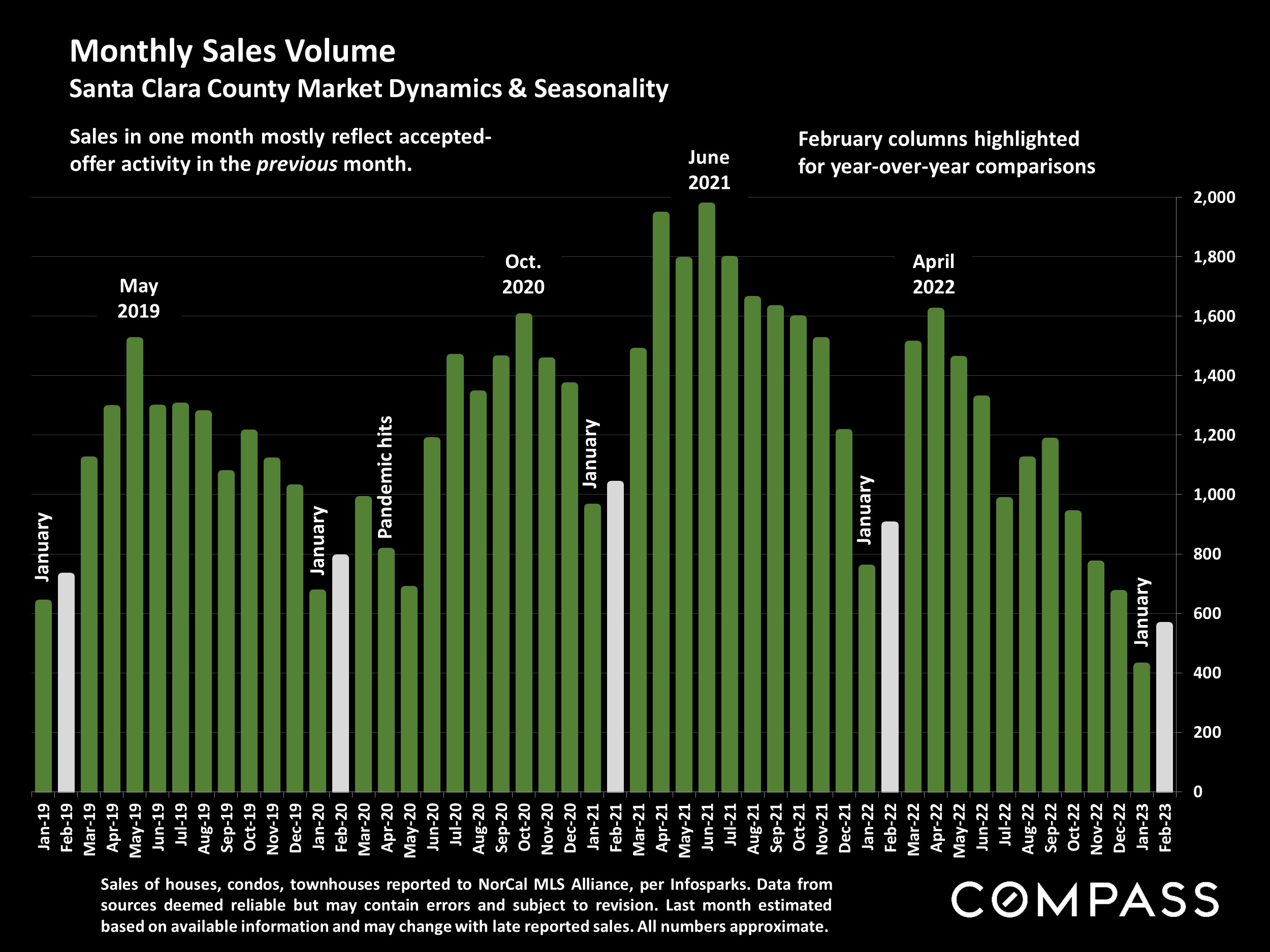

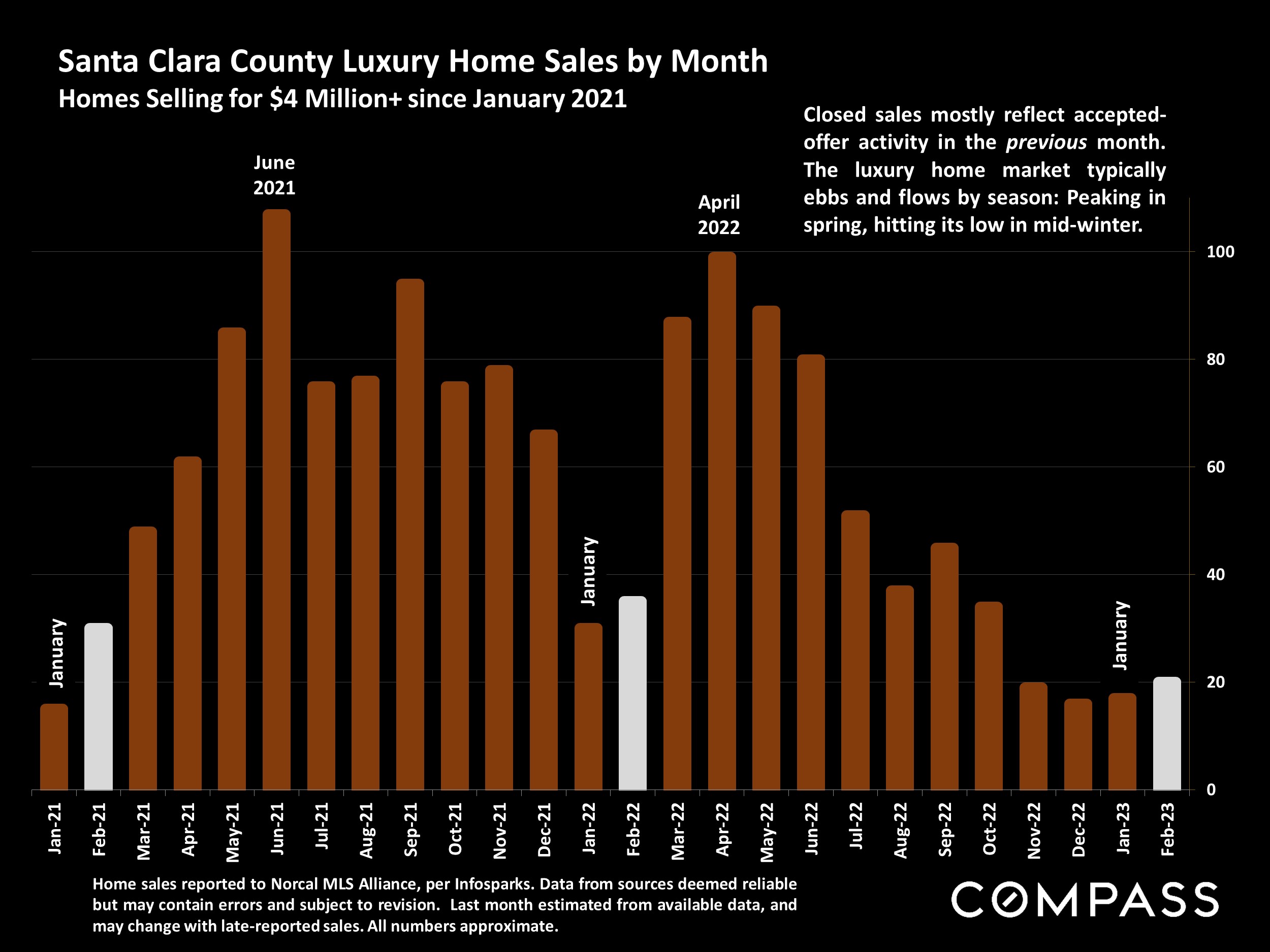

It is too early for significant effects to show up in home prices: Indeed, through February, 3- month-rolling median house sales prices saw year-over-year declines across all Bay Area counties. (These percentage declines should be regarded cautiously until substantiated over the longer term.) Even with the striking improvement in demand over late 2022, most year-over-year indicators remain depressed, but these comparisons are with the severely overheated conditions prevailing at the peak of a 10-year housing market upcycle. The market was still just waking up in February. March through May is typically the most active listing and sales period of the year, and should soon provide much more data on supply, demand and price trends. Over the last 3 years, spring markets were deeply affected, in very different and often surprising ways, by the onset of the pandemic (2020), the pandemic boom (2021), and soaring interest rates (2022).

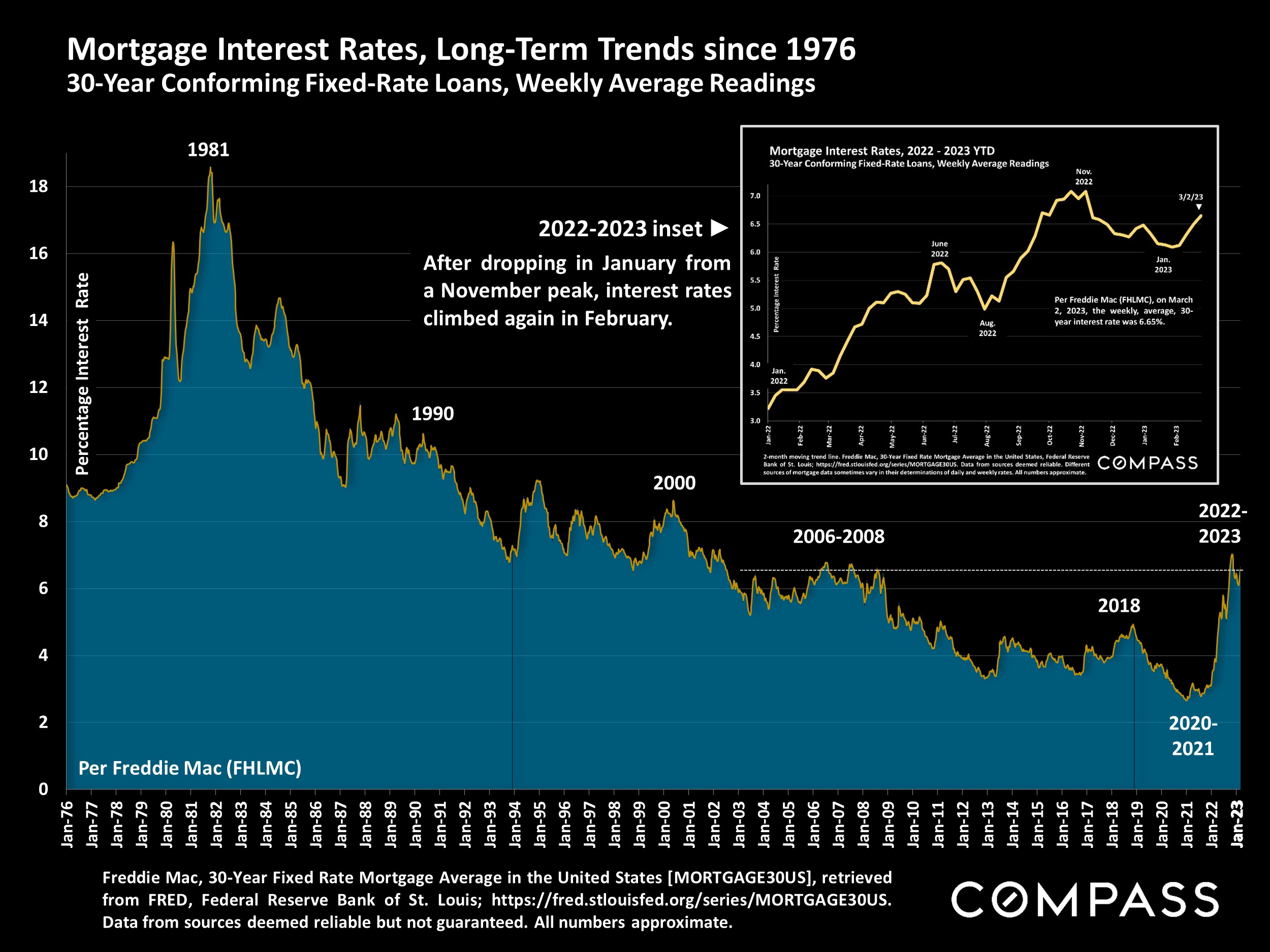

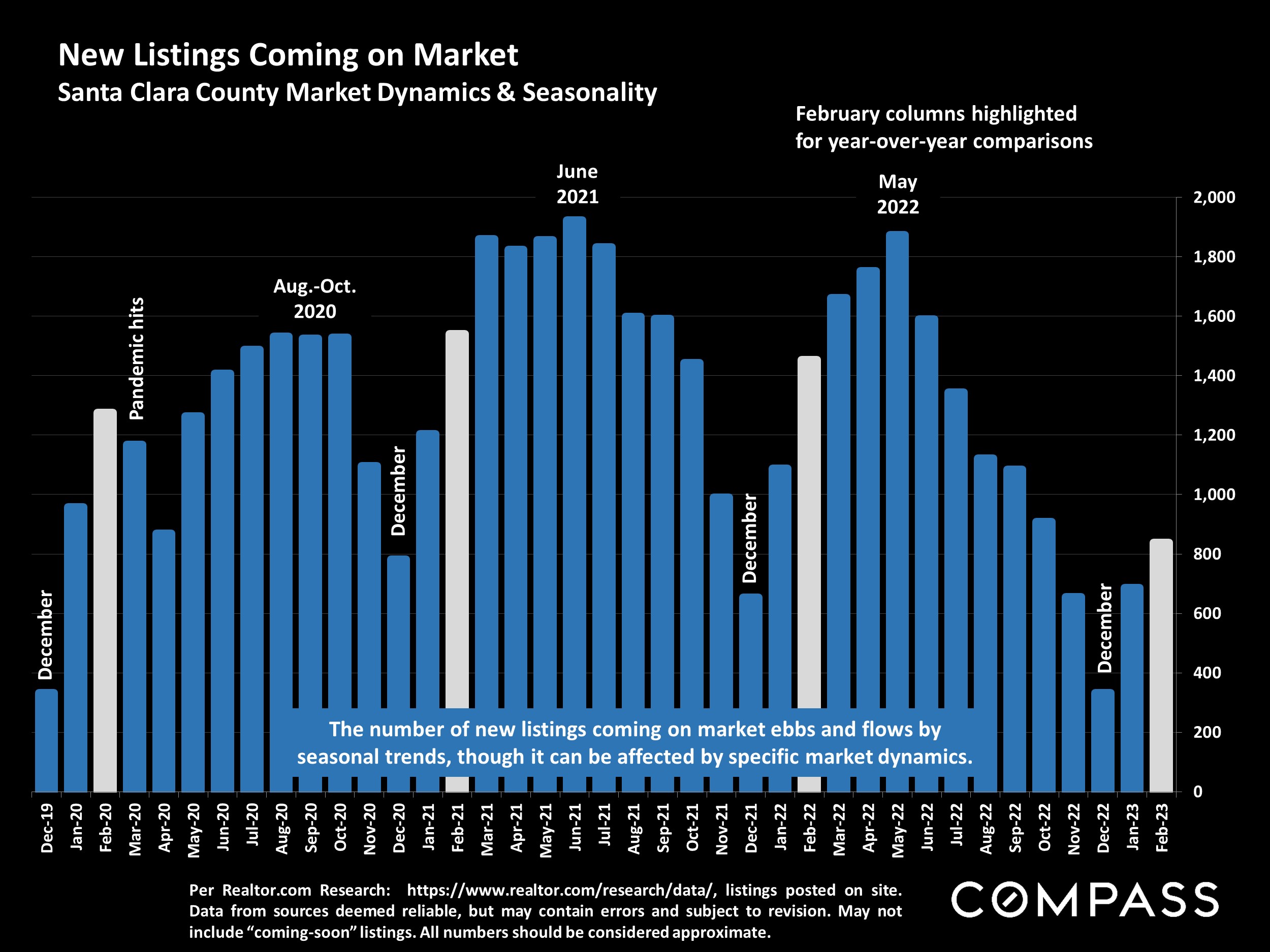

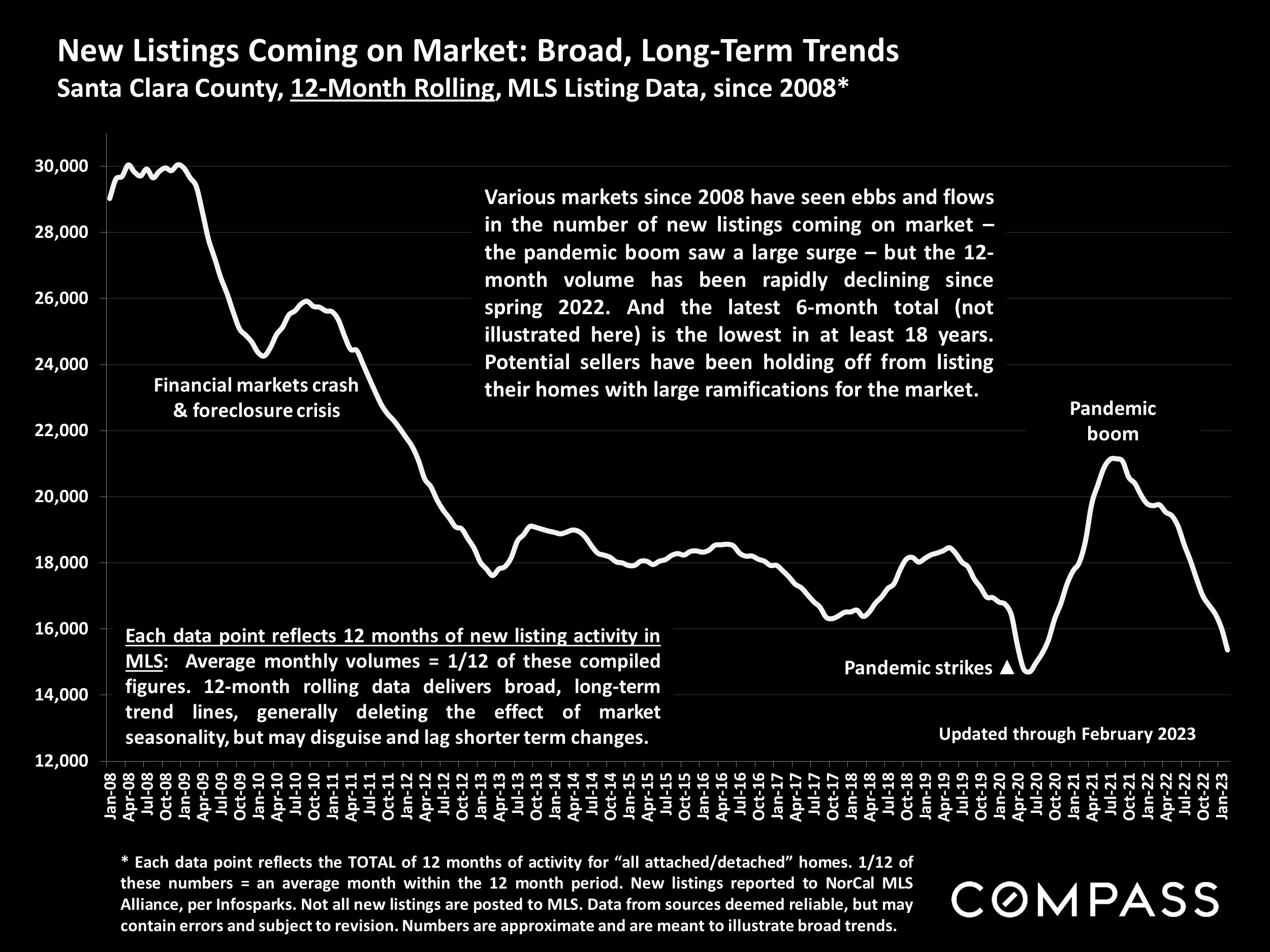

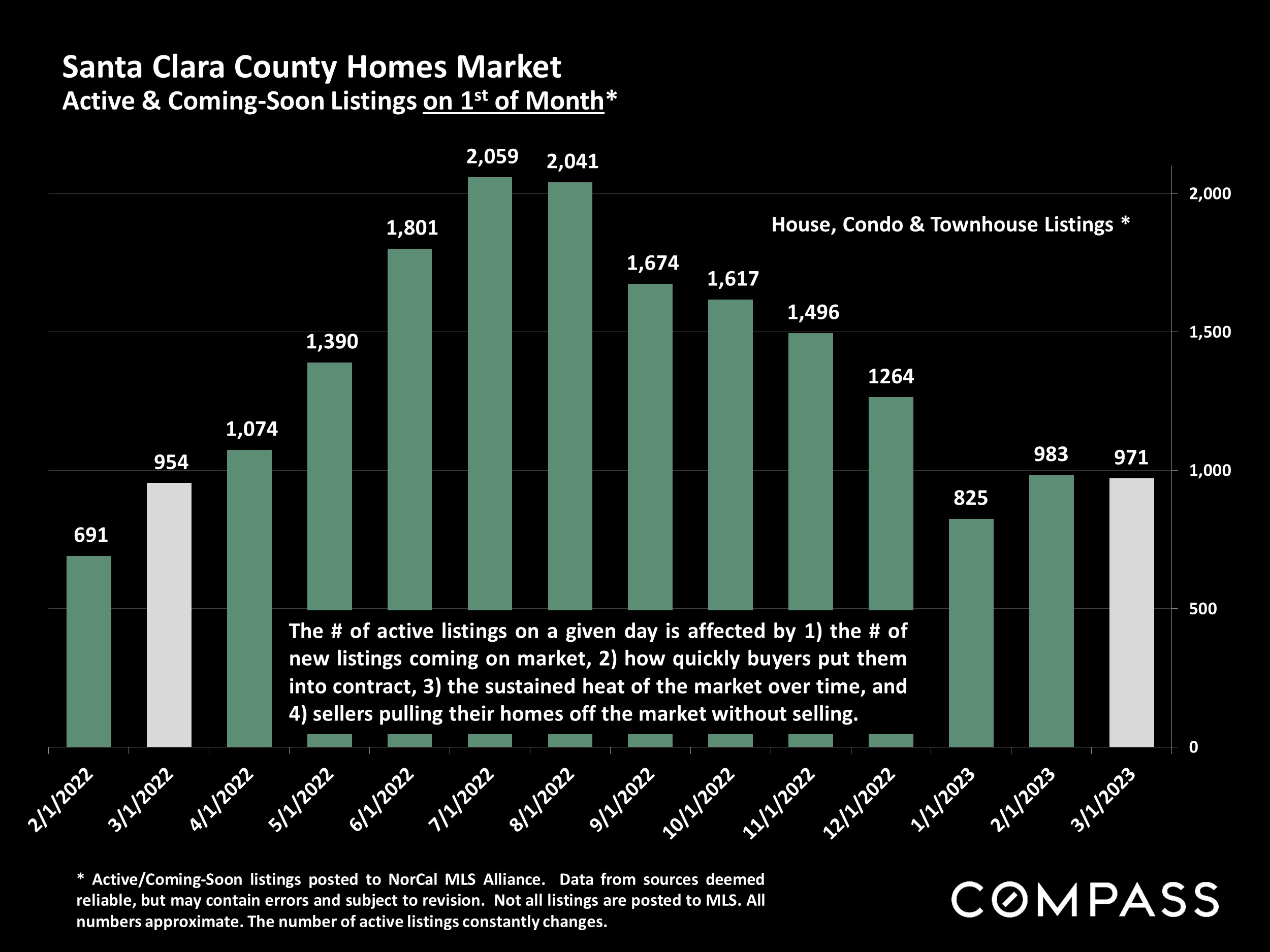

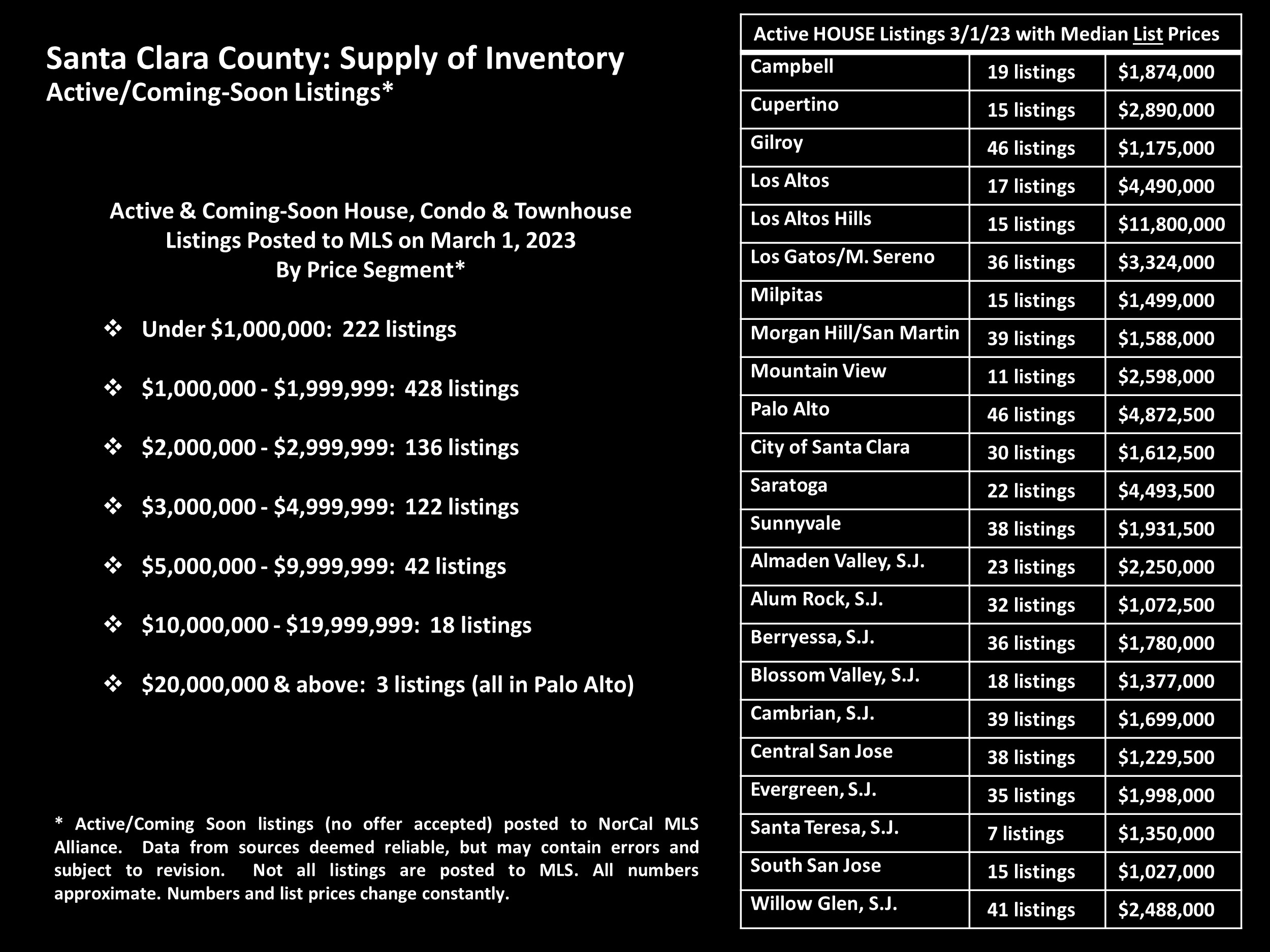

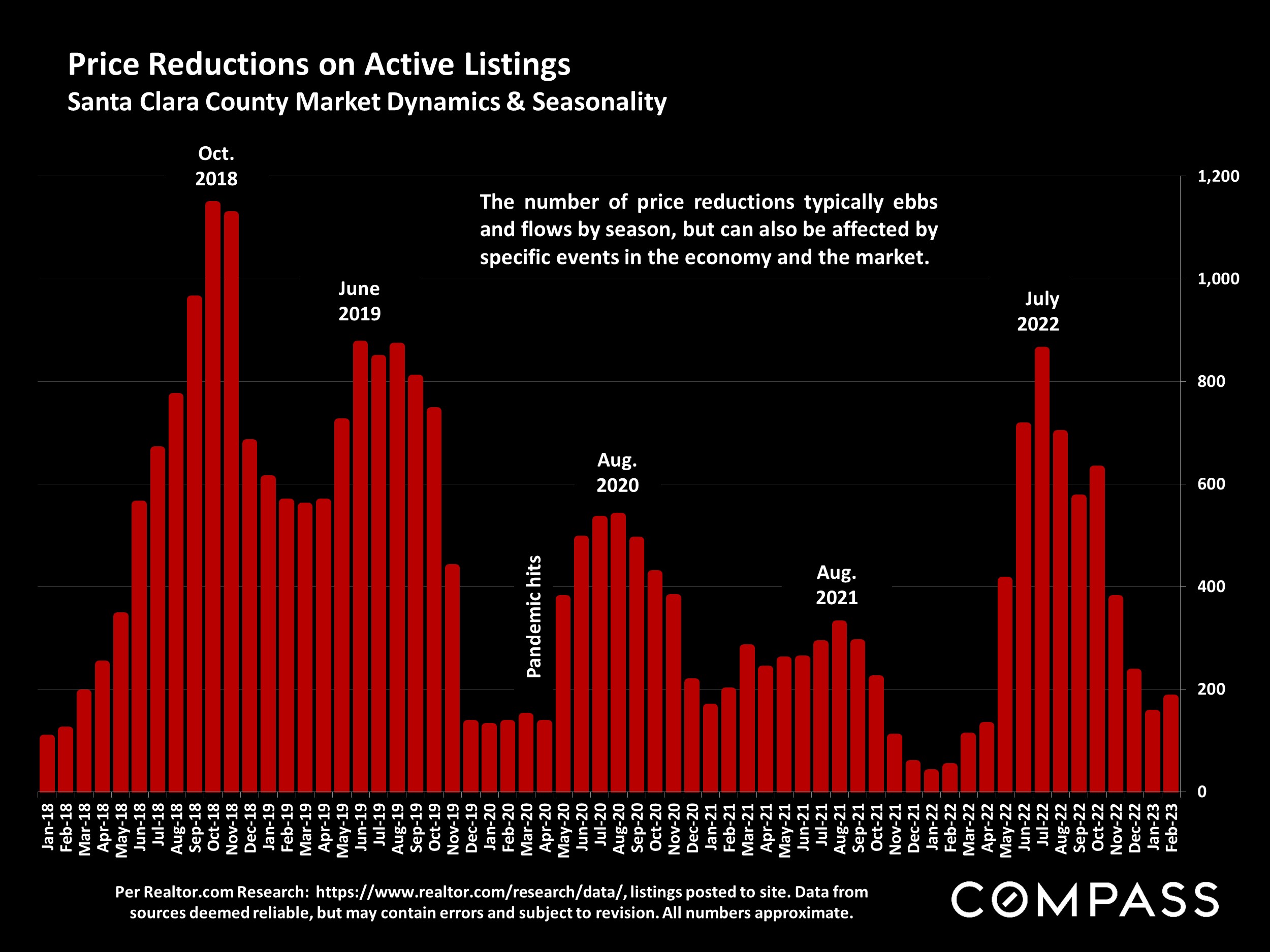

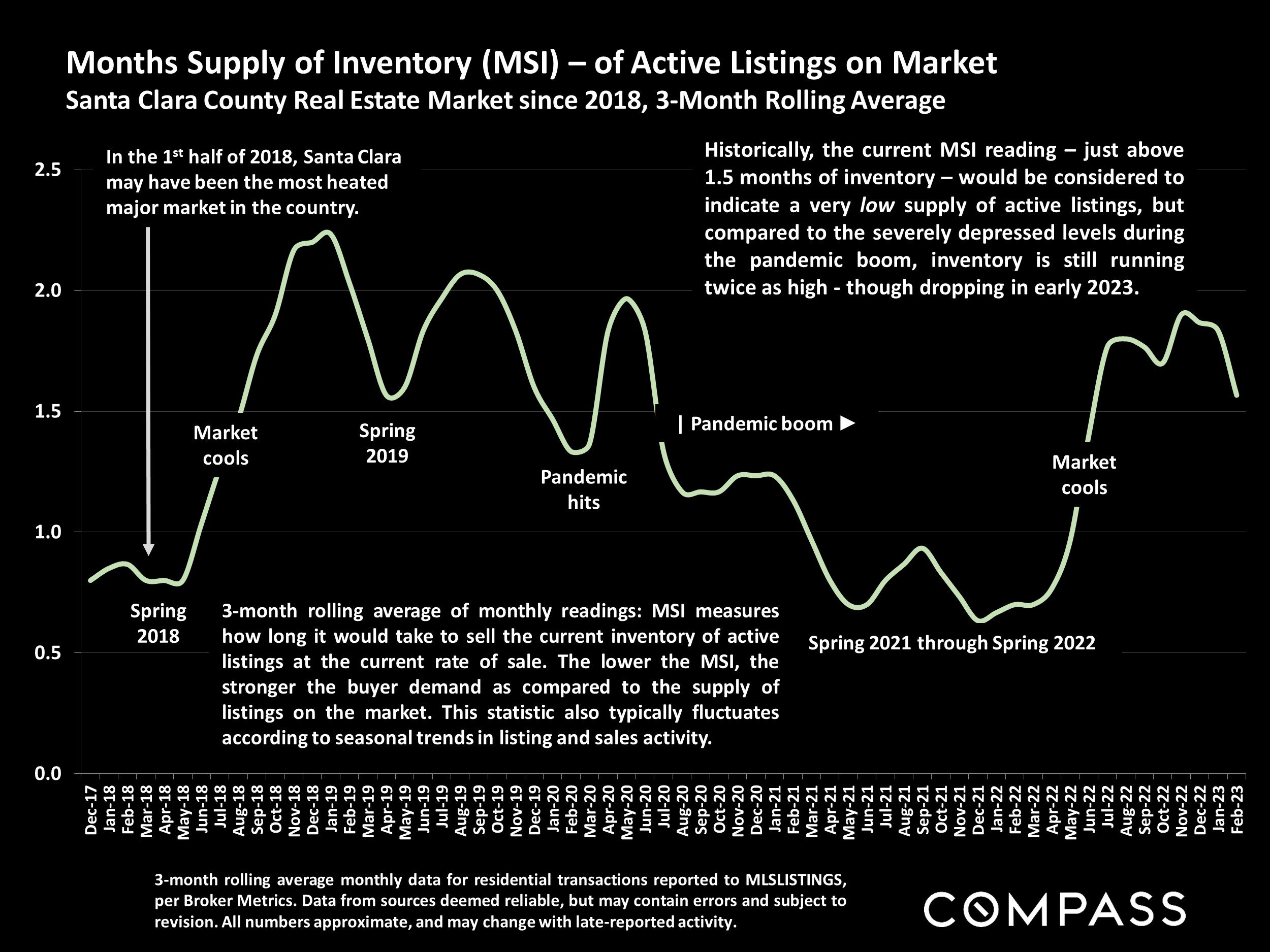

As has been the case for the last 14 months, the biggest wildcard remains interest rates: After dropping considerably in January from a November peak, they climbed again in February, with big impacts on loan application rates. It has been very challenging to predict short-term interest rate changes. Another major factor is the substantial decrease in the number of new listings coming on market, a critical issue with wide ramifications if it continues.

*Sales in one month generally reflect deal-making in the previous month, and often pertain to listings that have already been on the market for months longer. Many real estate statistics are lagging indicators, and even dramatic shifts in demand may show up only very gradually in their readings.

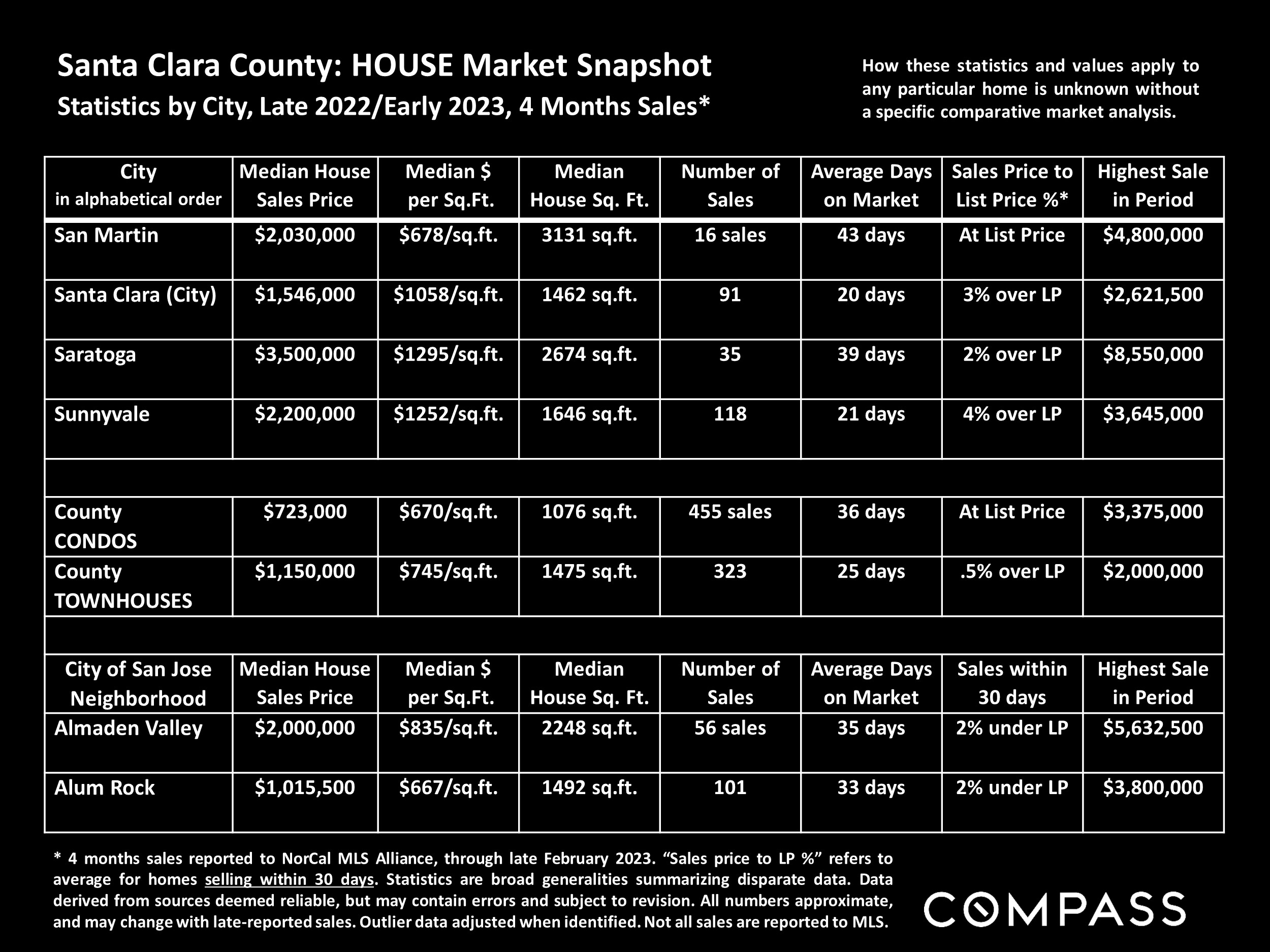

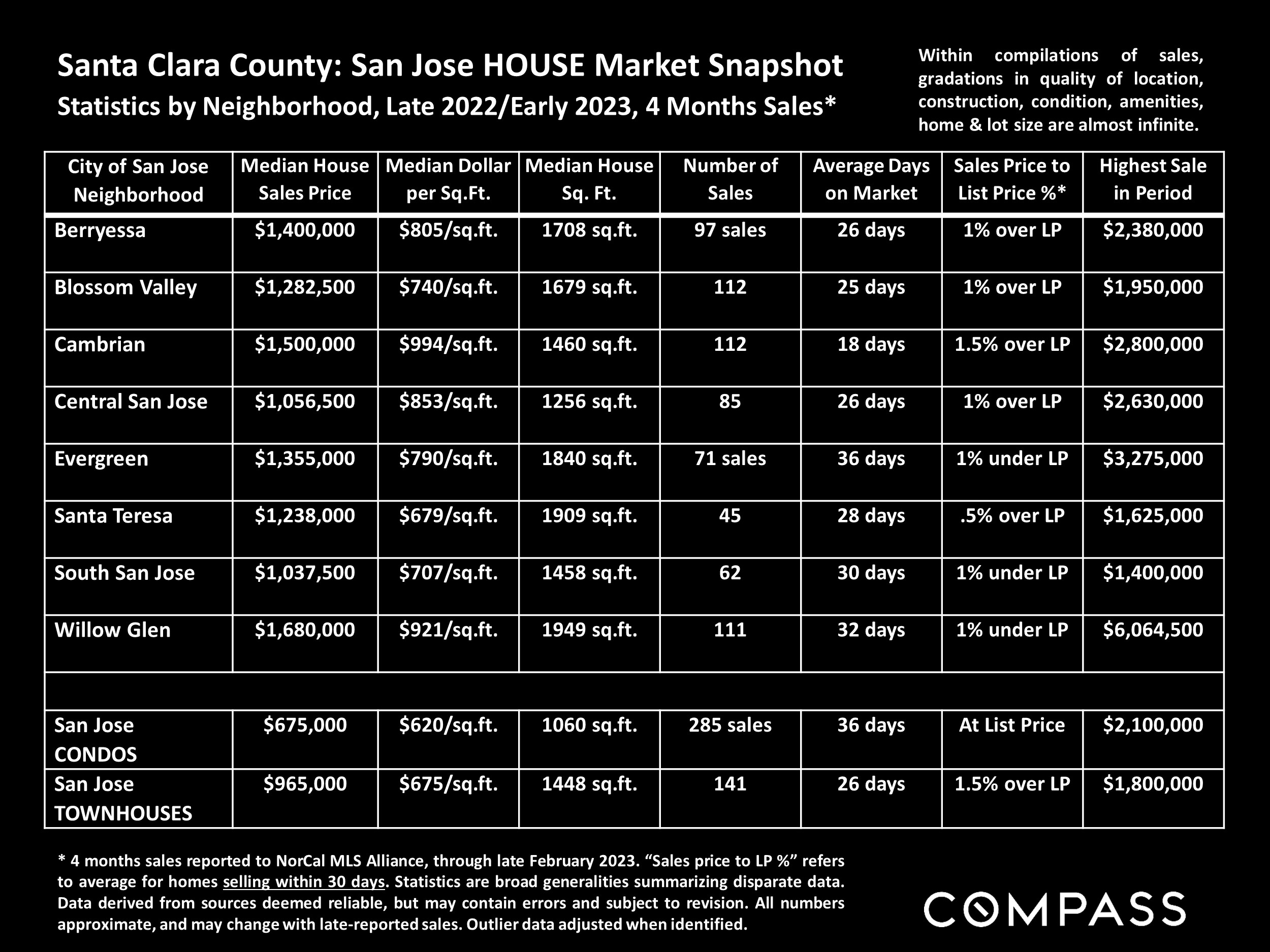

Statistics are generalities, essentially summaries of widely disparate data generated by dozens, hundreds or thousands of unique, individual sales occurring within different time periods. They are best seen not as precise measurements, but as broad, comparative indicators, with reasonable margins of error. Anomalous fluctuations in statistics are not uncommon, especially in smaller, expensive market segments. Last period data should be considered estimates that may change with late-reported data. Different analytics programs sometimes define statistics – such as “active listings,” “days on market,” and “months supply of inventory” – differently: what is most meaningful are not specific calculations but the trends they illustrate. Most listing and sales data derives from the local or regional multi-listing service (MLS) of the area specified in the analysis, but not all listings or sales are reported to MLS and these won’t be reflected in the data. “Homes” signifies real-property, single-household housing units: houses, condos, co-ops, townhouses, duets and TICs (but not mobile homes), as applicable to each market. City/town names refer specifically to the named cities and towns, unless otherwise delineated. Multi-county metro areas will be specified as such. Data from sources deemed reliable, but may contain errors and subject to revision. All numbers to be considered approximate.

Many aspects of value cannot be adequately reflected in median and average statistics: curb appeal, age, condition, amenities, views, lot size, quality of outdoor space, “bonus” rooms, additional parking, quality of location within the neighborhood, and so on. How any of these statistics apply to any particular home is unknown without a specific comparative market analysis. Median Sales Price is that price at which half the properties sold for more and half for less. It may be affected by seasonality, “unusual” events, or changes in inventory and buying trends, as well as by changes in fair market value. The median sales price for an area will often conceal an enormous variety of sales prices in the underlying individual sales.

Dollar per Square Foot is based upon the home’s interior living space and does not include garages, unfinished attics and basements, rooms built without permit, patios, decks or yards (though all those can add value to a home). These figures are usually derived from appraisals or tax records, but are sometimes unreliable (especially for older homes) or unreported altogether. The calculation can only be made on those home sales that reported square footage.

Compass is a real estate broker licensed by the State of California, DRE 01527235. Equal Housing Opportunity. This report has been prepared solely for information purposes. The information herein is based on or derived from information generally available to the public and/or from sources believed to be reliable. No representation or warranty can be given with respect to the accuracy or completeness of the information. Compass disclaims any and all liability relating to this report, including without limitation any express or implied representations or warranties for statements contained in, and omissions from, the report. Nothing contained herein is intended to be or should be read as any regulatory, legal, tax, accounting or other advice and Compass does not provide such advice. All opinions are subject to change without notice. Compass makes no representation regarding the accuracy of any statements regarding any references to the laws, statutes or regulations of any state are those of the author(s). Past performance is no guarantee of future results.